GlaxoSmithKline has now released its final results for the year ending 2014.

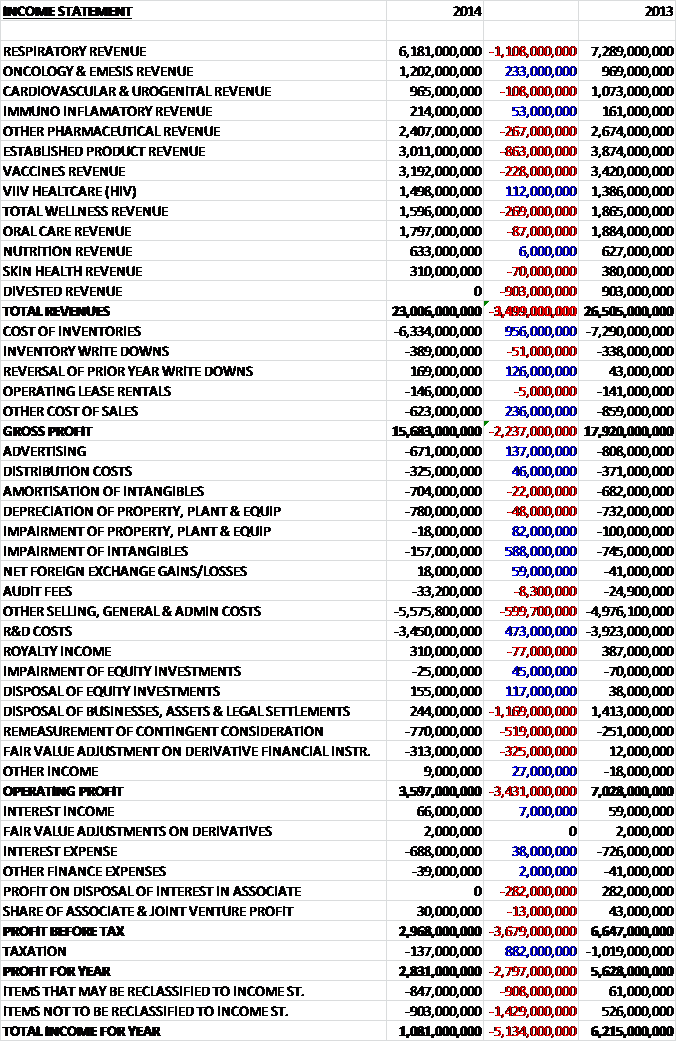

When compared to last year revenues in general fell, driven by a £1.1BN decline in respiratory sales, an £863M fall in established product sales, a £267M decline in other pharmaceuticals and a £269M fall in total wellness products. Not all divisions fell, however, with the best performing being Oncology, up £233M and ViiV Healthcare, up £112M. Cost of inventories and other cost of sales both fell and the gross profit was some £2.237BN lower at £15.7BN. A £137M fall in advertising costs and a £588M decline in intangible impairments were offset by a £600M increase in other sales and admin prices which included a £114Mm charge for an additional catch up year of the US Branded Prescription Drug Fee in accordance with the final regulations issued by the IRS.

We also saw a £473M decline in R&D costs but there were several one-off costs that increased such as the re-measurement of contingent consideration due to the higher potential sales of ViiV healthcare products and a £313M charge relating to a change in value of financial instruments due to the currency hedge taken out to protect the Novartis deal, so this should be counteracted by the higher receipts from Novartis due to currency movements. Compared to last year there was also a £1.169M fall in profits from disposals so that operating profit was nearly half that of last year at £3.597BN. There were some improvements to finance cost but there was no profit on the disposal of an associate which equated to £282M last year. There was very minimal tax to pay, however, as the charge fell by £882M to give a profit for the year £2.797BN lower than in 2013 at £2.831BN.

