TT Electronics has now released their interim results for the year ending 2017.

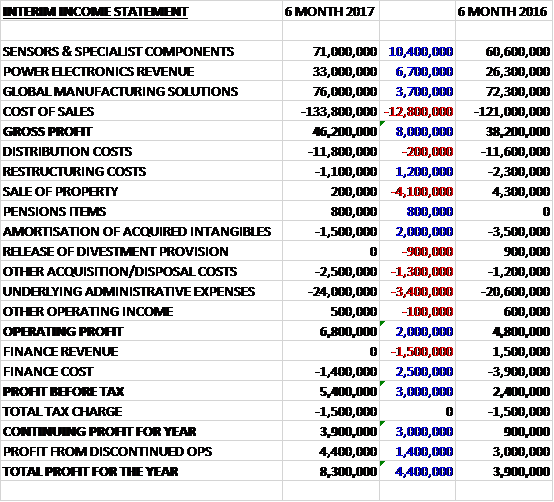

Revenues increased during the period with a £10.4M growth in sensors and specialist components, a £6.7M increase in power electronics revenue and a £3.7M growth in global manufacturing solutions revenue. Cost of sales increased by £12.8M to give a gross profit £8M higher. Restructuring costs fell by £1.2M but there was a £4.1M reduction in the profit from asset sales following last year’s property disposal. There was an £800K income from pension items, representing a past service adjustment under which members agreed to exchange future pension increases for an additional amount of initial pension, and a £2M reduction in the amortisation of acquired intangibles. Offsetting this, there was no release of provisions, which represented an income of £900K last time, other acquisition and disposal costs increased by £1.3M, related to the proposed disposal of the Transportation Sensing and Control division, and underlying admin expenses grew by £3.4M to give an operating profit £2M higher than last time. Finance revenue fell by £1.5M but finance costs declined by £2.5M and tax charges remained flat to give a continuing profit of £3.9M, a growth of £3M year on year.

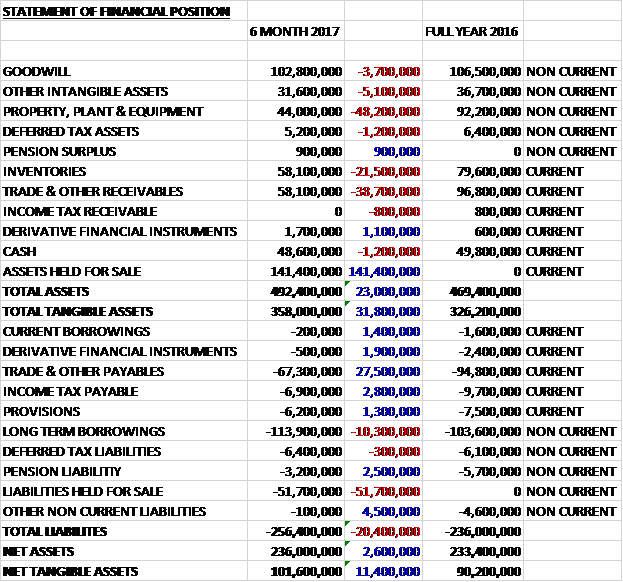

When compared to the end point of last year, total assets increased by £23M driven by a £141.4M asset held for sale, partially offset by a £48.2M fall in property, plant and equipment, a £38.7M decline in receivables and a £21.5M decrease in inventories – this doesn’t tell us much really. Total liabilities also grew during the period as a £27.5M reduction in payables was more than offset by a £51.7M liability held for sale and a £10.3M growth in long-term borrowings. The end result was a net tangible asset level of £101.6M, a growth of £11.4M over the past six months.

