GVC has now released their final results for the year ended 2016.

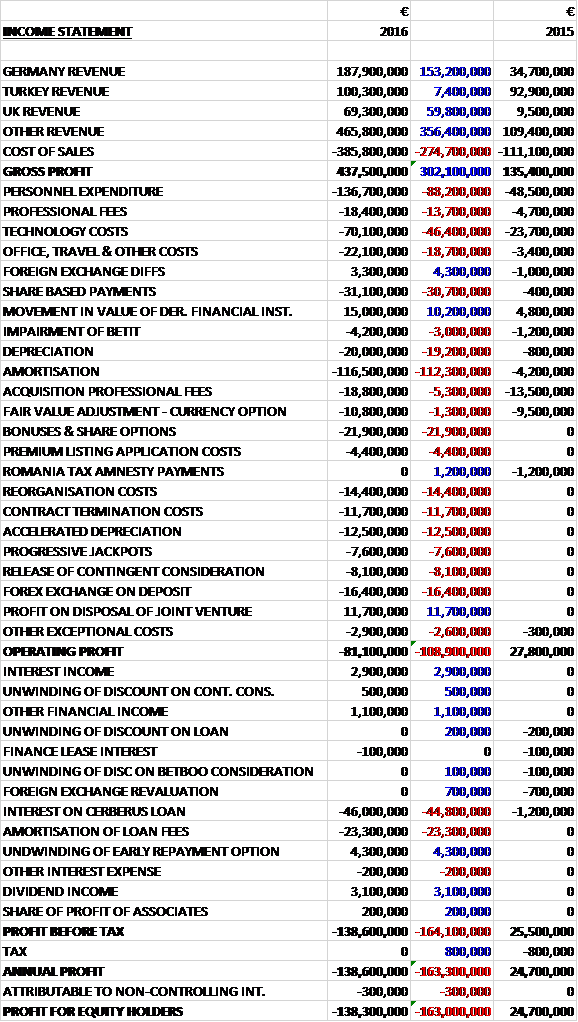

Revenues increased when compared to last year with a €153.2M growth in German revenues, a €59.8M increase in UK revenue and a €363.8M growth in other revenues. Cost of sales also increased to give a gross profit €302.1M ahead of last year. Personnel expenditure was up €88.2M, technology costs increased by €46.4M, share based payments grew by €30.7M, and amortisation was up €112.3M. There were also a number of smaller one-off costs including a €21.9M charge relating to share options, €14.4M of reorganisation costs, €11.7M contract termination costs relating to a legacy affiliate agreement on non-commercial terms, €12.5M of accelerated depreciation relating to certain software licences which were renegotiated following the acquisition, and a €16.4M forex charge on the deposit paid for the acquisition. There was an €11.7M profit received for the disposal of a joint venture however. Nevertheless there was an operating loss this year, which represented a deterioration of €108.9M over last time.

There was an increase in interest income and other financial income but the big finance costs were a €44.8M growth in the interest on the Cerberus loan and a €23.3M fee for the amortisation of loan fees. There was not tax and the loss for the year came in at €138.3M, a deterioration of €163M year on year.