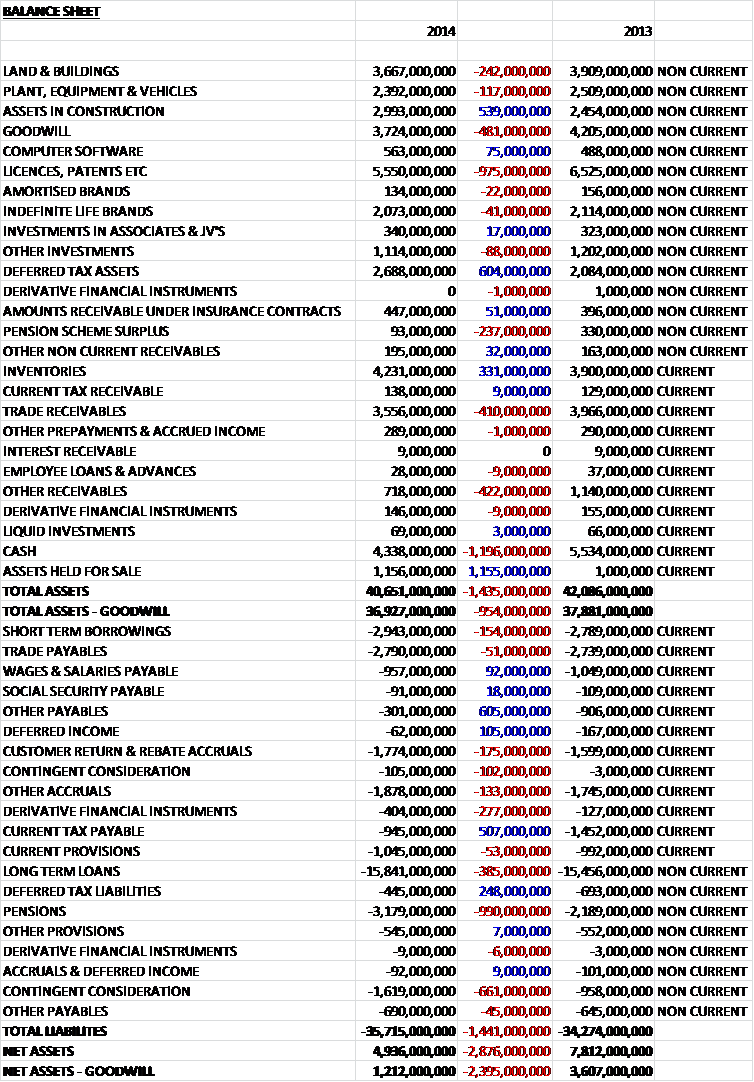

When compared to last year, total assets fell by £1.435BN, driven by a £1.196BN decline in cash levels, a £975M fall in the value of patents, partly due to the transfer to assets held for sale, and partly due to amortisation with a small impairment of Lovaza; a £481M decline in goodwill which was moved to assets held for sale, a £410M fall in trade receivables and a £422M decline in other receivables reflecting the receipt of deferred receivables from Aspen in respect of the inventory and a manufacturing site which formed part of the disposal of the anti-coagulant business. These declines were partially offset by a £1.155BN increase in assets held for sale, a £604M growth in deferred tax assets, a £539M increase in assets under construction and a £331M increase in inventories.

Conversely liabilities increased during the year driven by £990M increase in pension liabilities, a £661M increase in contingent consideration, a £385M increase in loans and a £277M growth in derivative financial instrument liabilities, partially offset by a £605M decline in other payables due to the lack of the £620M payable to non-controlling interests in the Indian subsidiary that was settled during this year, and a £755M decline in tax liabilities. The end result is a net asset (excluding goodwill) level of £1.212BN, a £2.395M collapse when compared to 2013. The group also has £701M of operating lease commitments, £310M of which are on the balance sheet.

