Easyjet has now released its interim results for the year ending 2016.

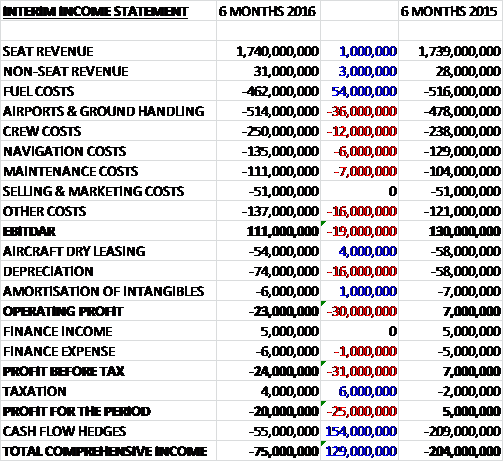

Revenues were broadly flat when compared to the first half of last year but costs increased as a £54M decline in fuel costs was more than offset by a £36M growth in airport and ground handling costs in Italy and Gatwick, a £12M increase in crew costs reflecting the greater number of flights, a £15M growth in navigation and maintenance costs and a £16M increase in other costs relating to disruption costs following events in Egypt, Paris and Brussels combined with industrial action and adverse weather conditions, to give and EBITDAR some £19M below that of last time. Depreciation increased by £16M due to the acquisition of new aircraft and a decrease in the number of leased aircraft in the fleet, but tax was down £6M which meant that the loss for the period was £20M, a detrimental movement of £25M year on year although it is worth remembering that Easy Jet traditionally reports losses/lower profits in the first half of the year and also at constant exchange rates, the group would have recorded a profit of £5M during the period, flat year on year.

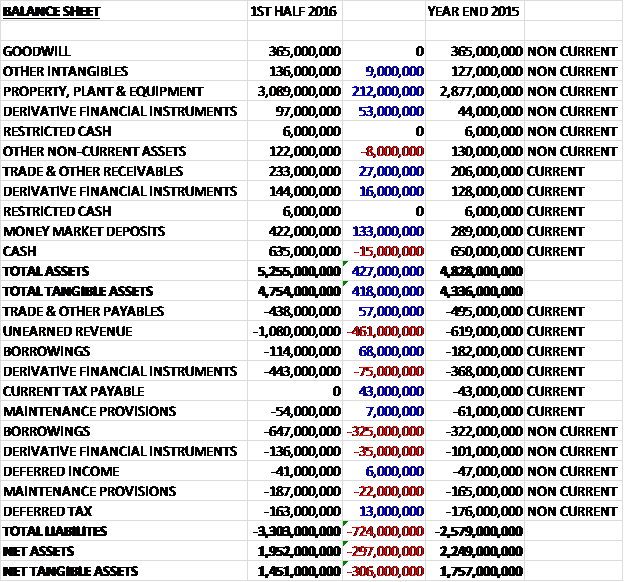

Total assets increased by £427M when compared to the end point of last year driven by a £212M growth in property, plant and equipment mainly relating to the ten new aircraft, a £133M increase in money market deposits, a £69M growth in derivative financial instruments and a £27M increase in receivables. Total liabilities also increased during the period as a £461M growth in unearned revenue relating to flights paid for by customers but not yet flown with the increase due to the seasonal nature of the airline industry, a £110M increase in derivative financial liabilities relating to the adverse mark to market movement on jet fuel forward contracts, and a £257M growth in borrowings was partially offset by a £57M decline in payables and a £43M fall in current tax payable. The end result was a net tangible asset level of £1.451BN, a decline of £306M over the past six months.

