Games Workshop have now released their interim results for the year ending 2018.

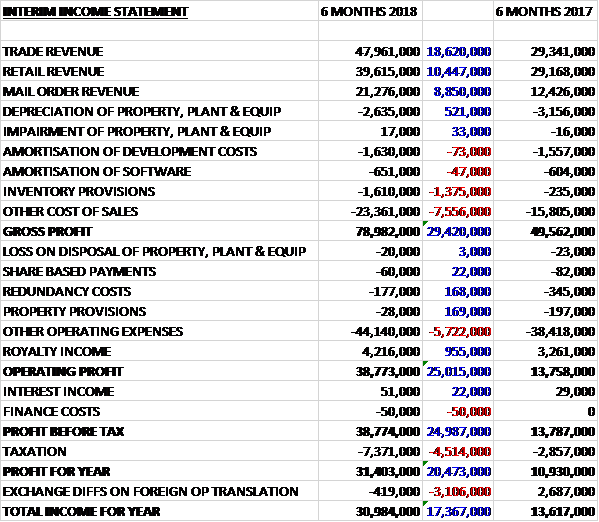

Revenues increased when compared to the first half of last year due to an £18.6M growth in trade revenue, a £10.4M increase in retail revenue and an £8.9M increase in mail order revenue. Depreciation was down £521K but inventory provisions were up £1.4M and other cost of sales saw a £7.6M rise to give a gross profit £29.4M higher. There was a £168K decline in redundancy costs and a £169K fall in property provision but other operating expenses grew by £5.7M before a £955K increase in royalty income meant that the operating profit was £25M higher. Finance costs were broadly similar than last time but tax charges increased by £4.5M to give a profit for the period of £31.4M, a growth of £20.5M year on year.

When compared to the end point of last year, total assets increased by £20M driven by a £10.7M growth in cash, a £3.9M increase in inventories, a £2.8M growth in receivables, a £2.2M increase in property, plant and equipment and a £1.4M increase in intangible assets. Total liabilities also increased during the period due mainly to a £6.1M growth in payables. The end result was a net tangible asset level of £60.1M, a growth of £11.6M over the past six months.

Before movements in working capital, cash profits increased by £24.7M to £43.9M. There was a small cash outflow from working capital and after tax payments increased by £3.7M the net cash from operations was £36M, a growth of £17.9M year on year. The group spent £4.9M on property, plant and equipment, £927K on software, and £2.6M on product development to give a free cash flow of £27.7M. They spent £17.7M on dividends and the cash flow for the half year was £10.9M and the cash level at the period-end was £28.6M.

The operating profit in the trade division was £13.5M, a growth of £4.7M year on year and all key territories achieved growth. On the period the net number of trade outlets increased by nearly 200 accounts. In the period they changed their trade terms with their independent accounts in North America, implementing a minimum advertised pricing policy which was implemented on time and as a direct result supported the growth in this territory in this channel.

The operating profit in the retail division was £1.8M, an improvement of £4.2M when compared to the first half of last year. There was growth in all territories and the group opened a net seven new stores. The key priority has been to continue to offer store managers the appropriate product and sales support to help them recruit new customers, retain existing customers and re-recruit lapsed customers.

The operating profit in the mail order division was £13.6M, a growth of £7M when compared to the first half of 2017. Sales in the online shops were up 71%. They continue to improve the online store shopping experience and functionality of the store and the new website homepage, the newsletters and personalisation of page content remain an area of focus.

Sales of digital publications through Apple continue to grow, up 22%. In addition, the last six months saw the group launch their digital titles onto Amazon and release their Black Library audio range onto Audible. This has increased exposure to new customers and will help the group recruit as they move into next year and beyond. The operating profit in the product and supply division was £17.9M, an increase of £11.5M year on year. The royalty income was £3.8M, a growth of £805K when compared to the first half of last year.

Over the past six months the group have doubled the number of customers interacting them on social media. They have supported these customers with daily content for Warhammer: Age of Sigmar and Warhammer 40,000, and increased their video output to more than one video every day. They have also continued to develop the community website and created new brand content sites.

Going forward, sales for the month of December have also shown good growth trends.

After an increase in dividends the shares are yielding 4% which increases to 5.5% on the full year consensus forecast. At the current share price the shares are trading on a PE ratio of 23 which falls to 12.5 on the full year forecast.

On the 5th February the group released a trading update where they stated that the good growth trends have continued to the end of January. Sales and profits in the year to date are therefore slightly above expectations.

Overall then this has been a very strong performance from the group. Profits were up, net assets increased and the operating cash flow grew with plenty of free cash being generated. All divisions performed well and it is quite hard to determine exactly what the group are doing better than before, with perhaps improved online engagement being decisive? The second half of the year has continued strongly and with a forward PE of 12.5 and yield of 5.5% these shares don’t look expensive yet to me and I continue to hold.

On the 22nd January the group announced that head of product and supply Max Bottrill sold 550 shares at a value of £13.7K. He still owns 10,803 shares.

On the 4th May the group released a trading update where they stated that the good growth trends have continued to the end of April/ Sales and profits for the year to date are therefore slightly above expectations.

On the 8th June the group released a trading update covering the year as a whole. The sales and profit growth reported on before has continued to the end of the year across all channels. The board expect pre-tax profit to be at least £74M with licensing royalties at around £10M. They are paying their staff a bonus of £5M.