Swallowfield have now released their interim results for the year ending 2015.

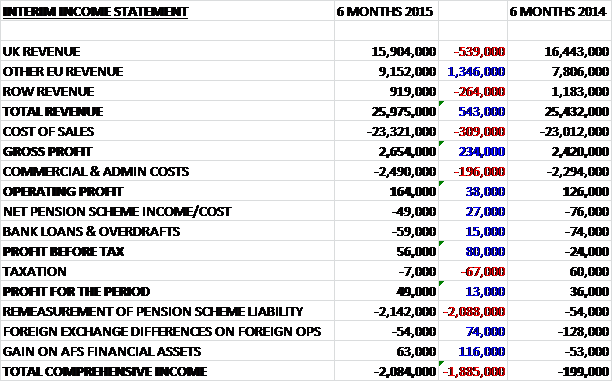

Revenues were up £543K when compared to the first half of last year despite the weak Euro reducing sales revenue by £600K, with good growth in EU sales being partially offset by declines in UK and ROW sales. Cost of sales increased slightly to give a gross profit some £234K higher. Commercial and admin costs increased by £196K but both pension costs and interest costs reduced so that profit before tax was £80K higher, before the lack of the tax rebate achieved last time meant that profit for the period grew by just £13K to £49K.

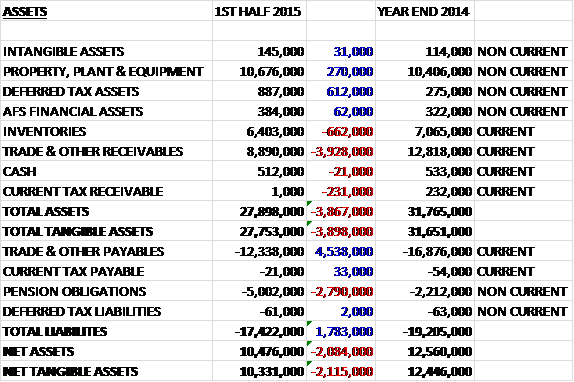

When compared to the end point of last year, total assets fell by £3.9M due to a £3.9M decline in receivables and a £662K fall in inventories, partially offset by £381K increase in tax assets, a £270K growth in the value of property, plant and equipment and a £62K increase in the value of the financial asset, relating to the re-measurement of the shareholding in Shanghai Colour Cosmetics. Total liabilities also fell during the period as a £4.5M decline in payables was only partially offset by a £2.8M increase in pension liabilities. The end result is a £2.1M fall in net tangible assets to £10.3M. A little disappointing but this is still fairly strong for a company of this size.

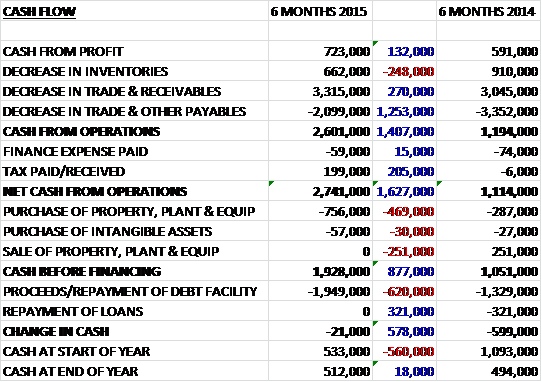

Compared to the first half of 2014, cash profits increased by £132K and with good control of working capital, particularly with a large decrease in receivables, the cash from operations increased by £1.4M to £2.6M. A lower finance expense and a decent tax rebate meant that net cash from operations was some £1.6M higher at £2.7M. Of this cash, £756K was spent on tangible assets and £57K on intangibles so that free cash flow was an impressive £1.9M. This was used to repay the debt facility to give a small cash outflow of £21K, a £578K improvement on the first half of last year.

In collaboration with one of the group’s large customers, they have developed and produced an aerosolised post foaming shower gel in a plastic can which is apparently soft and warm to the touch and weighs about 18% less than the previous metal format. Production started in December and it is now appearing in stores across the UK. The group have also received some initial orders for their own brand product, the ‘Tru Shave’ brand, which will appear in value retail channels shortly and have begun discussions with a department store regarding the distribution of their new premium beauty brand, Bagsy, which will begin production in March but due to retailer decision making taking longer than expected, the sales and margin delivery may take longer than anticipated, pushing some of the benefits into next year. It seems that the group are also considering some potential acquisitions should the right targets emerge.

The group are looking to develop a new high growth, high margin category by 2016. In the first half of the year they ran production trials on aerosolised food and beverage products and expect to run production trials for another new product in the second half of the year, which sounds like an interesting development. The consolidation of the Bedford facility into two buildings from three has now been completed with some production lines being relocated to the Czech site. This should deliver full year savings of about £230K going forward.

