Easyjet has now released their final results for the year ended 2018.

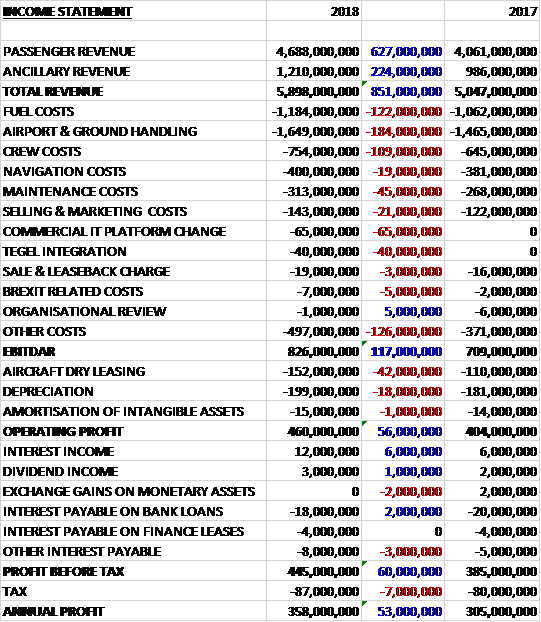

Revenues increased when compared to last year with a £627M growth in passenger revenue and a £224M increase in ancillary revenue. Fuel costs increased by £122M, airport and ground handling charges were up £184M, crew costs increased by £109M, maintenance costs grew by £45M and selling and marketing costs were up £21M. There was a £65M charge related to the commercial IT platform change and £40M was spent on the Tegel integration. Other costs were up £126M to give an EBITDA of £826M, an increase of £117M. Aircraft dry leasing charges grew by £42M and depreciation was up £18M to give an operating profit £56M higher. There was a small increase in interest income offset by a £7M growth in tax charges which meant the profit for the year was £358M, a growth of £53M year on year.

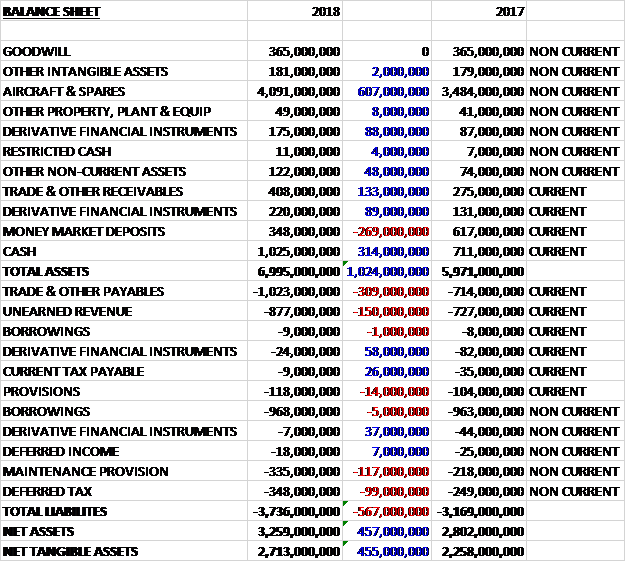

When compared to the end point of last year, total assets increased by £1.024BN, driven by a £607M increase in aircraft and spares, a £314M growth in cash, a £133M increase in receivables, and a £177M growth in derivative financial assets, partially offset by a £269M decline in money market deposits. Total liabilities also increased during the year as a £95M decline in derivative financial liabilities was more than offset by a £309M growth in payables, a £150M increase in unearned revenue, a £117M increase in the maintenance provision and a £99M growth in deferred tax liabilities. The end result was a net tangible asset level of £2.713BN, a growth of £455M year on year.

