Fairpoint has now released its interim results for the year ending 2015.

Revenues increased when compared to the first half of last year as a £1.1M fall in IVA revenue, a £54K decline in claims management and a £16K fall in debt management revenue were more than offset by a £10.2M increase in legal services revenue. An increase in cost of sales meant that gross profit increased by £4.6M. There was a £1.2M increase in the amortisation of acquired intangibles and other increases in underlying admin expenses were partially offset by the lack of £749k of acquisition costs relating to Simpson Millar and £480K in refinancing costs that occurred last year to give an operating profit of £974K, a positive movement of £1.1M year on year. We then see a decline in the unwinding of the discount on IVA revenues and an increase in the unwinding of the discount on contingent consideration along with a slightly higher tax level to give a profit for the half year of £1M, an increase of £228K when compared to the first half of 2014.

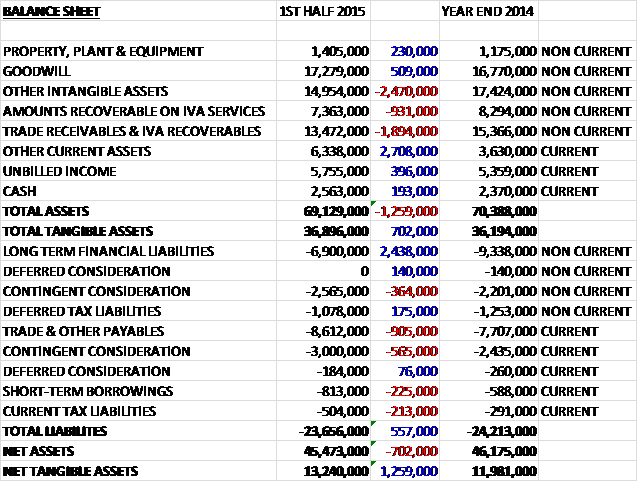

When compared to the end point of last year, total assets fell by £1.3M driven by a £2.5M fall in other intangible assets, a £2.8M decline in trade receivables and a £931K fall in amounts recoverable on IVA services partially offset by a £2.7M increase in other current assets. Liabilities also fell during the year as a £2.4M fall in long term financial liabilities was partially offset by a £905K increase in payables. The end result is a net tangible asset level of £13.2M, an increase of £1.3M over the past half year.

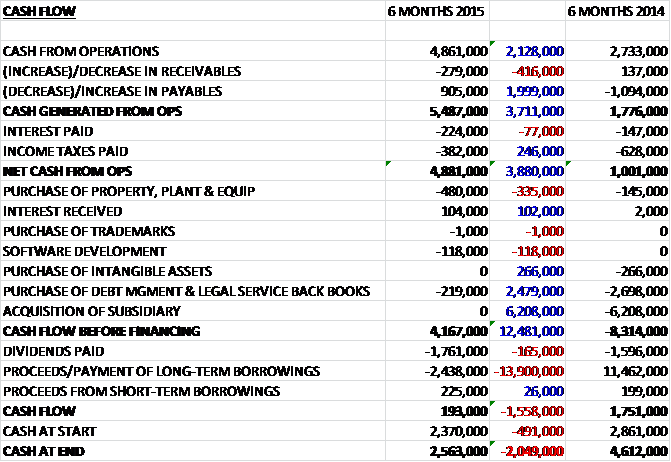

Before movements in working capital, cash profits grew by £2.1M to £4.9M. After a favourable swing to an increase in payables and less tax paid, the net cash from operations came in at £4.9M, an increase of £3.9M. The group then spent £480K on property, plant and equipment along with £118K on software development and £219K on the purchase of debt management and legal service back books to give an impressive looking free cash flow of £4.2M. Some £1.8M was spent on dividends and a net £2.2M was spent on repaying borrowings to give a cash inflow of £193K and a cash level of £2.6M at the period-end.