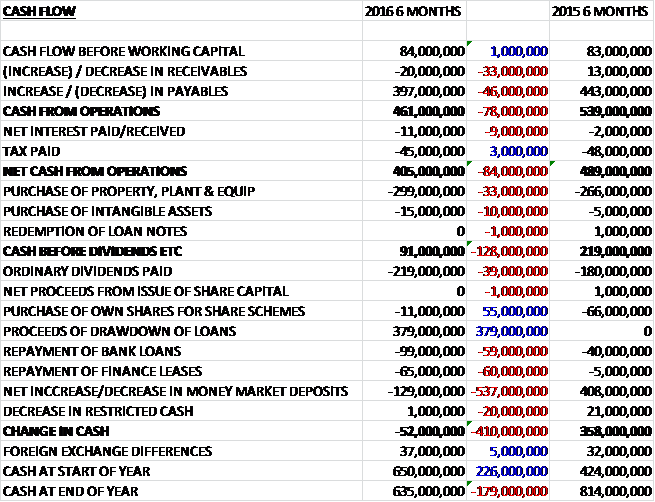

Before movements in working capital, cash profits were broadly flat at £84M. A large increase in payables meant that the net cash from operations came in at £405M but the cash inflow from working capital was much lower than last time primarily due to unearned revenue with the variance arising due to differences in the timing of flight schedule releases and the Easter school holidays, so this represented an £84M decline year on year. The group spent £299M on property, plant and equipment including the acquisition of ten aircraft, the purchase of life-limited parts used in engine restoration and pre-delivery payments relating to aircraft purchases, along with £15M on intangible assets to give a free cash flow of £91M. This didn’t cover the £219M spent on dividends and the group drew down on their loans and after £65M was paid back on finance leases and there was a £129M net increase in money market deposits, there was a cash outflow of £52M and a cash level of £635M at the period-end.

Underlying consumer demand has been strong with UK beach traffic providing a healthy start to the half and the group’s biggest ever ski season helping to deliver increased passenger numbers. Fares decreased by 6%, however, as the benefits of lower fuel costs were passed on to customers although cost controls helped maintain margins.

Revenue per seat decreased by 4.2% year on year on a constant currency basis and by 6.6% on a reported basis to £51.29 and the load factor remained flat at 89.7%. It is also worth noting that Easter fell during the period this year which is not always the case. There was a 1.3% impact to revenue per seat due to the cancelation of flights to Sharm el Sheikh and a 2.7% impact due to the fall in demand after the terrorist events in Paris. The decline in fuel costs also led to a reduction in revenue per seat as competitors reduced prices.

Cost per seat excluding fuel grew by 0.5% and decreased by 4.3% including fuel on a constant currency basis with costs decreasing by 5% on a reported basis. This decrease was due to lower fuel costs with increased disruption costs offset by fleet up-guaging and cost cutting initiatives. There was an adverse forex impact of £33M, mainly due to the weaker Euro exchange rate on routes in Europe with £4M relating to balance sheet revaluations. Disruption events impacted the cost per seat by 65p and there were also additional costs due to increased airport charges offset by volume deals on airport contracts, savings as a result of renegotiated airport and ground handling contracts and a new maintenance contract together with unit cost savings arising from the fleet upgrades.

Demand for European short haul travel remains strong with the market growing by 6.4% year on year. This growth looks set to continue as a result of improved economic conditions and a lower oil price. In the second half of the year the board expects demand increase to slow somewhat, up 5.3%. The group’s competitors increased capacity by 6.9% in its markets and Easy Jet grew capacity by 7.4% in these markets.

In the UK the group increased its capacity by 9%, investing in core routes and markets such as London to Scotland, increasing their share of the UK regional market to 20% and maintaining their share of the total London market by 21%, with particularly strong growth at Luton. In France they increased capacity by 6.5%, almost double the rate of growth in the overall market. This was partly driven by upgrading the fleet from A319s to A320. The terrorist attacks in Paris significantly impacted trading, particularly on City to City travel but the group will operate thirty new routes during the summer and are adding two new aircraft in Lyon, as well as a night stop in Bordeaux.

In Switzerland the group increased capacity by 8% with a significant benefit from ski traffic, against overall market growth of 5%. In Italy, a new base was opened in February in Venice with four aircraft to serve the region’s large business community and major inbound market. They also added major business flights from Milan to London, Amsterdam and Paris. Whilst they still expect to fly over two million passengers to Rome this year, the aircraft previously based at the airport have now been transferred to Venice, Naples and Milan.

In Germany the group increased capacity by 7% against competitor capacity increases of 5%, maintaining load factor and consolidating their position in Berlin and Hamburg. New routes were added to reinforce a strong city network and brand awareness continues to increase. In Portugal they increased capacity by 21% as they continued to establish the Porto base. In Spain, they opened a new base in February in Barcelona and three aircraft was based there at the period-end. Another new base in Palma Mallorca is planned for 2017. In the Netherlands, they increased capacity by 27%, focusing on adding frequencies to existing destinations and capturing first wave demand from business passengers.

The group have a number of initiatives in order to keep control on costs. They are gradually upgrading their fleet, moving from 156 seats on an A319 to 186 seats on an A320 Neo aircraft which is expected to deliver a cost per seat saving of around 13% to 14% with the introduction of the new aircraft occurring from June 2017. As of the end of the first half of the year, the total fleet comprised 247 aircraft and during the period they took delivery of ten A320 aircraft with four A319s being retired. In the second half of the year, no aircraft will leave the fleet and a further ten A320 deliveries are planned so at the year-end the fleet should consist of 144 A319s and 113 A320s.