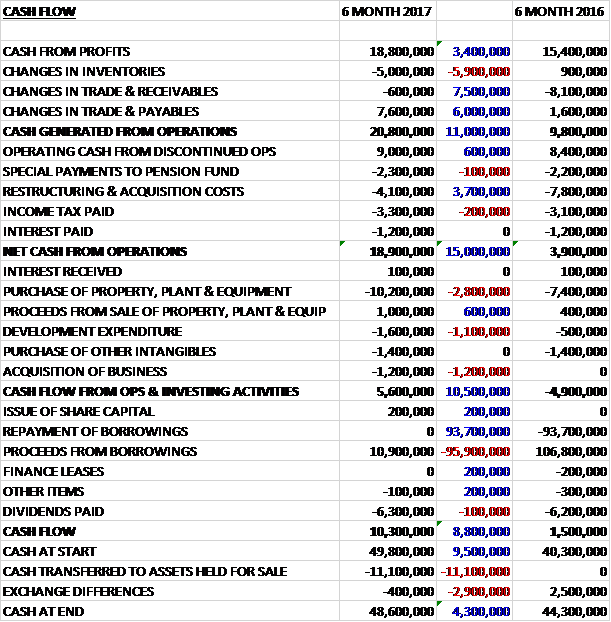

Before movements in working capital, cash profits increased by £3.4M to £18.8M. There was a cash inflow from working capital due to a reduction in payables and after a £3.7M reduction in restructuring costs and an increase of £600K in discontinued operation cash, the net cash from operations came in at £18.9M, a growth of £15M year on year. Although if we remove the cash from the discontinued operations, this is reduced to £9.9M. The group spent £10.2M in property, plant and equipment, £1.6M on development expenditure, £1.4M on other intangibles and £1.2M on acquisitions which left a free cash flow of £5.6M. This did not cover the £6.3M paid out in dividends and the group took out a further £10.9M of loans to give a cash flow of £10.3M and a cash level of £48.6M at the period-end.

The group have reorganised their continuing operations to move their circuit protection, current sensing and signal conditioning capabilities from the Advanced Components division into the Industrial Sensing and Control division, with it being renamed Sensors and Specialist Components. The remainder of the Advanced Components division has been renamed Power Electronics to reflect the change in business mix following the integration of Aero Stanrew into the group. No change has been made to the Integrated Manufacturing Services division apart from it being renamed Global Manufacturing Solutions.

The underlying operating profit of the Sensors and Specialist Components business was £8.6M, a growth of £1.5M year on year. Of this increase, £1.1M was due to a positive forex effect with £400K being the increase at constant currency. This was driven by a 6% revenue increase due to an improving underlying market demand and what the board believe to be a short term increase in OEM distributor demand for their advanced circuit protection, current sensing and signal conditioning components due to extending industry lead times. They have captured market share as a result of reduced lead times and improved capacity.

The benefit of volume increases was partially offset by adverse mix as a result of lower sales of high-margin aftermarket electronic power steering sensors. This impact is expected to normalise in the second half. During the period they saw growth in their optoelectronic assemblies which detect light in a number of applications such as cash machines, medical devices and industrial automation.

The improved market demand for their advanced circuit protection, current sensing and signal conditioning components has been driven by applications requiring reduced size and weight and increased packaging density and power efficiency. Market demand has been strong for these applications in product areas such as white goods and consumer electrical equipment.

New product innovation continues to increase with more new products launched than in the same period of last year. This includes a number of new components with battery monitoring applications with enhanced capabilities including higher rated power and lower temperature sensitivity.

The underlying operating profit of the Power Electronics business was £3.4M, an increase of £1.5M when compared to the first half of last year, all of which was due to favourable forex movements with a further £100K being as a result of the Cletronics acquisition. There was revenue growth of 25% as a result of continued penetration in the aerospace and defence market, together with one off last time buy activities as the group move production from the US to the UK.

Following the new contract won last year with a global engine manufacturer to outsource their product lines for ASIC solutions to the group, they have launched a range of new devices which are used in flight critical aerospace applications. They have now moved production for four customers into the clean room facility in Bedlington, the investment for which was completed last year. The contracts won with these customers will last up to five years.

They have seen increased demand for their connectors being used in rail applications in a significant UK transport infrastructure project. They have also seen good demand from some commercial aerospace engine programmes which have been in ramp up.

During the period they acquired Cletronic, a small US-based manufacturer of electromagnetic components for the aerospace industry, for £1.2M. The acquisition will help to accelerate the strategy for their power electronics capabilities in North America and adds product and technical breadth to the capabilities acquired with Aero Stanrew.

