Telecom Plus have now released their interim results for the year ending 2019.

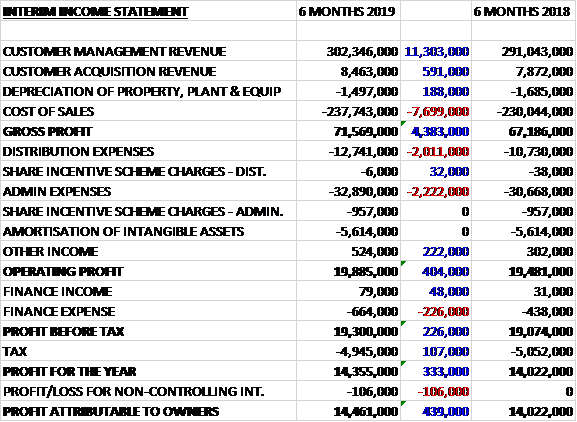

Revenues increased when compared to last year and with cost of sales only increasing by £7.5M the gross profit was £4.4M higher. Distribution expenses grew by £2M and admin expenses were up £2.2M so that after other income grew by £222K the operating profit was £404K higher. Finance expenses were up £226K but tax charges reduced by £107K to give a profit for the period of £14.5M, a growth of £439K year on year.

When compared to the end point of last year, total assets declined by £43.6M driven by a £47.5M fall in prepayments and accrued income, a £5.6M decrease in the energy supply contract and a £2.2M fall in inventories, partially offset by a £4.6M growth in cash and a £4.4M increase in receivables. Total liabilities also declined during the period as a £10.1M growth in bank loans was more than offset by a £50.8M decrease in accrued expenses and deferred income. The end result was a net tangible asset level of £39.9M, a decline of £2.2M over the past six months.

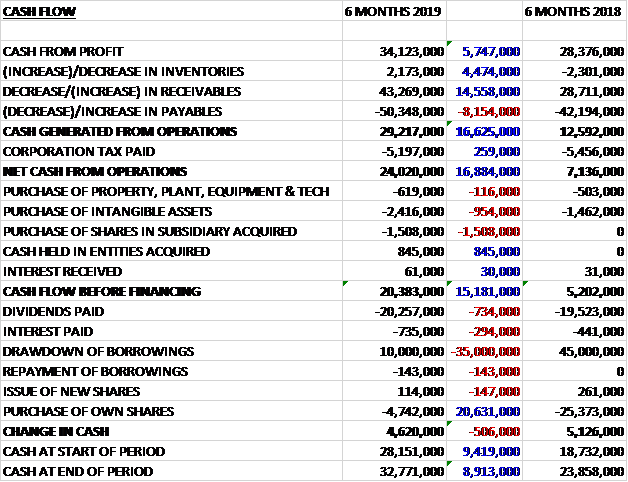

Before movements in working capital, cash profits increased by £5.7M to £34.1M. There was a cash outflow from working capital but this was lower than last time and after tax payments declined by £259K the net cash from operations was £24M, a growth of £16.9M over the past six months. The group spent £619K on fixed assets, £2.4M on intangible assets and a net £663K on acquisitions to give a free cash flow of £20.4M. This only just covered the dividends of £20.3M but the group also purchased £4.7M of their own shares and paid out £735K in interest. After a £10M drawdown of borrowings, there was a cash flow of £4.6M and a cash level of £32.8M at the period-end.

The growth in revenue was slightly above the increase in service numbers with the impact of higher energy prices being largely offset by a continuing decline in average energy usage due to warmer weather and the impact of energy efficiency initiatives. There was a 0.5% increase in gross margins due to improved commercial terms from their key suppliers and industry wide energy price increases.

Admin expenses grew by £2.2M due to a growth in the volume and range of services, higher technology costs as they accelerate their programme to update their core CRM systems, the costs associated with rolling out smart meters, higher regulatory costs and annual inflation-linked increases in staff pay.

In the Energy market, rising commodity, regulatory and distribution costs have led to a significant narrowing of the gap between the Big 6 and the bottom of the market and is expected to narrow further once the price cap takes effect in January. In spite of this reducing gap, customer switching has reached record levels with industry churn now exceeding 20% per annum with significant variation between suppliers (the group has a churn of 12%). As a result some independent suppliers are now struggling to meet their financial obligations with a number having withdrawn from the market.

During the period the group continued their smart meter rollout programme, taking the installed base to 29% of their residential meter portfolio, although this is below where they had planned to be due to challenges with getting their third party meter operators to deliver the agreed schedule. As a result they have established their own licensed meter operator to implement the programme more efficiently. This new venture is on track to install its first smart meters before Christmas with a rapid ramp up in volumes over the course of the coming year. The rollout of second generation smart meters has been subject to further delay but volume installations are expected to start in Q1.

Since acquiring Glow Green in May they have secured improved commercial terms with a number of their main suppliers, supported their move to a larger warehouse and started work on improving the effectiveness of their online customer acquisition process. In addition they have recently introduced a new CRM platform.

These were all prerequisites to supplying boilers directly to their members, being able to maintain and service them and to launching an integrated boiler care product, all of which have significant business potential. Their plans for moving into these markets are progressing well and they should launch these services during the course of next year.