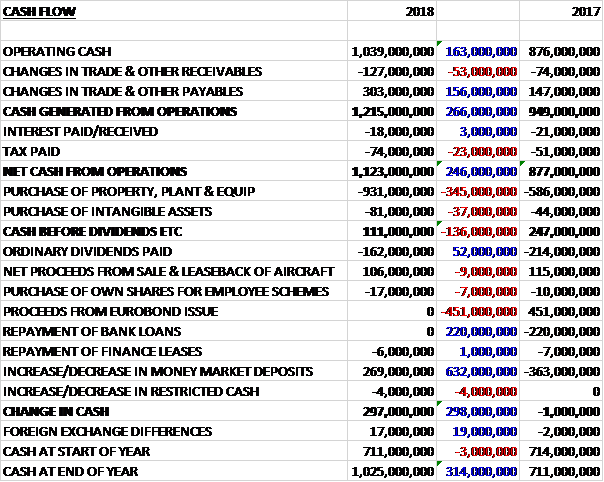

Before movements in working capital, cash profits increased by £163M to £1.039BN. There was a cash inflow from working capital and even after tax payments increased by £23M the net cash from operations was £1.123BN, a growth of £246M year on year. The group spent £931M on property, plant and equipment and £81M on intangible assets to give a free cash flow of £111M. They paid out £162M in dividends and received £106M from the sale and leaseback of aircraft and £269M from a decrease in money market deposits to give a cash flow of £297M and a cash level of £1.025BN at the year-end.

The total European short haul market grew by 5.6% and by 2.8% in the group’s markets. This was lower than in previous years reflecting a rising price of oil and the various issues affecting other airlines. Since the Brexit vote, Sterling has fallen significantly which has had an ongoing negative impact on profit.

Total revenue per seat grew by 6.4% to £61.94 and by 4.7% at constant currency. Passenger revenue grew by 15.4% driven by passenger growth of 10%, nearly half of which was due to Tegel; an increase in the load factor of 0.3% to a record 92.9%. Excluding Tegel this was up 1% to 93.6%; a good demand growth in the UK and France; the benefit of the Monarch and Air Berlin bankruptcies and Ryanair cancellations; and industrial action in France that led to a benefit of £20M as competitor airline and train customers switched to EasyJet.

Ancillary revenue was also very strong and grew 23% (18% excluding Tegel). This was driven by new bag segmentation leading to better conversion rates and improved bag pricing algorithms that better reflected demand, allocated seating demand driving higher conversion rates through pricing improvements and improvements to the website making it easier for customers to add ancillary products.

The growth in ancillary revenue was due to a number of initiatives such as improvements to the baggage options offered, with the introduction of 15Kg and 23Kg options, the continued enhancement of hands free and home puck-up services; continued multi-variant testing of their digital merchandising of ancillary products, leading to a 6% increase in allocated seat attachment rates; the launch of new partnerships such as insurance with Collinson and a two year partnership with Three Mobile who sponsor Hands Free for their UK customers/

In addition there was a trial of an inflight entertainment platform accessed through customers’ own devices, which has driven a 22% improvement in customer satisfaction for customers using the platform vs the average network; the growth of Worldwide by EasyJet, now offering connections to more than ten partner airlines across eleven airports in the network. Bag attachment rates for these bookings are 20% higher than the network average and the missed connection rate below 0.5%. there was growth in the inflight retail business, with inflight vouchers now available in the booking funnel and average transaction value increasing by 4%; and an increase in EasyJet Plus membership of 52%.

The headline cost per seat increased by 4.4% to £55.87, driven by exchange rates, underlying cost inflation and the cost of disruption which remains a major industry challenge. At constant currency it increased by 2.7% and 4.8% excluding fuel. The increase in costs was impacted by disruption with significant third party industrial action, particularly in France, air traffic control capacity constraints due to systems upgrades and weather, which meant a large increase in cancellations to 6,814. Also affecting the price was crew cost inflation, higher crewing levels to support resilience, general inflation and a negative impact from Airbus delivery delays resulting in lower than planned standby aircraft and wet leased aircraft. This was offset by total cost programme savings of £107M and better cost control in airport costs with lower navigation fees.

Total fuel costs increased by 11.5% as a result of capacity growth, higher emissions trading system costs and adverse forex movements. Fuel cost per seat at constant currency declined by 4.3% to £11.72. They have hedged 69% of fuel requirements for H1 2019 for $567 per tonne, 65% in H2 for $571 and 45% in 2020 for $654. The current price of fuel stands at $664 per tonne compared to $501 per tonne last year. Due to hedging, the actual price of fuel for the airline declined by $6 to $590 per tonne.