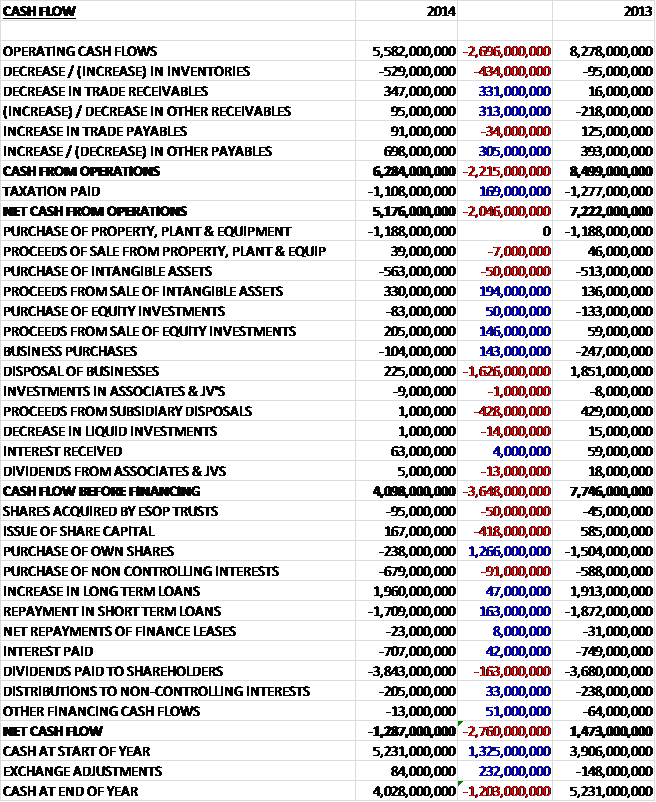

Before movements in working capital, cash profits were £2.696BN lower at £5.582BN. A decrease in receivables and an increase in payables, however, improved this to £6.284BN, a £2.215BN decline from last year and after tax the net cash flow from operations was £5.176BN. In a quirk of fate, the group spent the same amount as last year, £1.188BN, on property, plant and equipment. The group then spent £563M on intangible assets and gained a net cash inflow from the purchase and disposal of businesses so that before financing there was still a fairly healthy cash inflow of £4.098BN. This cash flow just about covered the £3.843BN spent on dividends but could not cover the £707M interest costs and the £679M purchase of non-controlling interests relating to the investment in the Indian subsidiary which meant there was a net cash outflow of £1.287BN. The group still ended the year with £4.028BN of cash, though, so despite losing more than a billion pounds in cash, this was not a total disaster.

Trading conditions during the year have continued to be difficult, especially in the US but the group have apparently worked hard to improve their formulary positioning and coverage in the country and as they move into 2015 there are some encouraging signs of how this might help them regain market share and deliver an improved performance in the respiratory sector where Incruse Ellipta has been launced for COPD and Arnuity Ellipta was launched for asthma with a regulatory decision for the potentially important Mepolizumab pending. Performance in Consumer Healthcare was impacted by some supply issues which seem to have been remedied, indicating a potentially improved performance in 2015 in the sector. New products launched in the last five years contributed sales of £1.5BN, an increase from £1.4BN last year on a rolling basis with Arzerra, Lamictal XR, Potiga, Prolia and Votrient no longer being included in the calculation. New respiratory drugs Breo Ellipta and Anoro Ellipta gained Medicare Part D coverage of 74% and 65% respectively which gives some early indication of how the new portfolio will help the group regain market share and deliver improved performance in respiratory.

In Europe rising public debt and government austerity programmes continue to create pressure on healthcare spending. Spending on hospital medicines increased which was mostly driven by increased use of oncology and biological products but decreased in primary care. In the US the focus on cost and value is leading payers to reduce price, restrict access and demand more differentiated products both within the private marketplace as well as for public programmes. In Japan the Ministry of Health conducted a bi-annual review of medicine pricing resulting in a 2.7% reduction under the National Health Insurance pricing scheme with the premium for new drug development remaining in place. In emerging markets countries such as Indonesia, China and India are looking to expand the population covered by government funded health schemes which suggests opportunities for high volume tenders but impacts pricing. In some markets patents and data collection are less enforceable. For example in India, Brazil and Argentina governments are considering practices that restrict the availability of patents. In addition some countries are considering more widespread use of compulsory licensing where an individual or company can use another’s patent without their consent and pays the patent owner a set fee for the license.

Profits of US pharmaceuticals fell by £782M to £3.173BN; European pharmaceutical profits fell by just £72M to £2.205BN, Japan pharmaceutical profits fell by £102M to £466M and emerging market pharmaceutical profits increased by £7M to £993M. In Respiratory the group expect to see a return to growth in sales in 2016. Seretide/Advair sales were down 15% to £4.2BN, Flixotide/Flovent sales fell by 6% to £665M and Xyzal sales, almost exclusively made in Japan, were up 7% to £130M. In the US respiratory sales fell by 18% due to continued pricing and contracting pressures in the market. Sales of Advair were down 25% to £1.972BN with a 14% fall in volume and an 11% decline in price. Flovent sales were down 6% while Ventolin sales increased by 18%. The newly launched products, Breo Ellipta and Anoro Ellipa recorded sales of £29M and £14M respectively.