Market conditions in debt solutions remain challenging and the group continues to take a disciplined approach to marketing expenditure. The volume of new IVA solutions in England and Wales decreased by over 30% to 19,426 in the first half of the year, a reflection of the economic stability in the wider economy. The board believe that these market conditions are likely to continue until bank base rates increase, adversely impacting the financial circumstances of home owners who typically have higher incomes.

The adjusted pre-tax profit at the Legal Services division was £1.4M, an increase of £1.3M year on year with a small improvement in profit margin to 13%. Compared to the full six month period of the prior year when the business was not part of the group, legal services performed well with a single digit organic growth in profits. The group is taking a series of actions with the business including placing prime responsibility for the generation of new customer enquiries into the group marketing function; defining a pricing tariff for over 70 legal products, which will enable the group to communicate a price point for a fixed schedule of services; developing the infrastructure to operate more efficiently, and more recently adding a class leading volume personal injury, conveyancing and travel law business to enhance the product set. Since the acquisition of Colemans, legal services now represent at least 62% of revenues.

At the IVA Services division, revenues fell by £1.1M as a result of fewer new cases due to the general market reduction, and pre-tax profit fell by £300K to £1M. In light of the difficult market conditions, the group has focused on profit margin management through cost control, hence the relatively small fall in profit margin from 19% to 17% despite the reduction in cases. The total number of fee paying IVAs under management at the period end was 16,889 compared to 18,717 last year with the number of new IVAs written in the first half being 795 at an average fee of £3,036 compared to £3,458 last time.

In the DMP Services division, revenues were flat but pre-tax profit fell by £100K to £1.5M. The focus during the period has been on existing clients and engaging with the requirements of the new regulatory regime and the group expect their application for full regulatory permission to be processed during the second half of the year. Due to the regulatory environment, no acquisitions of DMP back books were considered during the period. The total number of DMPs under management at the period-end was 20,730 compared to 21,422 at the same point of last year and adjusted profit margins were down by just 1% to 39%.

Revenue in the Claims Management division was flat and profit fell by £200K to £400K as the business invested in developing new products and services. Claims levels, largely relating to PPI reclaim activity from existing IVA clients, have reached maturity whilst those from the debt management clients are building well.

In August the group agreed a £5M extension to its previous £20M banking facility with AIM, taking the total facility to £25M. The new committed facility comprises a £17M revolving credit facility and an £8M term loan which extends to May 2019.

After the period-end the group acquired Colemans CTTS solicitors and Holiday Travel Watch, a provider of consumer focused legal services with particular class leading expertise in personal injury, volume conveyancing and travel law. The initial consideration was £8M in cash and a further £1M through the issue of 755,516 shares. Further contingent consideration of up to £7M may be payable based on the financial performance of Colemans for the 11 month period ending June 2016 and the year ending June 2017. There will also be £1M in legal, professional and integration costs in the second half of the year. As well as organic growth, the board has indicated that they will continue to look for acquisition opportunities.

The board anticipates that the market conditions in the IVA segment will remain challenging and they will therefore continue to focus on margin management and cash generation. They expect the development of other claims products to mitigate in part the effects of the maturing IVA claims activity. In DMP, the group are focused on existing business whilst their application for full regulatory permission is processed. The debt solutions activities are expected to benefit from their usual seasonally stronger second half, in part due to lower anticipated marketing costs given the subdued markets. As a result of the above factors, along with the initial contribution from Colemans, the board is confident of delivering progress in line with market expectations for the year as a whole.

After a 7% increase in the interim dividend, at the current share price the shares yield 3.7% which rises to 3.8% for the full year forecast. At the end of the half year, before the £8M spent on the acquisition of Colemans, the group has a net debt position of £5.2M compared to £7.1M at the same point of last year.

Overall then, this was a period of change for the group with a solid performance. Profits were up but this was only due to the refinancing and acquisition costs that occurred last year and underlying profits showed a small decline. Net tangible assets were up, however, as was operating cash flow with plenty of free cash being generated. The market for debt solutions is challenging and is likely to remain so until interest rates increased and therefore the decline in IVA profits have had a knock on effect on the claims management profit. The DMP division is also in a bit of limbo until it gains regulatory approval. The fact that the group has managed to anticipate these issues and shift focus onto legal services with some well-timed acquisitions really is a credit to them and were it not for this, profits would have been far more severely affected. The outlook therefore depends somewhat on the performance and integration of these law firms and with a yield of 3.8% I am happy to continue holding.