On time performance was 82%, impacted by French Air Traffic Control strikes, capacity restrictions from Brest ATC and ongoing congestion at Gatwick which has a major knock on impact on the rest of the network. This was in addition to cancellations and delays due to terrorism related events at Sharm el Sheikh and Brussels. During the period the group cancelled 1,374 flights compared to 683 flights in the first half of 2015. They are putting in place a number of initiatives in order to improve on time performance in future which include the roll out of auto bag drop, working with air traffic control to better manage ground and airborne congestion, enacting infrastructure improvements at Gatwick that include a new crew room and centralised ops room. Increasing investment in maintenance and resolving baggage handling arrangements with the Gatwick supplier.

The group have recently been targeting business passengers which grew by 6% ahead of overall business capacity growth of 4%. They have seen good momentum as they develop their capability further and sales of the dedicated business fares increased by 10%. They signed new three year distribution agreements with Sabre and Travelport to continue to leverage sales through global distribution systems. Some 58 new corporate agreements were signed during the period and their first local German Travel Management Company agreement has now been finalised.

Since adding a dedicated group booking capability for bookings of up to 40 passengers, revenue from this segment increased by 163%. Additionally, a third of those booking group travel were doing so for business reasons. The group are also looking at new revenue streams with a recent example being the launch of the Easyjet Holidays website last year. Some potential opportunities include exploring new distribution channels, partner agreements and structures such as connectivity with other airlines.

In the second half of the year the group have hedged some 87% of their fuel requirement at $793 per tonne and in 2017 they have 76% hedged at $626 per tonne with a 10% movement in the fuel price impacting profits this year by $1.5M. The average fuel price during the period was $409 per tonne. They are also susceptible to movements in exchange rates, particularly with the US dollar with a one cent movement impacting profit by £1.3M.

The group has continued to work with the Scottish government on its plans to halve passenger tax and they are campaigning against the recent €2.50 increase in taxes in Italy. Their primary focus on airport charges has been in Spain where charges for the next five years are being set and the company expects there to be no increase; and in Switzerland where the leading consumer body has made recommendations that are now being considered by the government.

The group appear to be susceptible to a potential Brexit vote at the upcoming referendum as European deregulation and being able to fly without restriction across Europe has great benefits for them.

As of the period-end, the group is contractually committed to the acquisition of 176 Airbus A320 family aircraft with a total list price of $15.5BN for delivery in 2016 (10 aircraft), 2017 and 2018 (36 aircraft) and between 2017 to 2022 (130 new generation aircraft).

At the period-end the group had a net debt position of £761M compared to £560M at the same period last year. In February they issued notes amounting to €500M for a seven year term with a fixed annual coupon rate of 1.75% which seems pretty good. To mitigate the foreign currency exposure on the Eurobond, they also entered into cross-currency swap contracts. Changes in the fair value of these derivatives are recorded in the income statement together with any changes in the fair values of the hedged assets or liabilities. They also signed a $500M revolving credit facility with a minimum five year term.

Taking into account the timing of Easter and the effects of terrorism in Brussels, the group expects Q3 revenue per seat to decline by around seven percentage points and revenue per seat on a constant currency basis for the second half of the year to decrease by low to mid-single digit percentage points. They expect cost per seat at constant currency excluding fuel to decrease by about 1% for the year assuming normal levels of disruption. The expected second half cost per seat decrease will primarily be driven by the savings programme, in particular in airport contracts and engineering and maintenance. Including fuel, cost per seat is expected to decrease by 5% in the year.

It is estimated that at current exchange rates and with jet fuel remaining between $350 and $450 per tonne, the fuel bill for the second half of the year is likely to decrease by between £85M and £90M compared to the second half of 2015. On a full year basis, it is expected that the full year fuel bill is likely to decrease by between £170M and £180M with costs estimated at £1.12BN. In addition, exchange rate movements are likely to have around a £20M adverse impact in the second half of the year and a £55M adverse impact for the year as a whole.

Forward bookings are in line with last year and the group is well placed to grow revenue and profit and passenger numbers this year and it is expected that profit for the year will be in line with market expectations which are currently around £721M.

At the current share price the shares trade on a historic PE ratio of just 10.4 and a dividend yield of 3.9% and the group have stated that they will grow the dividend from 40% of post-tax income as it is currently to 50% going forward.

An April the group saw passenger numbers increase by 6.1% year on year with a load factor that declined from 90.8% to 90.4%.

