Wentworth Resources has now released its Q1 results for the year ending 2016.

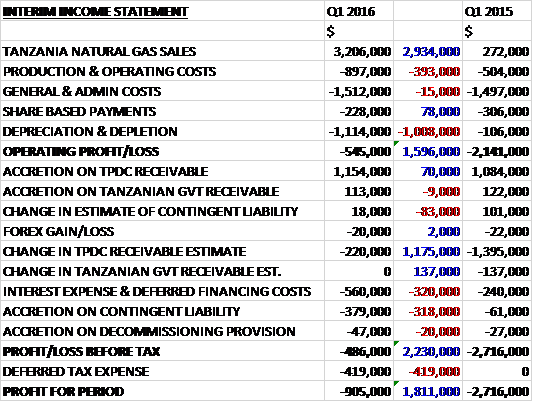

Gas revenues increased by $2.9M when compared to Q1 last year. Production and operating costs were up $393K due to increased field staffing levels to cope with the increase in production volumes, and depreciation/depletion grew by $1M as production levels increased to give an operating loss $1.6M lower than last time. The reduction in the TPDC receivable estimate was $1.2M lower than last time but interest expenses increased by $320K with the accretion on the contingent liability increasing by $318K to give a pre-tax loss some $2.2M better than last time which, after a deferred tax expense was incurred in the quarter, meant that the loss for the period was $905K, an improvement of $1.8M year on year.

When compared to the end point of last year, total assets increased by $927K driven by a $1.7M growth in receivables, a $1.3M increase in cash and a $372K growth in prepayments, partially offset by a $1.7M reduction in the TPDC receivable, a $611K fall in the value of natural gas properties and a $419K decline in deferred tax assets. Total liabilities also increased during the period due to a $1.6M growth in payables. The end result was a net tangible asset level of $136.4M, a decline of $859K over the past six months.

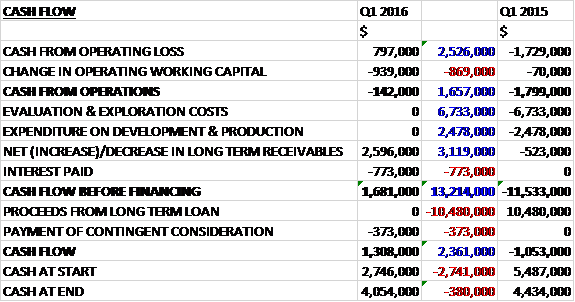

Before movements in working capital, cash profits of $797K represented an improvement of $2.5M on the cash losses of last time. A detrimental movement in working capital meant that there was an operating cash outflow of $142K, however, which was an improvement of $1.7M year on year. There was no capex and the $2.6M receipt on long-term receivables covered the $773K interest payment so that before financing there was a cash inflow of $1.7M. After the payment of contingent consideration, the cash flow for the period came in at $1.3M and the cash level at the end of the quarter was $4.1M.

Commissioning of the four turbines at the newly built Kinyerezi-1 power station continued during the period and the Symbian, Ubungo II and Mtwara power generation facilities were nearing full operational capacity at the end of March. At full operating capacity, Kinyerezi-1 is expected to utilise about 25 to 30MMscf per day of natural gas; Ubungo II and Symbian power plants about 45 to 50MMScf/d; and the Mtwara power plant about 2MMscd/d equating to a total average of between 70 and 80MMscf per day.

At the operating level, the Tanzania business is at a broadly break even stage compared to the $1.7M loss incurred in Q1 last year. During the quarter the Mnazi Bay gas field delivered 47.6MMscf per day, a modest increase over Q4 deliveries of 45.5MMScf/d. In March, deliveries averaged 55.9MMScf per day with production of 64.8MMscf by the end of the month. The wells are performing well and are capable of delivering volumes in excess of current production. The joint venture partners are contracted to supply up to 80MMscf per day for the first eight months after the commercial operations date which is expected to be reached in Q2.

The MB-1 well, which is currently producing just 2MMscf per day, fuelling the TANESCO-owned Mtwara power plant, will be tied into the pipeline infrastructure this year to join the other four wells already connected. The company anticipates gas sales to the pipeline to increase to 130MMscf per day in 2017 as market demand grows and gas deliveries could escalate up to 270MMscf per day should additional exploration success occur on the concession. During the period, minimal work was performed on the expansion of the processing facilities at Msimbati but the company are seeking to advance an exploration drilling programme in 2017, the costs of which are expected to be fully funded from internally generated cash flow.

The Mozambique operations incurred a loss of $155K in the quarter, up from the $114K in Q1 2015. During the period the group reached an agreement with the other partner, state-owned ENH, on assigning the participating interests of the relinquishing parties on the Romuva block. Wentworth were appointed operator and have an 85% interest in development and production of the block.

