Gem Diamonds has now released their interim results for the year ending 2017.

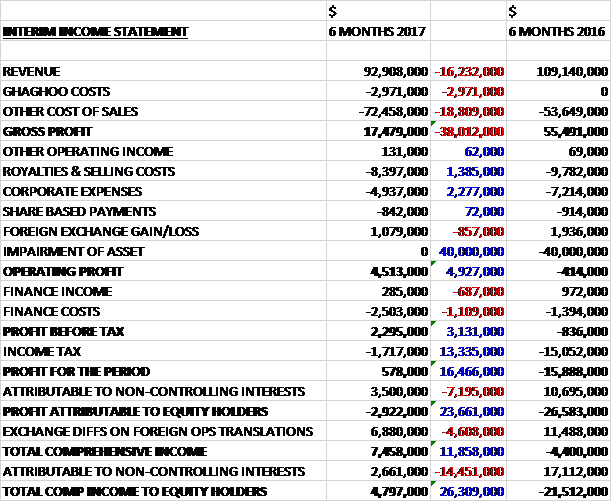

Revenues declined by $16.2M when compared to the first half of last year. We also see one-off Ghagoo costs of $3M and other cost of sales increase by $18.8M, mainly relating to an increase in waste stripping amortisation costs due to the mining mix, to give a gross profit $38M lower. Royalties and selling costs declined by $1.4M and corporate expenses were down $2.3M, however. We also see no asset impairments, which cost $40M last time so the operating profit increased by $4.9M. Finance costs grew by $1.1M and finance income declined but tax charges reduced by $13.M to give a loss for the half year of $2.9M, an improvement of $23.7M year on year. This isn’t the whole story clearly, however, as excluding last year’s $40M impairment, the performance was much lower.

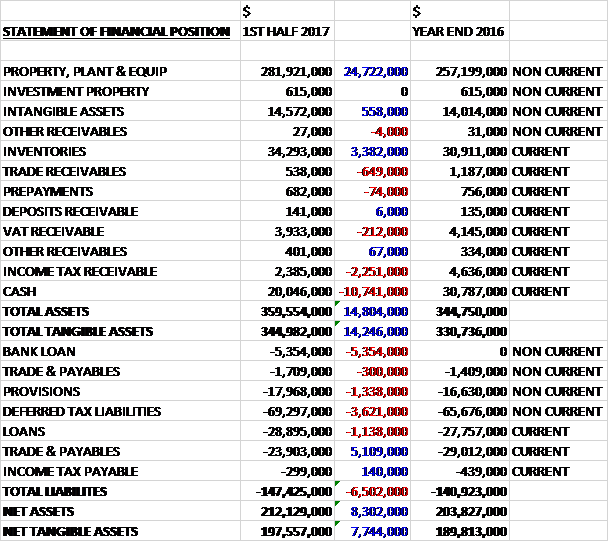

When compared to the end point of last year, total assets increased by $14.8M driven by a $24.7M increase in property, plant and equipment along with a $3.4M growth in inventories, partially offset by a $10.7M decrease in cash and a $2.3M fall in income tax receivables. Total liabilities also increased during the period as a $5.1M decrease in payables was more than offset by a $6.5M growth in loans, a $3.6M increase in deferred tax liabilities and a $1.3M growth in provisions. The end result was a net tangible asset level of $197.6M, a growth of $7.7M over the past six months.

