Orosur Mining has now released its interim results for the year ending 2017.

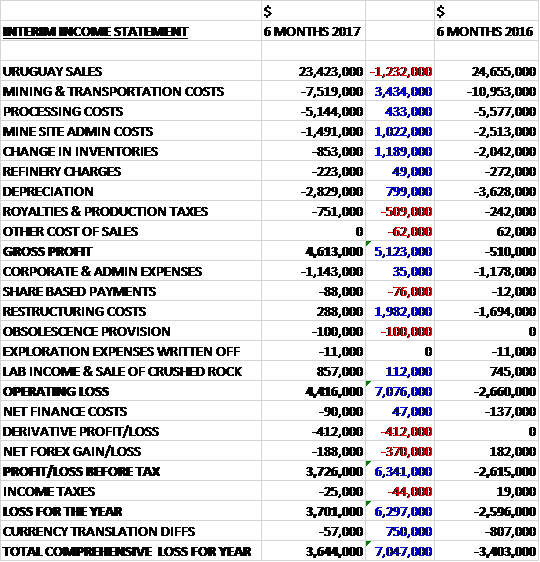

Revenues declined by $1.2M when compared to the first half of last year but cost of sales were considerably lower with mining & transportation costs down $3.4M, mine site admin costs falling by $1M, partly due to the $881K contingency recognised last time relating to a labour claim, a $1.2M positive change in inventories and a $799K reduction in depreciation due to the fact that Arenal had been mostly depreciated by Q2, only being partly offset by a $509K increase in royalty charges reflecting the fact the group has been paying royalties following the ending of the exemption in March 2016. Admin expenses were broadly similar to last year but restructuring costs improved by $2M as some redundancy costs provisioned for previously were not neaded, to give an operating profit of $4.4M, a positive movement of $2.7M. We then see a $412K derivative loss and a $370K swing to forex losses and after tax charges increased by $44K, the profit for the period came in at $3.7M, a positive movement of $6.3M year on year.

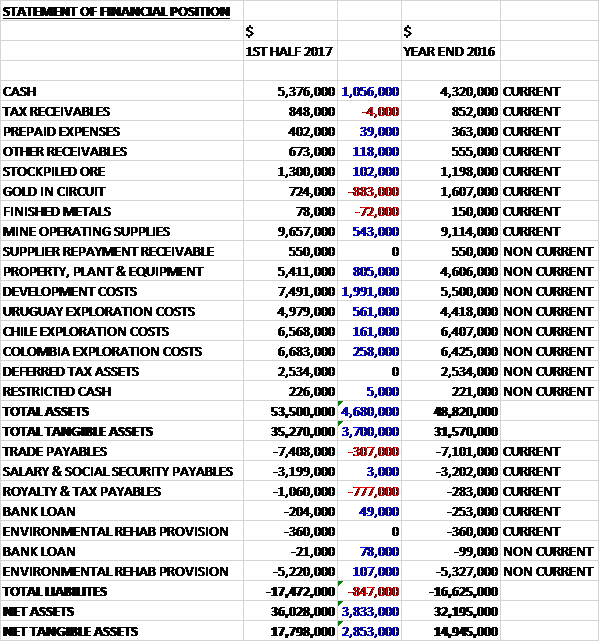

When compared to the end point of last year, total assets increased by $4.7M driven by a $2M growth in development costs, a $1.1M increase in cash and an $805K growth in property, plant and equipment, partially offset by an $883K reduction in the value of gold in circuit. Total liabilities increased modestly during the period due to a $777K growth in royalty and tax payments. The end result was a net tangible asset level of $17.8M, a growth of $2.9M over the past six months.

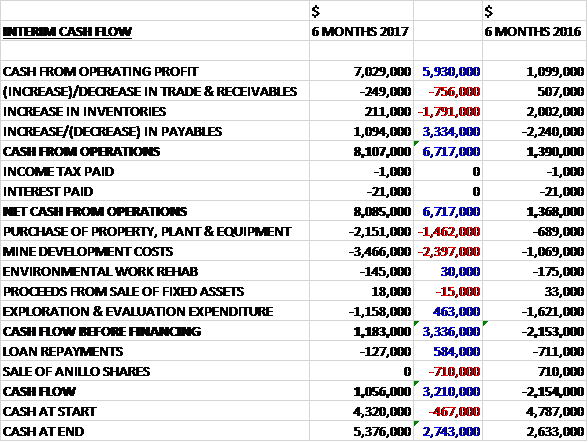

Before movements in working capital, cash profits increased by $5.9M to $7M. There was also a cash inflow from working capital due to an increase in payables and after both tax and interest remained steady there was a net cash inflow of $8.1M from operations, an increase of $6.7M year on year. The group spent $2.2M on property, plant and equipment; $3.5M on mine development costs, $1.2M on exploration (mostly in Uruguay and Colombia) and $145K on environmental work to give a free cash flow of $1.2M. After loan repayments of $127K there was a cash flow of $1.1M in the period and a cash level of $5.4M at the period-end.

The San Gregorio West Underground mine started full production at the end of November, in line with expectations following a safe and efficient transition.

During the period the group sold 17,919 ounces at an average price of $1,290 per ounce compared to 21,670 ounces at $1,127 per ounce in the first half of last year. During Q2, 232,964 tonnes of ore were fed into the plant at an average grade of 0.99g/t to produce 6,852 ounces of gold. This compared to 199,352 tonnes at 1.36g/t to produce 8,172 ounces in Q2 last year. The reduction in grade is largely related to the closure of the underground mining at Arenal Deeps and the start of mining at San Gregorio during the quarter.