European respiratory sales fell by 3% largely due to increased competition. Seretide sales fell by 5%, primarily due to falling prices as a result of competitive pressures and the transition to newer products in the portfolio during the latter half of the year. Relvar Ellopta sales were £18M during the year. In Emerging markets respiratory sales grew by 3% with Seretide sales increasing by 3% to £400M, helped by an improved performance in China. Sales growth for Ventolin and Veramyst was offset by declines in Flixonase due to falls in Chinese revenues. In Japan respiratory sales fell by 2% to £475M. Sales of Relvar Ellipta offset the impact of increasing competition on Adoair, which fell 6% to £228M. The growth in Xyzal, up 8%, was more than offset by lower sales elsewhere in the portfolio but new prescription share has increased to more than 56% following substantial increases in new prescriptions for Relvar after lifting of the “Ryotan” prescribing restrictions.

Oncology sales grew by 33% to £1.202BN with contributions from Votrient, up 33% to £410M and Promacta, up 34% to £231M. Conversely sales of Arzerra fell by 24% while Tykerb declined by 11% to £171M. New launches compensated for generic competition to both Hycamtin and Argatroban with Tafinlar and Mekinist recording sales of £135M and £68M respectively. In the US, Oncology grew by 41% to £509M with contributions from Votrient, Promacta, Tafinlar and Mekinist. In Europe sales grew by 29% to £417M led by Votrient while in Emerging Markets, sales were up 30% to £169M and in Japan sales grew 17% to £65M.

Sales in the Cardiovascular, metabolic and urology category were down 3% to £965M. The Avodart franchise grew by 1% to £805M with a 17% growth in Duodart. Sales of Levitra fell by 28% while sales of Prolia were down 10% to £41M following an agreement with Amgen to terminate joint commercialisation in selected markets. Sales in the US were down 16% to £364M although emerging markets grew by 20% to £145M while Japan also grew with sales up 14% and European sales remained flat during the year. Sales of immune-inflammation products increased by 40% to £214M, helped by a 25% sales increase for Benlysta, growing to £173M. The other therapy areas saw sales fall by 2% largely reflecting generic competition to dermatology products.

Profits in the established products portfolio declined by £559M to £1.793BN and sales of the established products portfolio fell by 16% to £3.011BN. Generic competition to Lovaza, whose sales more than halved to £240M, Seroxat and Valtrex all contributed to the decline. Sales in the US fell by 31% to £854M while sales in Japan and Europe fell by 15% and 13% respectively. Emerging markets fared slightly better, falling by just 1%.

Vaccine sales were down just 1% to £3.192BN although declines in Europe and Japan were partially offset by a small growth in emerging markets while US revenues were flat. Infanrix grew by 2% to £828M with growth in the US being partially offset by declines in Europe and emerging markets. Boostrix sales increased by 16% to £317M with growth in all regions except the US where sales fell by 7% due to the return of a competitor product. Rotarix sales grew 7% to £376M driven by tender shipments in Europe and emerging markets, although there was a decrease in the US which was impacted by a CDC stockpile withdrawal in Q4. Synflorix sales were also up, increasing by 4% to £398M mainly due to a strong tender performance in emerging markets. Sales of the hepatitis vaccines fell by 6% to £558M, partly due to supply constraints affecting the US and emerging markets. Fluarix and FluLaval sales fell by 9% to £215M due to lower production levels for the year and increased competition. Cervarix sales declined 26% due to a fall in sales in emerging markets and Japan along with increased competitive pressures.

Profits at ViiV Healthcare grew by £92M to £977M. Tivicay recorded sales of £282M and uptake has led the industry in the US, Germany and Japan compared to recent HIV medicine launches. Sales of Triumeq, the new single pill treatment that was launched in the USA in August and in some European countries in September were £57M during the year. Epzicom sales grew by 8% to £768M and Celsentri/Selzentry was flat at £136M. Sales in North America grew by 28% driven by strong performances of Tivicay and Triumeq as well as continued growth from Epzicom with the former two performing strongly with patients switching therapies. In Europe sales grew faster than the market as a result of an excellent performance from Tivicay, approved in January 2014, and successful initial uptake of Triumeq in countries where it has been launched. Sales also grew in the International region owing to the growth of Celsentri, Kivexa and Tivicay which now contribute to over two thirds of the region’s revenue. Japan and Australia, which launched Tivicay in the second half of the year have seen particularly impressive sales performance.