An appraisal plan has also been agreed which includes re-processing and interpretation of existing seismic data with specific focus on the sands relating to the Tembo-1 gas discovery. Should results of this reprocessing be encouraging, the proposed programme includes potential acquisition of new 2D seismic and, contingent on identifying a suitable appraisal target, drilling activity comprising an appraisal well. The programme is expected to take two to three years to complete, depending on the acquisition parameters and weather conditions.

An issue at this company continues to be the collection of receivables. They do seem to be being paid in a timely fashion by TPDC for the gas sales to the pipeline as the $2.2M owed at the period-end was collected in full in April but the same cannot be said for the gas sold to TANESCO relating to the small gas-fired power plant in Mtwara. They were owed $1.3M which is equivalent to eight months of gas sales and are engaged with TANESCO to try and accelerate payment. There also remains $32.9M outstanding from TPDC for its share of Mnazi Bay costs but this did come down by $2.4M as the group retained gas revenues to offset the receivable which seems as though it is a workable solution. Finally they don’t seem to be any closer to being paid the $6.5M outstanding from the Tanzanian government.

Tanzania elected its fifth president in November and in December a new cabinet was sworn in. The group believes that the re-election of the ruling party and the appointment of experienced individuals to key positions ensures stability and should encourage the continuation of key policies. The new government has placed an emphasis on eliminating wasteful expenditure, improving domestic revenue collection and directing investment to key infrastructure projects.

In the energy sector, the president followed up on his promise to commit funding for construction of the 240MW Kinyerez-2 power station and also pledged to provide funding for the expansion of the 150MW Kinyerezi-1 power station which provide a growth opportunity for the Mnazi Bay joint venture partners.

There group have fully drawn down on their loan facilities. Principal repayments will commence in June with the first of six semi-annual payments of $1M due and in July the first of six semi-annual principal payments of $3.3M will be made. As of the end of the quarter, they had cash on hand of $4.1M and as Q3 progresses, gas volumes are expected to stabilise at over 70MMScf per day. The expected funds from their share of gas deliveries to the pipeline combined with funds on hand and the collection of the long term receivable from TPDC should be sufficient to meet the current and ongoing obligations.

There is no exploration capital commitments and budgeted development capital is limited to the completion of Mnazi Bay infrastructure tying field producing assets to the NNGIP which is will cost around $3M. Current liabilities of $17.6M relate primarily to amounts due to the operators of the assets in Tanzania and Mozambique and principal repayment obligations on the debt.

Overall then this has been a quarter of steady progress for the group. The loss is improving but the company is still not profitable. Net assets reduced slightly and the there was an operating cash outflow, although this was due to working capital movements and there was a cash profit made and after some of the long term receivables from TPDC were received, there was actually a decent amount of cash being generated here.

There was an average of 47.6MMScf per day being generated in the quarter and by the period-end this has increased to 64.8MMScf with the level expected to stabilise at about 70MMscf in Q2 which should provide enough cash to pay back the upcoming $4.4M debt repayments (along with the $4.1M I cash already received – although trade payables also have to be paid). The receivables from TPDC seem to be being recouped and the company is still being paid in a timely manner for its gas sales to the pipeline. As long as this continues, this company seems like a decent investment to me at these levels.

On the 22nd June the group gave an operational update. In Mozambique, government approval for an appraisal plan as how been received. Under the two year appraisal period the group becomes the operator of the Rovuma Onshore concession and increases its participation interest from 12% to 85%. The state owned oil company retains a 15% interest as a carried partner through to the start of commercial operations. In addition, it has the right to acquire a further 15% interest in the concession within 18 months from the data of submission for a development plan for a consideration equal to the proportionate share of past costs incurred.

Implementation of a work programme will commence this year with the reprocessing of about 1,000km of existing seismic data, the cost of which will be funded from internally generated cash flow. Starting in H2 2017, the group plans to acquire a minimum of 500km of new onshore 2D seismic data. The drilling of an appraisal well is expected to occur in 2018 after the identification of a suitable drilling location based on the interpretation of the data.

In Tanzania, production volumes from the Mnazi Bay gas field have been ramping up and peaked at 74MMscf per day during Q2. Volumes were curtailed for a period of time in April, however, due to heavy rains when some natural gas power generation was displaced by hydro generated power.

Furthermore, and of more concern, sales volumes to the pipeline have been maintained at 50MMscf per day since the start of June due to a dispute between Symbion, one of the power plants and TANESCO. It is unclear how long it will be before the dispute is resolved and power generation at the plant resumes and until that time, volumes are expected to remain at this level, meaning production volumes were lower than expected in Q2.

The group is still receiving prompt payment for its gas delivered to TPDC at least, but this news is a set back and I will not be rushing out to buy shares now.