The chart looks fairly reassuring too, although perhaps it is a little overcooked now.

With regards the acquisition of Simson Millar, there was a provision for the payment of an earn-out of up to £6M based on the financial performance of the business for two 12 month periods ending June 2015 and June 2016 with a maximum of £3M to be payable each year and satisfied by a consideration of 50% cash and 50% shares. The financial performance has exceeded the financial hurdles set for the first earn-out period ending June 2015 so on the 25th September the group paid £1.5M in cash and issued just over 1M new shares at the previously agreed price of 141p per share to the vendors.

On the 27th November the group put out a statement in response to the Autumn Statement by the chancellor. The government’s proposals seek to restrict the ability for sufferers of minor whiplash injuries to claim compensation which is expected to be implemented in April 2017 following a period of consultation. As such the proposed changes have no impact on the board’s expectations for performance in 2015 and 2016. Following the acquisition of Colemans in August, the group has an operational capability designed specifically in anticipation of such changes and therefore they believe they are well positioned to take advantage of these market changes.

Unfortunately this statement does not tell us anything really. To state that the proposed changes will have no effect in 2015 and 2016 when they are expected to be implemented in 2017 is obvious and the fact that they have not mentioned 2017 suggest to me that they are likely to have a serious impact. I am also not sure what to make of the last sentence – there is no detail here at all. I have made good money here and the shares do look a bit cheap but I am considering selling out on the strength of this.

On the 19th January the group released a trading update for year. Overall the group’s adjusted results are expected to show double digit growth against the previous year and are in line with market expectations. This is principally as a result of the continued development of the group’s consumer legal services business.

In legal services, the business has delivered significant double digit increases in segmental revenues and profits whilst making good progress on margin improvement. The division now represents about two thirds of revenues and benefited from the Acquisition of Colemans in August which brings a legal processing centre to the group for the delivery of volume personal injury, conveyancing and travel law.

Following the proposed changes announced by the chancellor in his Autumn statement, relating to small claims limits and whiplash claims and subsequent clarification in the government’s response, the group believes that the changes are intended to focus on whiplash claims relating to road traffic accidents; are subject to consultation; and are expected to follow previous precedent and apply to cases introduced post implementation and not retrospectively. This category business represents about 8% of group’s revenues (although this might increase as the other divisions decline).

In the IVA division, conditions in the debt solutions market remain challenging with the volume of new IVAs in the UK falling by nearly 26% in the first three quarters of 2015. IVA revenues have as a consequence reduced by about 15% and the group has continued to focus on delivering good margins, strong cash generation and avoiding uneconomic new business.

In the DMP division, revenues have declined by about 15% which reflects the absence of acquisition activity in 2015. Following the clarification form the FCA regarding debt management back book acquisitions, the group do not intend to resume activity in this field and will maintain focus on cost control within the division. Within the claims business, as expected revenues have declined significantly compared to last year as the business transitions from maturing IVA PPI claims to newer lines of activity and margins have reduced to reflect this mix change.

Group net debt at the end of the year stood at £13.6M compared to £7.6M at the end of the prior year. During the year the group incurred exceptional acquisition transaction and restructuring costs totalling £1.4M with the former associated with the acquisition of Colemans and the latter with the application for full regulatory permission with the new regulator of DMP activities, the FCA.

Overall then, this is a decent enough update. We can clearly see the legal services business is going to be the driver for growth going forward as the other divisions seem to be declining fast. The fact that about 8% of revenues are affected by the chancellor’s announcement is a bit more helpful but there is no indication of what the effect on profit might be. I suppose I will have to wait for a broker note to include it which is not rally a very fair state of affairs. I am a bit torn here, the business looks cheap but there are clear risks.