Consumer Healthcare profits fell by £172M to £657M but an improved performance was seen in Q4. Oral Health sales grew by 4% to £1.797BN driven by strong growth of Sensodyne in Sensitivity and acid erosion which was up 11%, and gum health, also up 11%. The brand maintained its leading position in the sensitive teeth category and consumption grew ahead of the market in all regions with the most notable successes seen in China and North America where Sensodyne Repair & Protect and Sensodyne Complete were key drivers. The Nutrition category grew 10% to £633M led by Horlicks and Boost, which grew 11% and 9% respectively.

The leading UK protein brand, MaxiNutrition, was up 10% driven by strong innovation and increased distribution. In Wellness, sales fell by 7% to £1.596BN, impacted significantly by supply, particularly in Smokers Health. The gastro-intestinal products grew by 4% and despite the impact from supply constraints, ENO saw very strong growth in emerging markets, in India and Brazil particularly. Pain management grew by 2% driven by double digit growth of Fenbid in China but offset by some supply interruption to Bactroban in the country. Skin health sales were down 11% to £310M driven by Bactroban supply interruptions in China, partially offset by increased Physiogel sales. It is expected that Flonase Allergy relief will be a growth driver for the division in 2015 and to provide a well-established allergy treatment to consumers as the group continues to lunch the brand as an over the counter product in various markets.

At a regional level, the US business declined 8% to £836M, impacted by supply issues, primarily in Wellness. Oral health grew by 4%, led by very strong sales from Sensodyne. In Europe, sales fell by 5% to £1.242BN due a combination of factors such as supply, competitive pressures, particularly in oral health, and political disruption in Eastern Europe. ROW markets were up 4% to £2.258M despite an overall slowdown in emerging markets. Of particular note was the India business which grew 12% during the year with a successful re-stage of Horlicks, focusing on its increased nutritional benefit and an improved formula that dissolves more easily in both hot and cold milk. The group also launched a new variant, Horlicks Saffron and Almond, in India specifically designed to meet the unique tastes of Indian consumers. There was a continued focus on new routes to market, expanding the distribution model to better reach rural consumers. In Latin America, sales were up 4% with strong performances in Oral Health and Wellness.

Once again there were a lot of restructuring costs, totalling £750M this year which included £101M under the Operational Excellence Programme, £334M under the Major Change Programme, £243M under the Pharmaceuticals Restructuring Programme and £67M on pre integration planning on the proposed Novartis transaction, and more specifically the restructuring of the pharmaceuticals business in North America, Emerging Markets and Europe leading to staff reductions in sales force and administration; projects to rationalise core business services and to simplify or eliminate processes leading to staff reduction in support functions; transformation of the manufacturing and vaccines businesses to deliver a step change in quality, cost and productivity; and the rationalisation of the consumer healthcare business. The Operational excellence programme has now been completed and has delivered £2.9BN in annual savings for a total cost of £4.7BN. The major change programme is still ongoing and has so far delivered an additional £600M in annual savings for an expected cost of £1.5BN, with a further programme announced this year to refocus the pharmaceutical business expected to contribute a further £1BN of savings by 2017 at a cost of £1.5BN.

The group are working to simplify operations, reducing the number of third party suppliers who manufacture medicines on behalf of the company by a further 8% and they have reduced complexity in their supply base by standardising specifications for goods and materials that are purchased and integrated sourcing processes are being pursued. The complexity of the pharmaceutical product portfolio was also addressed with a 19% reduction since 2012 that equates to more than 4,000 discontinued packs.

Some key challenges for the group this year have included increased pricing pressure in the US from market changes, competitor dynamics and contracting; continued pricing pressure in Europe due to government austerity programmes; unanticipated supply continuity challenges in consumer healthcare; disappointing phase 3 results for MAGE A3 and darapladib programmes and rebuilding in China following the criminal conviction of a China affiliate for violation of Chinese law

As with most UK companies with a pension scheme, it is currently running at a deficit which requires regular payments to reduce. The liabilities on GSK are not as hefty as some other companies with £85M being paid this year with the same amount expected next year, although employer contributions as a whole are expected to be £320M in respect of defined benefit pension schemes and £70M in respect of post-retirement benefits.