Overall then, this has been a bit of a mixed period for the group. Profits declined, although they were flat at constant exchange rates; net assets fell and the operating cash flow decreased due to timing differences relating to working capital receipts. There was some free cash generated, however, and cash profits were actually flat. Fares have declined due to lower fuel costs being passed on to customers and demand has been effected locally by the terrorist atrocities in Egypt, Paris and Brussels.

Costs have also reduced due to the decline in jet fuel prices, but the group is still hedged at quite a high price and this should come down considerably by next year. They are also benefiting from the move to larger A320 aircraft. The business passenger initiatives seem to be making modest progress and perhaps the big gains there have already been made and going forward the Brexit vote has the potential to be disruptive given their reliance on European markets. In Q3 revenue per seat is expected to fall, although costs should be lower too. At some point, this company will probably be a good investment but I feel there is just too much uncertainty around at the moment.

On the 6th June the group announced their passenger stats for May. Total passengers increased by 5.7% to 6,861,040 and the load factor fell from 91.6% to 91.5%. There were 173 cancellations for the month with French ATC strikes and weather conditions accounting for most of them.

On the 24th June the group released a response to the EU referendum vote. Overall it is confident that it will not have a material impact on its strategy or ability to deliver long term sustainable earnings growth. They have been preparing for this eventuality in the lead up to the referendum vote and have been working on a number of options that will allow them to continue flying in all of their markets.

Their initial focus will be to accelerate discussions with UK and EU governments and regulators to ensure that the UK remains part of the single EU aviation market. This would enable EU airlines to fly freely within the UK and vice versa and allow the group to operate as they do now.

On the 27th June the group announced that the operating environment in May and June has been extremely challenging. To date they have experienced 1,061 cancellations in Q3 due to the impact of continued strike action by French ATC, runway and congestion issues at Gatwick, severe weather and the knock on cancellations across the network. As a result, in June alone there have been over 700 cancellations to date compared to 487 in June last year (mainly relating to the Fiumicino fire).

These incidents, together with the Egyptair tragedy, resulted in some drop off in consumer demand leading to lower yield and impacted Q3 profit by about £28M and had a negative impact on revenue per seat of about 1.6 percentage points. This means that revenue per seat at constant currency in the quarter will fall by around 8.6% compared to the original guidance of 7% as disrupted passengers were allocated seats that normally would have been sold close to departure for a higher yield.

Following the outcome of the EU referendum, the group also anticipate that additional economic and consumer uncertainty is likely this summer and as a consequence it is expected that revenue per seat at constant currency in H2 will now be down by at least a mid-single digit percentage compared to H2 2015. In addition, recent movements in fuel prices and exchange rates are now expected to add about £25M of additional cost in the year to that guided at the half year results stage.

All in all, this is pretty desperate stuff – I am staying out for now.

On the 28th June the group announced that director Chris Brocklesby purchased 2,294 shares at a value of £25K and a day later Chairmen John Barton purchased 10,000 shares valued at £107K.

On the 6th July the group announced their passenger stats for June. Passenger numbers grew by 5.8% to 6.8M and the load factor increased from 92.7% last year to 94.1%. Cancellations nearly doubled to 852, however.

On the 21st July the group released a trading update covering Q3. Passengers carried increased by 5.8% to 20.2M, driven by an increase in capacity of 5.5% and load factor increasing by .3% to 92%. Total revenue per seat decreased by 8.3% on a constant currency basis, however, to £54.54 per seat. Total revenue in the quarter decreased by 2.6% to £1,196BN as increased seat capacity was offset by the impact of overall market capacity and cancellations as a result of significant external events.

In order to combat these issues the group has taken a number of steps. They have optimised their revenue management system. Individual flight profiles have been rolled out which enables the system to be more tailored to individual flight customer demand. Upgrades to the system have further increased its responsiveness to the very dynamic environment as thousands of automated pricing adjustments are being made each day.

They have become the first major European airline to launch an Apple Pay function for bookings and they have increased customer focused propositions such as a 24-hour cancellation capability, a new low deposit offer on holidays and the introduction of premium and European brands inflight which helped to drive a 12% increase in non-seat revenue. Business passengers grew by 9%, helped by 25 new corporate agreements and a higher proportion of business bookings through the mobile channel.

Commercial and operational performance during the period was impacted by the Brussels attack and Egyptair tragedy, significant disruption due to air traffic control strikes and congestion, runway closures at Gatwick and severe weather leading to 1,221 cancellations. June in particular was badly affected, suffering 852 cancellations with eleven ATC strikes taking place in the country.