In December 2017 the group completed the acquisition of part of Air Berlin’s operations at Berlin Tegel airport. This resulted in them becoming the largest short haul operator in Berlin, leapfrogging Lufthansa and Ryanair. Their flying programme at Tegel started in early January, operating an adopted winter schedule with a fleet of mainly wet leased aircraft. As expected, this resulted in a dilutive impact to overall load performance and revenue per seat and an increase in cost per seat while the operation becomes established.

Overall progress to date has been in line with expectations and on track to demonstrate the value of the acquisition. Since start up, EasyJet has seen strong operational performance with on-time performance of 82% vs a network average of 75%. Brand consideration scores have also increased by 5pts in Germany as a result of their increased presence. Demand has been growing steadily with load factors reaching 86% over the summer period despite an inefficient schedule.

The headline profit impact was worse than first expected due to increases in unhedged fuel costs, airport charges and taxes as well as late competitive capacity in the market. Performance improved during the summer as the group took direct control of its revenue management system to improve data decisions and revenue profiles. The total loss for the year is better than originally expected at £152M due in part to faster than planned transition of crew and fleet. In 2019 their Tegel operations will benefit from a longer selling window, schedule improvements, a full flying programme, no planned wet lease costs and pricing optimisation. Schedule optimisation will continue into 2020.

In the UK there was a 4% increase in capacity, in part to match airport capacity increases at Luton; in France there was a 5% increase aligned with their strategy of regional growth; in Switzerland a growth of 7% including a focus at their base in Basel; in Italy a 10% increase in capacity as a result of consolidation in Venice; a 48% increase in Germany following the Air Berlin acquisition; a 3% increase in the Netherlands consolidating the position at Schipol, adding routes and frequencies; and a 6% increase in Portugal to strengthen connections to the rest of Europe.

The group see an opportunity to radically change their holiday offering. Currently only one in forty EasyJet customers book a hotel through the group which they plan to change by refining their current business model to capture more value through the customer journey, build the necessary infrastructure to directly curate their product offering, develop direct relationships with hotel partners, and build enhanced value from bundling.

They also plan to improve the profit made in this area by moving to a contribution rather than commission model. They have already spoken to a large number of hotel partners and are progressing well to develop stronger direct relationships with them. Their core focus will remain on flights but the holiday offering incorporates other aspects of the customer journey which can be sold to a customer base that is well aligned.

There was a 17% increase in business customers, driven in particular by strong business penetration on Berlin Tegel routes. The business pricing premium increased by 14% due to higher penetration and the benefit of cancellations by other airlines leading to late bookings and higher yields. High premiums were also generated from sales through indirect channels.

The group will extend their business offer through the development of business products, a recognition programme and improved back office functionality. The development will focus on improving connectivity to their customers through improved back office functionality including the development of an SME portal; a more personalised product offering including new business fares and bundles; and ongoing improvements to the schedule. Since may they have started to offer semi-automated invoicing, launched Flight Club for business partners, undertaken schedule analysis and adapted their schedule to prioritise business routes at certain times of the day.

Over the last few years the impact of increasing disruption has led to a declining trend in on time performance and customer satisfaction. During 2018, on time performance decreased by 1% to 75%. The group has begun a process of self-help which has already seen a strong improvement at Gatwick by 3% to 68% following the contract with DHL to provide ground handling, further investments in resilience and as a result of their partnership with Gatwick to resolve wider system issues. As a result of this improvement, they have now agreed with DHL to manage ground handling at Bristol and Manchester too.

As of the year-end the group had taken delivery of two A321s with a third since delivered. These aircraft are operated from Gatwick, enabling growth in a slot-constrained airport. The planes have a 51% higher seat capacity than the A319s and deliver 9% cost savings compared to an A320neo and 20% more than the A319.

The group is potentially going to be severely affected by Brexit. They have established an Austrian entity which will enable them to continue to operate flights domestically in the EU. In order to operate air services within the EU, however, they must comply with the requirement that a majority of shareholders must be nationals of a member state, Switzerland, Norway, Iceland or Liechtenstein. Already 47% of shares are hold by these nationals and they are trying to get this to increase to more than 50%.