This year has been fairly quiet as far as acquisitions and disposals are concerned, probably due to the impending Novartis deal. £225M was received as contingent consideration on the Anti-coagulent business disposed of last year and costs of £141M have so far been incurred from the Novartis deal. One large acquisition of non-controlling interests took place with regards to the Indian subsidiary where the group increased its holding from 51% to 75% for a total of £625M.

As part of the proposed Novartis transaction, a new consumer healthcare business will be created over which GSK will have majority control with a 63.5% interest. In addition GSK will acquire Novartis’ global vaccines business, excluding the flu vaccines for an initial cash consideration of $5.25BN with subsequent potential milestone payments of up to $1.8BN and ongoing royalties. GSK will divest its Oncology portfolio and future products in that category for a cash consideration of $16BN. Under the terms of the transaction, up to $1.5BN could be returned to Novartis if certain conditions relating to the COMBI-d trial are not met. The transaction is expected to be completed in the week commencing 2nd March and it is estimated that the deal will deliver annual cost savings of £400M, the delivery of which will be phased over the next five years.

The group seems to be doing a lot to try and open up further emerging markets. In India they have created a network of over 13,000 rural sub-distributers who are delivering GSK products to village retailers. In addition, local women have been trained in order to set up their own distribution businesses selling directly to households in areas that are not covered by local stores. In Africa the group are investing to increase access to medicines, build capacity and deliver growth. Over the next five years, £130M will be invested in Africa with £25M being spent to create the continent’s first non-communicable diseases open lab where GSK scientist and external researchers will work on understanding disease variations found in African patients in order to develop new medicines to address the specific needs of African patients. Up to £100M is being invested to expand existing facilities in Kenya and Nigeria and to build new factories elsewhere to ensure local production of medicines in Africa required by African people and the facilities will make locally relevant products.

A lot of GSK’s problems are due to their most important drug running into sales problems. Seretide/Advair sales fell by 20% to £4.229BN. There are just no other drugs in the portfolio that come close to the success of this one, which is a big problem when sales are falling 20% a year. Incidentally, the next largest drug, Avodart, saw revenues fall by 6% to £805M although on a constant currency basis, sales were broadly flat suggesting this drug still has some legs. So are there any major drugs that saw sales increase? Well, there are a number of promising candidates in the Oncology portfolio. Votrient sales increased by 24% to £410M, Promacta sales were also up 24% to £231M and the new one, Tafinlar, grew sales from £16M last year to £135M this year. It is unfortunate then that the Oncology portfolio will be lost in the deal with Novartis. The only other big growth drug is Tivicay in the ViiV healthcare portfolio which grew from £19M in 2013 to £282M this year which is an exceptional performance and is now the second most important ViiV drug after Epzicom which saw sales increase 1% to £768M.

The pipeline does seem fairly strong. Following approvals received in 2013 for respiratory products Breo Ellipta and Anoro Ellipta, Tafinlar and Mekinist in oncology and Tivicay in HIV, the group received approvals for Incruse Ellipta and Arnuity Ellipta in respiratory, Triumeq in HIV and Tanzeum for Type 2 diabetes this year. They are waiting for FDA decisions on Breo Ellipta for use in asthma and mepolizumab for severe eosinophilic asthma with up to 25 phase 2 and 3 starts expected. In the advanced pipeline, the board see significant potential from the shingles vaccine, a triple combination therapy for COPD and new long acting HIV treatment Cabotegravir and the potential Ebola vaccine that is now being tested in a phase 3 clinical trial could bring some Kudos to the group if it is successful.

As is normal for GSK and probably other similar companies, there are multiple legal and other disputes ongoing mostly relating to patents; product liability, principally relating to Avandia and Paxil; anti-trust, principally relating to Wellbutrin XL and Lamictal; government investigations, currently relating to the China settlement and SEC/DOJ and SFO related investigations; and contract terminations. During the year a £301M fine was paid to the Chinese government with £248M being paid on the various other disputes, in particular the product liability case regarding Paxil and various other government investigations. In China the group had offered money or property to non-government personnel in order to obtain improper gains and had been found guilty of bribing non-government personnel. The UK and US authorities are also looking into some of the group’s operations. During the year two sites received quality standard warning letters from the US FDA, one in Cork and one in Canada which the group is apparently taking comprehensive actions over.