The underlying operating profit of the Global Manufacturing Solutions business was £2.5M, a growth of £100K when compared to the first half of 2016 but all of this, again, was due to favourable forex movements with the constant currency operating profit down 11%. Revenue was down 2% at constant currency. Revenue growth in Asia was strong and the North American industrial market weakness has subsided and the group has won contracts that were previously deferred but this has been offset by weaker European customer demand which has prompted management to make headcount reductions which is expected to yield benefits in H2.

After experiencing challenging North American industrial markets during 2016, they have started to see the market strengthen, winning key multi-year awards in aerospace and defence. In Asia they have continued to see strong growth, particularly in medical markets across a number of customers in life sciences and lab instrumentation. For one customer where they supply printed circuit board assembly integration box builds and cable assemblies, they have seen increased demand as a result of the fast growing Asian medical market as well as ramping up new contracts won with this customer.

In July, after the period-end, the group announced the proposed disposal of the Transportation Sensing and Control division to AVX Corp for £118.8M in cash. The business made an underlying operating profit of £6.5M in the period, an increase of £1.1M year on year with £600K of that as a result of favourable forex movements making this the best performing sector. Completion is expected in Q4.

Going forward, the first half performance and order momentum reinforce the board’s confidence of making further progress in the rest of the year. At the current exchange rate, the group are not expecting to see any further benefit in the second half.

At the current share price the shares are trading on a PE ratio of 21.3 which falls to 16.3 on the full year consensus forecast. After an increase in the interim dividend, the shares are yielding 2.6% which remains the same on the full year forecast. At the period-end, the group had a net debt position of £56M compared to £65.5M at the end of the prior year but it should be noted that this will be wiped out by the £118.8M cash consideration of the disposal.

Overall then, on the surface this has been a strong performance with an increase in profit, a growth of net assets and an increase in the operating cash flow. Some free cash was generated but not enough to cover the dividends. This good performance has been almost entirely due to favourable forex movements, however. Looking at constant currency operating profits, Sensors & Specialist Components saw a decent performance but how much of this was due to a one-off increase in OEM distributor demand is hard to tell.

Power Electronics saw a flat performance and Global Manufacturing saw a declining profit due to a reduction in European demand. Clearly the big event is the disposal of the most profitable part of the group which will eliminate the debt and give the group a decent amount of cash to invest in the business. The current performance doesn’t really warrant the forward PE of 16.3 and yield of 2.6% but I believe that is taking into account the cash that is coming this way. I have decided to take a position here but am a little unsure if that is the right thing to do!

On the 20th November the group released a trading update covering the first four months of H2. Trading overall has been positive with the growth trends experienced in the first half in Sensors and Specialist Components and Power Electronics continuing, and with Global Manufacturing Solutions returning to growth in the period as expected. Group revenue is up 6% on an organic basis compared to the prior year. The order book across all divisions continues to be strongly ahead of the prior year.

The group completed the sale of the Transportation Sensing and Control division. As part of the separation they have announced the closure of their Global Manufacturing Solutions site in Romania which was shares with the TS & C division. They will move their lines to Wales and China rather than incur the cost of establishing a new facility with the site closure expected in H1 2018. Overall this is decent enough, I remain a holder.

On the 15th February it was announced that the group had made a cash offer for Stadium Group whereby Stadium shareholders would be entitled to receive £1.20 for each share, valuing the group at around £45.8M.

Stadium is a supplier of wireless connectivity solutions, power products, human machine interface solutions and electronics assemblies with design, manufacturing and fulfilment operations in the UK, Sweden, the US and Asia. In 2016 the business generated revenues of £53.1M and pre-tax profit of £2.2M.

The benefits are being cited as a greater presence in attractive segments of the industrial, medical, aerospace and defence and transportation sectors; enhanced product capabilities in power electronics and connectivity; and extended R&D facilities. The transaction is being funded by existing cash resources and debt and the group expects it to be immediately earnings enhancing.

The two groups have a complementary customer base, providing opportunities for both businesses to cross-sell their product portfolios. The board believes that their scale and well established routes to market will be beneficial to extending Stadium’s product presence. In particular the development of Stadium’s North American business is expected to be accelerated through TT’s established network in the region.