The group were able to produce an additional 90,000 tonnes at 1.39g/t from Arenal which was not in the mine plan.

Total cash operating costs were $914 per ounce compared to $858 last time and the AISC for the quarter was $1,345 per ounce compared to $1,095 in Q2 last year. The key driver behind the higher costs was the development of San Gregorio which started production at the end of Q2 2017 as the underground staff and equipment were transferred from the Arenal operation to San Gregorio. Excluding the capex cost, the AISC in the quarter would have been $1,207 per ounce.

During Q2 the group intensified the investment in the construction of the ramp, access and finalised the construction of the ventilation shaft at San Gregorio. In addition they started the construction of the phase 4A of the tailings dam and continued during the current quarter.

At Minerales Cala in Uruguay, in September the group retained a 20% interest and Phase 3 of the option agreement has started and exploration work has been carried on based on a proposed budget and drilling programme submitted by Minerales Cala and Patagonia Gold. In October the group elected not to continue phase 3 expenditures and thus their interests in the project has been diluted and converted to a net smelter return royalty of 2%.

At Gladiator, also in Uruguay, in August, Gladiator announced its intention to dispose of its current interest under the option agreement and in September notified the group of an offer received from a third party proposing a purchase of all of its interest. The group have concluded that the offer is not compliant with the underlying option agreement, however, and cannot be accepted in its current form. In December Gladiator announced that it had executed a binding agreement with a third party to dispose of its interests so the group is in discussions with them regarding the matter and intends to “take all necessary steps to protect their interest in the project”.

At Anillo in Chile, in July the group accepted a request from Asset Chile to extend until March 2017 to allow them to decide on exercising their option to move to phase 2. In September 2016, Asset Chile contributed $120K to cover the minimum expenditure on the project. They have to complete their required contribution to phase 2 (up to $1.25M to fund 5,500m of RC drilling) in order to earn into a 32.5% interest if the group’s share in Anillo. In the event that Asset Chile does not complete the phase 2, they will forfeit their earn-in achievement to date.

At Pantanillo in Chile, in November the group signed the documents for the return of the project back to Anglo American and the transaction will close once they counter-sign. At Talco in Chile, the group’s option to acquire the remaining 75% of the Tellos ownership expired unexercised and they continue to look for opportunities to monetise this asset.

The company’s forecast production guidance for 2017 remains between 35,000 to 40,000 ounces of gold at operating cash costs of between $800 to $900 per ounce. The group incurred higher unit costs in Q2 due to the transition from the Arenal underground to the SGW underground mine which are expected to gradually decrease during the rest of the year.

The group made a loss last year so we don’t have a current PE ratio but at the current share price the consensus forecast is showing a forward PE of 3.2. At the period-end the group had a net cash position of $5.2M compared to $4M at the year-end.

On the 19th January the group announced an update of their exploration activities at the Anza gold project in Colombia. They have completed a preliminary geological model for the Aragon-Pastorere Trend Area of the project and a geological estimate of an exploratory gold potential has been prepared. This ranges between 1.6MT and 2.3MT averaging between 3.2 and 3.7g/t of gold. This estimate is based on current drilling and is expected to grow as future exploration drilling is conducted.

The group believes that the mineralised zones in the APTA continue, both at depth and at the surface, to the north and south of the limited area which has been analysed to date so there is potential for a much larger resource base to be identified. The APTA extends 2km along strike of the vein-like deposit but only accounts for a small portion of the total Anza project which covers about 105km2 in total.

Previous drilling of Anza has shown consistent high grade gold intercepts over significant widths as well as coincident zinc mineralisation. Anza is situated in a well-known geological setting in Colombia already hosting a number of substantial gold projects. It has existing mine and environmental permitting and its existing infrastructure including camps, roads, power and water are in good standing.

During 2017 the group plans to undertake a 15,000 to 30,000m drilling campaign to delineate maiden resources, further define and expand the potential mineralisation for APTA, test mineralisation in undrilled areas of the deposit where strong indications of economic gold occurrences exist and start initial drilling of nearby untested and highly prospective targets.

The site has environmental permits enabling both underground and open-pit mining operations. The Anza project includes two small underground gypsum mines, each of which also have environmental and mining permits granted by the Colombian authorities. Historically the gypsum mines have been operated by a third-party contractor but the group is currently in the process of taking over operatorship. The gypsum permits can be readily expanded, enabling them the ability to fast track permitting for future gold mining operations.

The group believes that Anza has significant upside and they expect the project to take a more prominent standing in their suite of South American gold assets in the months to come.

Overall then this has been a fairly positive period for the group at a time when they switched production to San Gregorio. Profits were up, net assets increased and the operating cash flow grew, aided by higher payables.

Discounting the working capital movement, the group was broadly free cash neutral. The $1,290 selling price is a bit higher than the current price and the AISC of $1,207 is also above the current price of gold, although the group say this will reduce in the second half.

The Anza project looks interesting and the transition to San Gregorio seems to have gone rather smoothly. The current price of gold is a bit on the low side, however, and I would like to see what a whole quarter of San Gregorio production looks like but I am starting to think a forward PE of 3.2 more than accounts for the risks and am tempted to hop back in here.