In order to combat these problems, management has de-linked compensation for sales reps from the number of prescriptions written to remove any conflict of interest. In addition the group has also stopped paying healthcare professionals to talk about their products. Instead Medical Science Liaisons will be delivering talks to physicians about the group’s recently released medicines in the US. One benefit of this is that internal experts may have a more direct knowledge of the clinical trials which led to approval of the medicine and thus far the programmes are attracting a similar number of attendees as the external presentations of the past. In addition, staff are now required to undergo mandatory training on the group’s code of conduct and the group has enhanced its whistleblowing procedures.

Sir Philip Hampton has been selected to succeed Sir Christopher Gent as Chairman of the group at their next AGM in May. Jing Ulrich, non-executive director will stand down at the AGM as does Tom de Swaan after spending nine year at the group.

Going forward, closing the Novartis deal is a key consideration as well as building on the new respiratory products, launching new products and making sure the supply issues in consumer healthcare are properly dealt with. Some of the sales headwinds experienced this year will continue into 2015 with a greater impact in the first half of the year but a stronger performance is expected in the second half. During the year the group will also make a decision on whether to undertake a minority IPO of ViiV Healthcare.

At the current share price the shares trade on a pretty expensive looking 26.5 P/E ratio, although clearly this is affected by one-off costs. On next year’s consensus forecasts it reduces to 16.8 which is still not exactly cheap. Conversely the dividend yield is currently at 5.2% which is an excellent return which is expected to stay the same next year, although this payout is not covered by earnings but is just about by free cash flow. The group currently has net debt of £14.377BN, a big increase from the £12.645BN at the end of last year with a US Medium term note of £641M and a European medium term note of £1.239BN becoming payable this year.

Overall then there is no denying this was a difficult year for GSK. Profits were down and net assets collapsed during the year with a near £1BN increase in pension liabilities not helping. The cash flow was actually a little better than I was expecting as despite the large cash outflow, free cash flow nearly covers dividends and interest payments. The real issue is the decline in prices and volumes of the main blockbuster respiratory drug in the US which is likely to continue into next year, although the supply problems of consumer healthcare products seems to have been sorted out. The Novartis deal is clearly the main thing to happen during the year but it is a shame to see the successful Oncology portfolio leaving. The other good performer was ViiV Healthcare, with some successful new launches during the year but a quick glance at the pipeline suggest there are not many new HIV drugs in development which is perhaps why the group are looking to offload the division.

Some of the new respiratory drugs that gained approval this year could have a good potential which could be a driver for growth in the future, though, so I will keep an eye on this. I think that next year will probably be quite difficult for GSK too but that 5.2% dividend yield is enough to keep me holding here.

The GSK chart actually looks quite promising. After a decline through much of 2014, the shares have been recovering so far this year with both the share price and the 50 day EMA above the 200 day moving average.

On the 2nd March the group announced that it had completed the three-part transaction with Novartis. As a reminder, they have acquired Novartis’ global vaccines business excluding the flu vaccines for an initial cash consideration of $5.25BN; completed the formulation of a consumer healthcare joint venture where the group has a 63.5% interest and divested the Oncology business for a cash consideration of $16BN. The net after tax proceeds received today were $7.8BN and $1.5BN could potentially be returned if certain conditions relating to the COMBI-d trial are not met. GSK plans to use the proceeds to fund a $4BN capital return to shareholders which is expected to be implemented through a B share scheme.

On the 13th March it was announced that GSK had sold 28.2M of its shares in Aspen for approximately £574M. This sale represents half of the group’s holdings in Aspen and they have undertaken not to sell any more for the next 180 days. Going forward, it is expected that the group will no longer account for Aspen as an associate.

On the 19th March it was announced that the Pulmonary Allergy Drugs Advisory Committee and Drug Safety and Risk Management Advisory Committee of the US FDA had advised that Breo Ellipta should be approved for adults with Asthma but not for children with the full decision to be made at the end of April.

On the 28th April the group presented data from a phase 3 study of its vaccine candidate for Shingles. The two dose schedule reduced the risk of the virus by 97.2% in adults aged 50 and over with no serious side effects. Additional trials are to evaluate the vaccine in people over 70 and those with compromised immune systems.

On the 30th April, the group announced that the US FDA approved Breo Ellipta for the once-daily treatment of patients aged 18 and over. The data submitted did not show adequate risk-benefit to support the approval in patients aged between 12 and 17, however. This follows the approval already granted for use of the drug with patients with COPD.