The penetration of Telecoms amongst their membership base has more than doubled over the past six years to 38%. As a result of a number of improvements they made to their tariffs in the Spring, over 70% of new members applied for a mobile service from them during the first half. As average fixed line call revenues follow a gentle downward trend, they continue to ensure that growing their mobile base remains a priority. In a broadly flat overall market, they were pleased to achieve a net increase of 10,000 broadband services, taking their installed base to over 293,000. Of these, around 33% are currently taking one of their fibre options compared to 60% amongst new members.

They remain encouraged by the high level of interest in their home insurance service and have deployed a fully automated marketing and quote & buy system which is delivering conversion rates approaching 30%. As a result they have now issued around 10,000 policies which recent sales running at an annualised rate that will see this total double over the next year. Early indications show that the book they are building is of a high quality with a loss ratio well below the industry average. This should enable then to expand their insurance panel and further increase the current conversion ratio.

Around 97% of policy holders are subsequently renewing their insurance at expiry which gives the board confidence that over time this new service will generate significant value. Their focus in 2019 is to continue building scale for their home insurance product whilst working towards launching other complementary insurance products, starting with boiler cover.

The group saw a particularly strong demand for their Cash Back card during the period. This was relaunched in March, offering savings to members and is proving to be an effective acquisition tool and is one of the key drivers of their performance during the first half.

In May the group acquired 75% of Glow Green Ltd, a small supplier and installer of domestic gas boilers and warranty plans for the consideration of £1.5M plus £500K repayable working capital loan facility. They also acquired 75% of Cofield Ltd as part of the transaction. Cofield was under the same ownership and is a small online retailer of central heating equipment to the plumbing industry.

Going forward, growth in the first half was encouraging and the board look forward to the introduction of the energy price cap at the end of 2018 which will further improve their competitive position. They are on track to deliver growth in customer and service numbers that are materially up on last year and expect adjusted pre-tax profit to remain in the range previously guided at £55M to £60M. It has been a number of years since the overall outlook has appeared this positive.

At the current share price the shares are trading on a PE ratio of 36.7 which falls to 24 on the consensus full year forecast. After a 4.2% increase in the interim dividend the shares are yielding 3.6% which increases to 3.7% on the full year forecast. Net debt at the period-end stood at £16.9M compared to £11.2M at the year-end.

Overall then this seems to have been a decent period for the group. The net asset level did deteriorate somewhat but profits were up and the operating cash flow improved with the free cash flow covering the dividends. The price cap being introduced next year should help further improve the group’s competitive position and things are looking rather rosy. The shares aren’t cheap though with a forward PE of 24 and yield of 3.7% and they are looking just a bit expensive for my tastes.

On the 17th April the group released a trading update covering the year. Full year pre-tax profits are expected to be towards the lower end of previous guidance at around £56M. This reflects the impact of a warm winter and the Ofgem price cap and modest initial losses associated with the expansion into related areas such as Glow Green and Boiler and Home Cover insurance. Net debt increased from £11.2M to £38M reflecting higher working capital requirements associated with changes to the phasing of certain energy industry payments, higher technology investment, smart meter rollout costs and the share buyback. A further modest increase in working capital is anticipated over the course of the coming year.

The board are encouraged by the profit outlook for the current year. The combination of accelerating growth in customer numbers and a small increase in their gross margins due to the improved supplier agreement with npower, mean that they expect profits of between £60M and £65M for 2020.

They saw an acceleration in customer growth during the course of the year, notwithstanding a significant and persistent gap between the low introductory fixed price deals available and standard variable prices charged by the big 6. Although this gap narrowed in Q4 following the introduction of the Ofgem price cap, it has since started to widen again, driven by the questionable pricing strategy adopted by some independent suppliers who continue to sell energy at zero margins.

Customer numbers increased by 4% and service numbers by 8.2%. In addition, they saw a further improvement in the quality of the customer base with 26.6% of their membership having now switched all their core services to Telecom Plus. Their own churn fell slightly and remains well below the levels of many other independent suppliers.

This growth has been driven by growing activity in their distribution channel with increasing numbers of partners taking advantage of their Quick Income Plan which enables them to combine the benefit of receiving meaningful introductory payments from recommending their services and building a long term residual income for the future.

The Boiler and Home cover insurance product they launched last month has been designed primarily as a customer acquisition and retention tool rather than a profit centre. Early sales are encouraging with around 150-250 policies per week. The home insurance product is now making a modest contribution to profits which will become increasingly significant as the penetration of policies within the member base continues to grow.

Since the acquisition of the 75% holding of Glow Green, losses have been running slightly higher than expected (£1M) but they expect to reach break-even within the next few months. Since making the investment they have assisted them in securing improved customer financing and boiler procurement terms, upgrading their financial controls, optimising their marketing spend and implementing a new CRM platform.

The proposed merger between Eon and Innogy created an opportunity to initiate discussions with npower on the terms of their current wholesale energy supply arrangements with them which has resulted in a number of changes to the previous arrangements including an overall modest improvement to the commercial terms, including a small increase in the current level of discount received; the ability for them to switch from their current retail-minus wholesale pricing structure onto industry standard wholesale price arrangements from 2024; and a relaxation in the previous exclusivity obligations, giving them the freedom to source energy in the open market. In return they agreed to delete their termination rights on any future change of control in the ownership of npower.

Going forward the board anticipate that the momentum that has been building over the past year will continue, with growth in customer and service numbers for the year ahead reaching 5% and 10% respectively. Despite the higher costs associated with multi-service customers, they are hugely encouraged by the continuing high proportion of new members choosing to switch all their services to them.