The group is permitted to regulate the level of ownership by non-qualifying nationals by suspending rights to attend and vote at meetings and forcing the sale of shares. They currently have no intention of exercising these powers but this will be kept under review pending the outcome of Brexit.

As usual there are a number of non-headline items. The largest was a £65M commercial IT platform charge. During the year they decided to change their approach to technology development for their commercial IT platform through better utilisation and development of existing systems on a modular basis rather than working towards a full replacement of their core commercial platform. The charge was required to write down IT assets under development which will no longer be used by the business. A charge of £5M in relation to associated commitments was also incurred.

The next item was a £40M integration cost of the Tegel operation. This comprises £14M of engineering costs to align the technical specs of ex-Air Berlin aircraft with the rest of the EasyJet fleet, £10M of dry lease rental costs incurred prior to those aircraft being operational, £7M of crew costs and £9M of other costs including consultancy and legal fees.

The group incurred £19M of sale and leaseback costs relating to ten of their oldest A319 aircraft. This included a loss on disposal of £11M and an £8M maintenance provision. There were Brexit-related costs of £7M principally due to the cost of re-registering aircraft in Austria, and £2M of other non-headline costs.

Going forward the group’s capacity growth in the first half of next year is expected to be around 15% and 10% in the year as a whole. On a like for like basis, revenue per seat is expected to be down by low to mid-single digits including the effect of annualisation of one-off revenue benefits from this year, dilution from Berlin and the effect of Easter moving to the second half. On the same basis, total headline cost per seat excluding fuel is expected to be flat next year. Capex for the year is expected to be £1BN. There are initiatives targeted to deliver savings of over £100M in 2019, offsetting inflationary pressures.

Revenue per seat in H1 is expected to be down by mid-single digits mainly due to the new treatment of booking fee revenue which is now recognised at the time of flying and which will benefit the second half of the year, as well as the revised treatment of disruption costs which are now partially offset against revenue. Based on the current fuel price, fuel costs for next year are expected to be a headwind of between £50M and £100M and the forex impact is expected to be a headwind of around £10M.

At the current share price the shares are trading on a PE ratio of 12.2 which falls to 10.2 on next year’s consensus forecast. After a 43% increase in the dividend the shares are yielding 5.3% which increases to 5.4% on next year’s forecast. At the year-end the group had a net cash position of £396M compared to £357M at the end of last year. After allowing for the impact of aircraft operating leases etc, adjusted net debt increased by £325M to £738M, however.

On the 22nd November the group announced that CFO Andrew Findlay bought 3,500 shares at a value of £40K. He now owns 33,916 shares.

Overall then this has been a strong year for the group. Profits were up, net assets increased and the operating cash flow improved. There was a reduction in free cash, however, which didn’t cover the dividends. The markets are still quite healthy but there does seem to be some slow down. The group has benefited from some of their rivals going out of business or encountering other problems. The ancillary revenue is doing particularly well due to new bang segmentation and some other stuff. Costs have risen, however, mainly due to the increased disruption that the industry seems to be experiencing, along with the Tegel acquisition.

Tegel has obviously been dilutive this year but hopefully it will start contributing soon. The holidays and business travel initiatives have potential and the DHL ground handling contract really seems to have helped mitigate further on time issues at Gatwick. The company is obviously rather constrained by Brexit, and really doesn’t benefit from weakening sterling but and revenues per seat are expected to reduce in the first half of next year. Still, with a forward PE of 10.2 and yield of 5.4% this seems to be factored in any I am holding on here.

On the 22nd January the group released a trading update covering the most recent quarter. Robust customer demand drove passenger and ancillary revenue growth which was in line with expectations. Underlying revenue per seat was positive but this was offset, as expected, by the impact of last year’s one-off revenue benefits, the dilutive impact of Tegel and new accounting standards delaying the recognition of revenue. The group has made good progress with its cost and operational performance but both were affected by the impact of drone activity at Gatwick over Christmas.

In the first half of 2019, booking levels remain encouraging despite the lack of clarity around Brexit. Second half bookings continue to be ahead of last year and their expectations for the full year headline pre-tax profit are broadly in line with current market expectations.