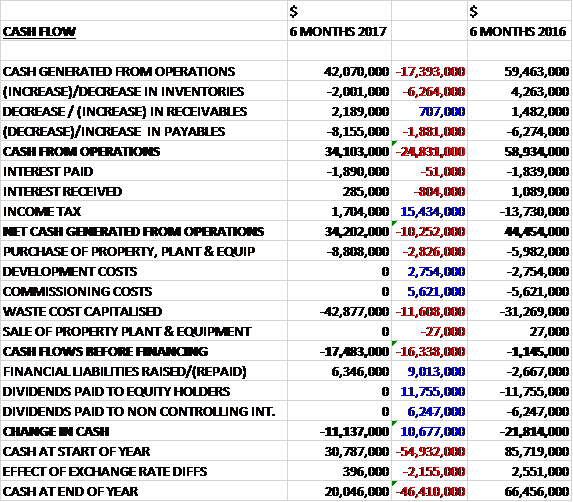

Before movements in working capital, cash profits declined by $17.4M to $42.1M. There was a cash outflow from working capital, mainly due to a decrease in payables, but tax payments reduced by $15.4M to give a net cash from operations of $34.2M, a decline of $10.3M year on year. The group spent $8.8M on property, plant and equipment, mostly relating to the mining support services complex construction, along with $42.9M on waste costs which meant that there was a cash outflow of $17.5M before financing. They raised $6.3M through finance leases to give a cash flow of $11.1M and a cash level of $20M at the period-end.

The global market for diamonds remained cautious. Financing challenges persist and the volatile macro-economic environment continues to create challenges for the middle diamond market.

The operating profit at Letseng was $16.3M, a decline of $30.5M year on year. Overall the group treated 3.2M tonnes of ore at a grade of 1.59cpht compared to 3.3M tonnes at 1.72cpht last time. This meant that the number of carats recovered fell from 57,380 to 50,478. There were lower than planned ore tonnes treated during the period due to reduced plant availability and downtime associated with the installation of the split front ends for plants one and two. The availability issues have largely been addressed now. A significant amount of time and resources were used in addressing these issues and both plants have improved towards the end of the period.

The lower than expected grade was mainly due to the underperformance of the Main pipe contact material and internal changes in the geology of this pipe. The recovery of large diamonds has improved, with four greater than 100 carat diamonds and two D-colour Type IIa diamonds of 98.42 and 80.58 carats being recovered during the period. The average price achieved fell from $1,899 per carat to $1,779 per carat but this has been trending positively having been $1,480 in H2 last year and the latest sale in July achieved $2,385 per carat.

During the period the construction of the relocated mining complex, which is required to make way for the expansion of the open pits, started. Construction progressed well and is expected to be completed in early 2018, on time and budget. Following the disbandment of the Letotho parliament in early 2017, peaceful electrons took place in June and a new government has been elected. Initial engagement with the new government has started positively.

Costs increased during the period due to strengthening of the local currencies against the US dollar, local country inflation and longer hauling distances as a result of mining in deeper sections of both pits.

Going forward the focus will be on building relationships with the new government in Lesotho, continuing to pursue efficiency and cost reduction initiatives, continuing to reduce diamond damage and delivering the mining complex on time and on budget.

The operating loss at Ghaghoo was $5.8M, an improvement of $33.2M when compared to the first half of last year due to the $40M impairment that occurred last time. During the period an earthquake occurred with an epicentre 25km from the mine. There was superficial damage to the surface infrastructure but the earthquake also damaged the seal of the underground water fissure, leading to a large influx of water into the underground workings of the mine. This water was being pumped out of the mine and rehabilitation of the seal will be completed in Q3. Once the water fissure has been sealed, the operation’s annual care and maintenance costs will return to the expected costs of $3M per annum.

The costs incurred in the period included development costs, retrenching costs, one-off costs to renegotiate contracts and one-off costs associated with the additional water pumping and sealing of the fissure as a result of the earthquake.

In February the board decided to place the mine on care and maintenance based on the decrease in the prices achieved for its diamonds. This was achieved in the period and the planned annual care and maintenance cost of $3M is expected to be achieved in the second half of the year.

Apparently the group have received an offer to buy Ghaghoo which the board are considering, but they don’t give any further details. The operating profit in Belgium was $109K, an improvement of $1M when compared to the first half of 2016. The board has approved capital projects of $16M, mainly relating to the Letseng mining support services complex, of which $14.9M have been contracted as of the period-end.

During the period, Roger Davis stepped down as chairman and was replaced by Harry Henyon-Slaney. Also, the Letseng CEO, Mazvi Maharasoa, retired after ten years of service and a new COO, Jeremy Taylor, has been appointed.

No dividends were paid in the period and none are proposed. The group ended the period with a net debt position of $14.2M, cash on hand of $20M and unused debt facilities of $36.2M.

