Games Worksop has now released its interim results for the year ending 2017.

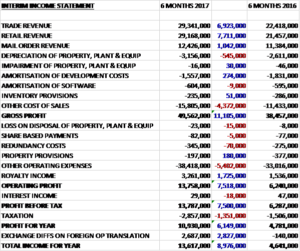

Revenues increased when compared to the first half of last year due to a £7.7M growth in retail revenue, a £6.9M increase in trade revenue and a £1M growth in mail order revenue. Amortisation declined by £265K but depreciation was up £545K and other cost of sales grew by £4.4M to give a gross profit £11.1M above that of last time. Other operating expenses grew by £5.3M but the royalty income increased by £1.7M to give an operating profit £7.5M ahead. After tax charges increased by £1.4M the profit for the period came in at £10.9M, a growth of £6.1M year on year although £644K of this was due to a change in accounting estimates.

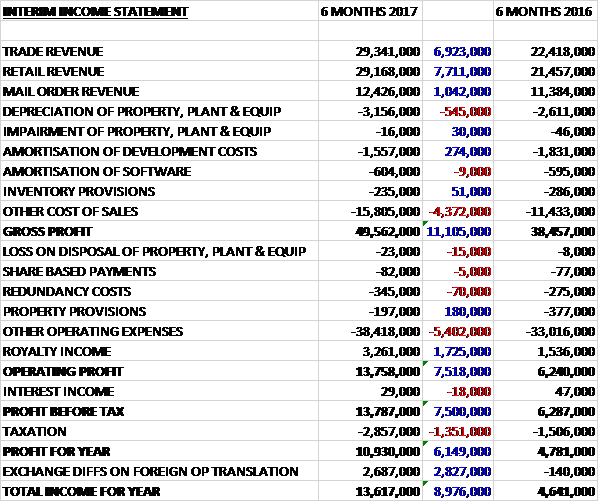

When compared to the end point of last year, total assets increased by £10.4M driven by a £4.1M growth in cash, a £2.7M increase in inventories, a £2.3M growth in intangible assets mostly due to the change in accounting estimates for amortisation, and a £1.4M increase in receivables. Total liabilities also increased during the period due to a £3.9M growth in payables and a £765K increase in current tax liabilities. This all meant that there was a net tangible asset level of £44.6M, a growth of £3.4M over the past six months.

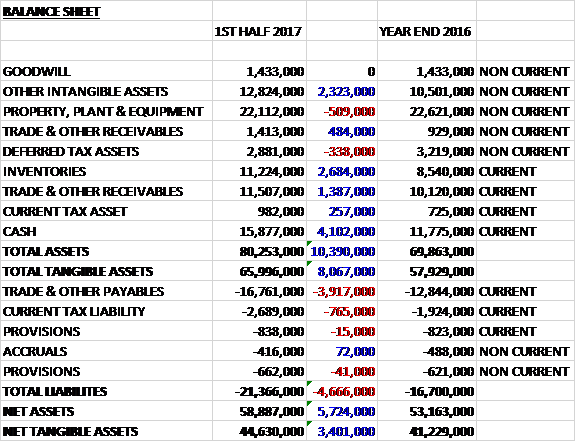

Before movements in working capital, cash profits increased by £7.5M to £19.1M. There was a small cash inflow from working capital compared to an outflow last time and after tax payments increased by £600K the net cash from operations was £18.2M, a growth of £10.5M year on year. The group spent £2.5M on fixed tangible assets, £1.2M on software and £3.2M on product development to give a free cash flow of £11.4M. This easily covered the £8M paid out in dividends to give a cash flow of £3.3M and a cash level of £15.9M at the period-end.

It is worth noting that of the £5M growth in operating profit before royalty payments, £3M was due to favourable forex movements with the constant currency figure being a growth of £2M which is still good but not quite as stellar as it first seems. The group does not hedge against currency movements so they received the whole benefit from the weaker sterling.

The operating profit in the trade division was £8.8M, a growth of £3M year on year with strong growth in revenues from all regions and the number of trade outlets increased by 60 accounts.

The operating loss in the retail division was £2.4M, an improvement of £683K when compared to the first half of last year with growth in sales from all regions. The group opened 17 stores including their first for some time in Singapore, Malaysia and Hong Long. After closing eight stores, their net number of stores at the end of the period is 460. The recruitment of new store managers remains a key area of focus.

The operating profit in the mail order division was £6.7M, an increase of £420K when compared to the first half of 2016. The Made to Order and Last Chance to Buy web store initiatives, aimed at ensuring customers have access to the broader range, have performed well.

The operating profit in the product and supply division was £6.1M, a growth of £1.4M year on year with £798K of that increase due to the change in accounting estimates for the amortisation of development costs and the depreciation of moulding tools. The group launched new editions of the White Dwarf Magazine and Blood Bowl game, the first of many new products from the specialist design studio. Both of these have sold through well. The group made £3M in royalty payments, an increase of £1.8M when compared to the first half of last year.

The capital expenditure contracted but not yet incurred is £996K which includes the replacement of the local area network for the HQ in Nottingham and tooling and machinery spend. It is worth noting that the group are still part way through the ERP change and this complicated project has the risk of widespread business disruption of it is not implemented well. Another risk is that they are changing their mail order warehouse system which carries risks associated with the transition.

At the current share price the shares are trading on a historic PE ratio of 19.9 but this doesn’t take into account the out-performance so far this year and the consensus forecast going forward for 2017 is 12.3. After an increase in the dividend the shares are now yielding 5.4% which increases to 6.6% for the full year. At the end of the period the group had net cash of £15.9M compared to £7.8M at this point of last year.

On the 17th January the group released a trading update covering the Christmas period to mid-January. They saw a significant increase in sales and profits compared to the same period last year and they believe profits for the year are likely to be above market expectations. Profits have further benefited from the continuing favourable impact of the weaker pound but the board remains aware that there is some uncertainty in the trading periods ahead for the rest of the year.

Overall then this has been a good period for the group. Profits increased, net assets grew and the operating cash flow increases with a decent amount of free cash being generated. All operating sectors improved, although it should be noted that the group really benefited from the weak pound and more than half of the growth has come from currency movements. Nonetheless the performance of the trade and royalty sectors looks very impressive. The forward PE of 12.3 and dividend of 6.6% make the shares look like they are still good value to me with the proviso that should sterling appreciate again, much of this would be reversed.

On the 6th March the group released a trading update where they stated that the sales and profit growth discussed in the last trading update continues and income from royalties is ahead of expectations. In light of this, profits for the year are likely to be materially above market expectations.

Sales and profits have further benefited from the continuing favourable impact of the weaker pound but the board remains aware that there is some uncertainty in the trading periods ahead.

On the 2nd June the group released a trading update covering the whole year. Sales and profit growth has continued and the board expect sales to be about £158M and pre-tax profits to be above market expectations at at least £38M, both benefiting from the continued weak sterling.