Total revenue in Q1 increased by 14%. Passenger revenue was up 12% and ancillary revenue increased by 20%. Passenger numbers increased by 15%, driven by an 18% increase in capacity, albeit this was slightly lower than expected due to late A321 deliveries from Airbus. Load factor decreased by 2 percentage points to 89.7%, due to the one-off increase in prior year late demand and the dilutive effect of Tegel.

Total revenue per seat decreased by 4.2% at constant currency, affected by an increase in underlying revenue per seat of 1.5% due to robust underlying demand and disciplined capacity growth by competitor and continued growth in ancillary revenue per seat through better bag and allocated seating sales. This was offset by the dilutive effect of Berlin Tegel, last year’s competitor bankruptcies and Ryanair cancellations, the £8M impact of the change in accounting standards, and the £5M impact from the drone issue at Gatwick.

The group’s underlying cost performance has been solid and in line with expectations, before the impact of the drones at Gatwick. Headline cost per seat excluding fuel at constant currency increased by 1% reflecting a £10M cost impact of the drones at Gatwick, the annualisation of crew pay deals, and ownership costs reflecting new aircraft and some additional leasing costs resulting from late Airbus deliveries.

The group has entered into another planned sale and leaseback arrangement for ten A319 aircraft which has generated £120M in cash and further facilitates the fleet management strategy. Six were completed in the quarter and a further four were finalised in January. This is currently expected to lead to a small loss on disposal.

The group is well prepared for Brexit. They now have 130 aircraft registered in Austria and has made good progress in ensuring they have a spare parts pool in the EU and in transferring crew licenses.

Going forward, despite the consumer and economic uncertainty created by Brexit, demand currently remains solid and forward bookings for the period after the end of March are robust. For the full year 2019 the group expects capacity to grow by 10%. Revenue per seat in the first half is expected to decrease by mid to high single digits reflecting a larger than previously anticipated phasing impact from H1 to H2 from the impact of new accounting standards and the shift of Easter into H2, both of which are expected to have a negative impact of £50M each which will reverse in the second half. Due to a more competitive market in Berlin and constraints on their ability to deliver network optimisation as quickly as expected, they now expect to make a loss in Berlin in 2019.

Full year headline cost per seat excluding fuel at constant currency is expected to be flat and the full year fuel bill is expected to be £10M to £60M higher. Forex movements will likely have a £10M adverse impact on pre-tax profits and overall the group’s expectations for the full year are broadly in line with market expectations.

On the 7th February the group released a trading update where they stated that they had made a good start to 2019.

On the 13th February the group confirmed that they were in discussions with Ferrovie dello Stato Italiane and Delta about forming a consortium to explore options for the future operations of Alitalia.

On the 8th March the group confirmed that Chief Commercial and Strategy officer Robert Carey acquired 7,500 shares at a price of £88.6K.

On the 18th March the group announced that discussions regarding the consortium to bid for Alitalia had been stopped.

On the 1st April the group released a trading update covering the first half of the year when they expect to deliver a performance in line with guidance with a loss of £275M before tax. Revenue is expected to grow by 7.3% with seat capacity increasing by 14.5% as they complete the annualisation of their flying at Berlin. Revenue per seat declined by 7.4%. Underlying revenue is expected to be positive, offset by the impact of IFRS 15, the move of Easter into the second half, the dilutive impact of Tegel and the prior year impacts from the Monarch and Ryanair problems.

Headline costs are expected to increase by 18.8% due to increased capacity, higher fuel costs and a modest increase in cost per seat. Headline cost per seat excluding fuel is expected to increase by 1.4%. It is expected that the fuel bill will be around £37M higher and forex will have an £8M adverse impact.

While the group will deliver first half results in line with expectations, macroeconomic uncertainty and many unanswered questions surrounding Brexit are driving weaker customer demand and they are seeing increased softness in ticket yields. Given this uncertainty, the board outlook for the second half is now more cautious. Despite this, revenue per seat is expected to be slightly higher in H2 reflecting a weakening Q3 demand and an expected year on year uptick in Q4 driven by a programme of yield initiatives and an assumption of a more certain Brexit outlook.

There is no change to guidance for full year cost per seat excluding fuel and forex, which is expected to be flat.