While these issues have affected the entire industry, EasyJet has been particularly affected due to its high exposure to both London and French airspace. Gatwick has experienced a 350% increase in delay minutes in June due to air traffic and the group sustained further delays as a result of restrictions in the Brest control area.

The cost per seat including fuel reduced by 3.8% at constant currency due to low fuel prices and an underlying cost focus and the group’s cost per seat excluding fuel was broadly flat despite £20M of disruption costs incurred during the quarter. The cost improvements were achieved through maintenance savings, lower navigation charges and a focus on driving overhead cost savings.

Net cash stood at £368M at the period-end compared to £421M at the same point of last year and the group have recently issued a tender for 25 A319s as part of their sale and leaseback programme with strong indications of interest.

In the quarter the group took delivery of six A320 and all new deliveries will be in the 186 seat configuration, delivering a 13% unit cost and fuel savings against the older A319s. From September they will start the process to retrofit the existing A320 fleet which is expected to be completed by the summer of 2018. They will start taking delivery of A320neo aircraft from June 2017 which will drive further fuel efficiency savings.

Following the UK’s decision to leave the EU a team is now mobilised and actively engaging with regulators and government to secure European flying rights. The group has a contingency plan to obtain an EU Airline Operator Certificate in the event that the UK government negotiation does not achieve the desired outcome but they remain committed to the UK.

It is estimated that at current exchange rates and with jet fuel remaining within a $350 to $450 trading range, the group’s fuel bill for the second half of the year is likely to decrease by between £75M and £85M. Exchange rate movements are likely to have a £45M adverse impact.

Going forward, the economic and operating environment remains uncertain following the high levels of disruption and the UK’s decision to leave the EU along with the recent events in Turkey and Nice which have affected consumer confidence. This, combined with industry capacity growth in short haul, continues to have an impact on yields at a peak time of year. About 65% of expected bookings for Q4 have now been secured with booked average revenue per seat declining by around 7.5% at constant currency. As a result of events last week, the revenue per seat trajectory in Q4 remains uncertain and capacity is expected to grow by 6%.

Overall then, the shares now look rather cheap but there is unprecedented uncertainty in the market and now might be too soon to take a position.

On the 28th July the group announced that non-executive director Andreas Bierwirth acquired 1,480 shares at a value of nearly £15K.

On the 4th August the group released passenger stats for July. Total numbers increased by 6.7% and the load factor was up 1.5% to 95.8%. In total there were 350 cancellations compared to 318 in the same month last year. These figures don’t look all that bad to me.

On the 6th September the group announced their passenger stats for August. The total passengers increased by 6.4% and the load factor grew by 0.5pp to 94.9%.

On the 6th October the group released a trading update for the three months to September (Q4). Passenger numbers for the period were a record 22M with a load factor of 93.9% and revenues per seat at constant currency fell by 8.7%. Conditions have been challenging during the period with all European airlines being affected by major disruption, exchange rate fluctuations, terrorist attacks and the low cost of fuel increasing market capacity. During the period the group grew capacity by 6.1%.

Cost per seat excluding fuel on a constant currency basis is expected to decrease by 1.1% for the full year, slightly better than previous guidance. Including fuel, costs are expected to decrease by 4.6%. Significant forex movements since the Brexit cote have had a net adverse impact on Easy Jet with a £90M impact now expected for the year, although the unit fuel bill is expected to decrease by £75.5M.

Going forward, the full year pre-tax profit is expected to be between £490M and £495M and next year capacity is expected to grow by around 8%. About 45% of seats are now sold for Q1, in line with last year. Revenue per seat in Q1 continues to be down year on year and is currently expected to be broadly in line with the reduction seen in Q4.

Cost per seat excluding fuel and at constant currency is currently expected to grow by around 1% in 2017, reflecting increased investment in operational resilience as well as the timing of longer term cost savings. This excludes the impact of a number of aircraft sale and leaseback transactions, plus the one-off costs associated with the set-up of a European AOC and changes to the organisational structure as well as the outcome of ongoing union negotiations.

The group remains committed to its target of flat unit cost per seat in 2019 against 2015, however. The forex headwind will continue into 2017 mainly driven by weaker Sterling against the US dollar affecting the cost of fuel. The total expected impact for the year is expected to be around £90M.

Overall then there is no doubt that these are tough times for airlines like Easy Jet and I am not looking to invest just yet.

On the 4th November the group released passenger stats for October. Overall they increased by 6.9% but load factors declined from 93.3% last year to 90.2% this October.