During the period the group had one customer that accounted for 13.5% of revenues and one that represented 10.8% of sales which means they are still quite reliant on a few large customers but this was better than during the same period of last year when one accounted for 15.8%, another 11.4% and a third for 10.3% of sales.

It can be seen that the group suffered a relatively large increase in pension liabilities. This was because that corporate bond yields, that are usually used as a proxy to determine the discount rate, were significantly lower than six months ago which has translated into higher liabilities. The pension scheme is currently undergoing its latest triennial valuation, the results of which are expected to be finalised by the end of the year.

Looking ahead, the UK and European markets remain very competitive with pressure on pricing and continuing uncertainty surrounding the Euro. The performance in the second half of the year remains dependent on the exact timing of planned product launches (we have already learned that the premium brand product sales are likely to slip into next year), the impact of wider economic condition and underlying consumer demand. Overall for the current year, the board expects a strong profit before tax growth when compared to last year with a more significant full year benefit expected next year.

Due to the investments being made in the group, an interim dividend has not been declared. Going forward it is intended that a dividend pay-out will be reinstated and be aligned to underlying earnings and the cash flow of the group. At the period end, net debt stood at £3.1M, a £1.5M improvement on the same period of last year and a £1.9M improvement on the end point of last year. It seems as though the board expect this to increase again in the second half of the year though, due to the brand launches and increased investment.

Overall then, this is a solid set of results but perhaps not as much progress has been made as was expected. European sales were good, but revenues fell across other regions and profits were only slightly ahead of the same period last year. Net assets actually fell, mainly due to the increase in pension liabilities but the strong cash generation, partially due to a good control on working capital, meant that the group could pay back some debt. There does not seem to be much information about current trade and projects but some guidance has been given on future products, which sounds interesting. There is just enough here I think to keep me holding in anticipation of a stronger second half to the year.

The reaction to the interim results was not great with the market retracing after a good run but at the chart still looks OK for now.

On the 30th April the group announced that it had acquired the Real Shaving Company brand from Creightons. The Real Shaving Company is a well-established premium brand in the male grooming sector whose products are distributed in the UK through major supermarkets and health & beauty retailers as well as the value retail sector. They also sell their products into Canada and France. The price comprises of an initial cash consideration of £900K with a further £100K contingent on the outcome of certain customer negotiations, plus stock at valuation, which is expected to be £170K to give a total cash consideration of up to £1.17M. Underlying EBITDA of the brand for the year to March 2015 was £300K on sales of £800K and the acquisition is expected to be earnings enhancing in the first full year of ownership.

The acquisition will be financed with a new five year loan of £720K with the balance from existing facilities. It enables the group to leverage already developed technologies such as plastic aerosols and gives them a presence in trade channels that they are trying to access with their other brands such as Bagsy and Tru. It also enables them to leverage their existing capabilities in females shave formulations and gifting, neither of which currently feature in the brand’s product range. This seems like a very good fit for the group at a decent price, whether they can afford even this modest acquisition remains to be seen, however.

On the 24th June the group announced that CEO Chris How’s wife purchased 10,000 shares at a cost of £11.4K. After the purchase he has an interest in 60,000 shares. Although this is quite a modest purchase, I still take it as a good sign, although the CEO still does not really have a very large holding here.

On the 8th July the group released a statement covering trading for the year ending 2015 in which they stated that profitability will be in line with market expectations. Revenues for the full year are expected to increase by 0.8% or 2.7% on a constant currency basis and they have seen a slight softness in revenues versus expectations due to the delayed availability of some materials and the continued effect of the weak euro. The net debt at the year-end stood at £5.4M which included the £1.2M spent on the acquisition compared to £5.1M at the end of last year so progress seems slow in bringing this down.

The recently acquired Real Shaving Company brand has now been integrated into the business ahead of schedule and customer response to the group’s plans for the brand have apparently been positive. The development of the own brands continues to progress well with the first orders of the premium brand “Bagsy” having been shipped in recent weeks and the extension of the distribution of the value brand “Tru”. The premium new male haircare brand has also been positively received by major retailers and will be launched in the autumn.

Going forward, it is expected that the challenging retail market conditions being experienced will continue in the medium term but the new strategy outlined last year will gain momentum and should improve profitability. In addition, the new year is expected to benefit from further efficiencies and improved profitability, tighter control of working capital and new product developments.

Overall then, there seems to be pretty slow progress being made here but there is just about enough interesting new products and improved efficiencies going forward to keep me interested for now.