Overall then this has been a rather disappointing period for the group. They have swung to a loss and although net assets were up, the operating cash flow declined and there was a cash outflow before financing. The diamond market remains cautious and the average selling price was lower than last time. The group might have turned a corner here, however, as the more recent sales have been at higher prices due to more large stones being recovered. Both the grade and the tonnes of ore being processed has fallen due to the underperformance of the main pipe material and stoppages at the plant related to the upgrade.

Ghagoo is experiencing further problems following the earthquake but the offer of a sale of the asset is interesting. I would imagine that overall they are not going to get much, however, and this project has been a big waste of money. Whilst the pick-up in the number of large gems is encouraging, there is not much else to get excited about here and I remain on the side lines.

On the 19th September the group announced the recovery of a high quality 115 carat D colour Type IIa diamond from the Letseng mine.

On the 31st October the group released an update covering trading in Q3. At Letseng they recovered 30,774 carats, up 23% compared to Q2. They achieved an average price of $2,397 per carat in July, making it the highest average since September 2015 but the average price in the quarter was $1,858, up 4% over H1. At the period-end they had a net debt position of $11.8M compared to $14.2M at the start of the quarter.

The mine treated a total of 1.3M tonnes, 61% from the main pipe and 39% from the satellite pipe with the higher tonnes treated due to higher plant availability. Despite the improved availability, a crack was identified in the scrubber shell in Plant 2, which is being closely monitored. A decision has been made to reduce the amount of material being fed into this plant to reduce the stress on the scrubber. This reduced feed rate will be maintained until a new scrubber shell is installed, which is planned for February 2018. As a consequence, guidance for tonnes treated for this year has been reduced marginally to between 6.5 and 6.5M tonnes.

Management has implemented various initiatives at Letseng to ensure carats recovered and sold remain within original guidance, and they have increased the contribution from the higher grade satellite pipe material. As a consequence, unit cost guidance is expected to increase due to the higher amortisation charge associated with using the satellite pipe material and the reduced tonnages.

On the 2nd December the group announced that it had not been able to come to an agreement on the sale of Ghaghoo. They are still in discussions with other parties, however.

On the 15th January the group announced the recovery of an exceptional quality 910 carat D colour Type IIa diamond. This is huge, the largest recovered from Letseng and believed to be the fifth largest gem quality diamond ever recovered.

On the 22nd January the group announced the recovery of an exceptional quality 149 carat D colour Type IIa diamond. This is the fourth high quality diamond of over 100 carats recovered so far this year and these shares are looking a bit interesting.

On the 2nd February the group released a trading update covering Q4. The group achieved an average price of $2,217 per carat, up 19% from the amount achieved in Q3 and meant that the average for the year was $1,930. They sold 31,476 carats, up 21% on Q3. At the end of the period the group had a net cash position of $1.4M, a $13.2M improvement on the end of Q3.

The improvement in the recovery of 100 carat gems in continuing into 2018 with five recovered in January alone. This is largely attributable to the ongoing technical improvements made at the Letseng mine.

The reduced feed rate into plant 2 due to the crack in the scrubber shell continues. The installation of a new scrubber shell is planned for April 2018 where the feed rate will revert to normal levels. Full year tonnes treated was 6.4MT, below the 6.5M guidance due to the reduced feed rate. Although waste mining was down quarter on quarter, this was a conscious decision to reduce mining rates to ensure the amount of waste mined was aligned to the amount of ore treated for the year.

During the period 30,560 carats were recovered at a grade of 1.88cpht against an expected reserve grade of 1.75cpht. In the second half of the year a Tomra XRT machine was installed at the mine to re-treat recovery tailings material, recovering 3,298 carats from 25,404 tonnes treated. The recovery of large diamonds has improved markedly over the past four months with 214 larger than 20 carat diamonds recovered in 2017.

Two tenders were held in the period with a total of 31,476 carats sold for $69.8M. A 58.38 carat white diamond achieved $61,905 per carat, making it the highest for rough white diamonds for the year and further contributing to the average increase, a 7.87 carat pink diamond achieved $202,222 per carat, the second highest price per carat ever achieved at the mine.