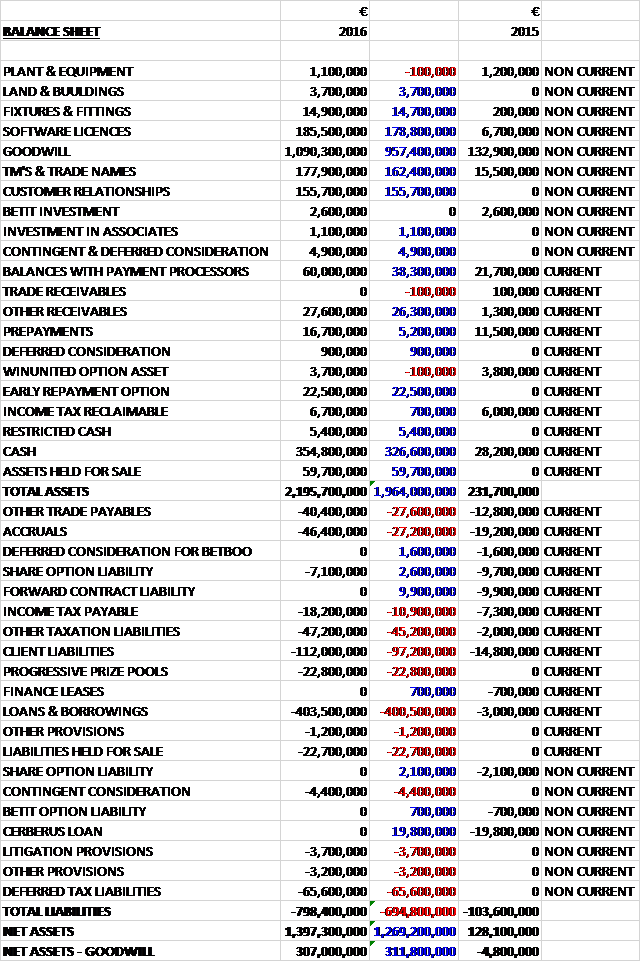

When compared to the end point of last year, total assets increased by €1.964BN driven by a €326.6M growth in cash, a €957.4M increase in goodwill, a €178.8M growth in the value of software licenses, a €162.4M increase in trade names and a €155.7M growth in the value of customer relationships. Total liabilities also increased during the year due to a €380.7M growth in borrowings, a €97.2M increase in client liabilities, a €65.6M increase in deferred tax liabilities, a €45.2M increase in other tax liabilities mostly relating to betting taxes, a €22.8M increase in progressive prize pools, a €27.2M increase in accruals and a €27.6M growth in other trade payables. The end result was a net asset level of €307M (excluding goodwill), a growth of €311.8M year on year.

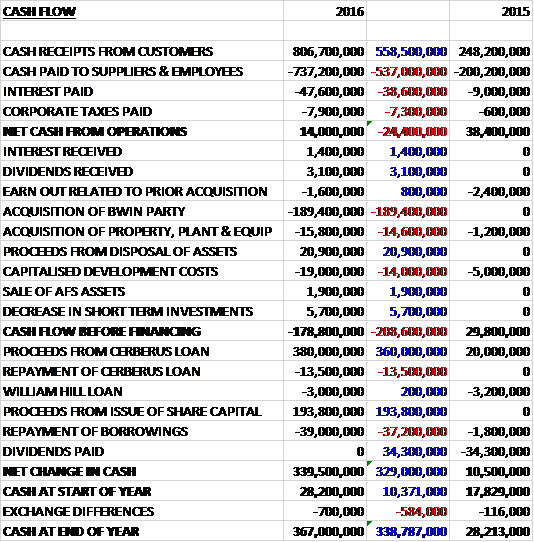

Cash receipts from customers grew by €558.5M but cash paid to suppliers and employees increased by €537M, interest payments were up €38.6M and tax payments increased by €7.3M to give a net cash from operations of €14M, a decline of €24.4M year on year. The group spent more than this, €19M, on development costs and paid out €15.8M on property, plant and equipment. They did receive €20.9M from the disposal of assets but the €189.4M spent on the acquisition meant that before financing there was a cash outflow of €178.8M. The group had a net €324.5M of new borrowings along with €193.8M from issuing new shares so the cash flow for the year was €339.5M and the cash level at the year-end was €367M.

The contribution from the sports labels was €342.5M, a growth of €228.9M year on year. On a like for like basis, sports NGR was up 9% on a margin that grew from 8.6% to 9.6% due to the improvements made at bwin, particularly in the area of risk management which led to a significant reduction in low margin turnover. The year also benefited from the UEFA Euro 2016 tournament, during which the group took €162M of wagers and achieved an impressive gross win margin of 18.3%.

Gaming and other NGR was up 18% on a pro forma basis. During the year the group significantly expanded their gaming offer to their sports customers. Over 17 deals were signed with suppliers which gives them access to over 650 new games across mobile and desktop. Together with improved cross-sell at the acquired businesses, this helped the NGR rise by 18%.

The contribution from the Games labels was €82.9M, an increase of €61.1M when compared to last year but pro-forma games labels NGR fell 5%, although it was flat at constant currency. Momentum improved through the year, however, with constant currency NGR up 4% in H2. The contribution also declined due to a number of factors such as increased gaming taxes and investment in partypoker. Despite the continued structural challenges in the poker market, partypoker NGR increased by 14% with a 16% growth n H2. In December the group reached a deal with one of Europe’s leading poker rooms, Dusk to Dawn, to launch a new live global poker tour, partypoker live.

They also took the decision to restructure partycasino and separate the brand from partypoker, repositioning the brand under a new management team. Taking inspiration from Casino Club, there is greater emphasis on VIP management and reducing reliance on partypoker in terms of customer acquisition. Improvements were made to the product and customer services before relaunching the brand in the second half of 2016. This included the relaunch of the partycasino front end, enhancements to the live casino experience, the introduction of the new pro series table games and a number of technical improvements such as the reduction of game load times. As a result partcasino saw a significant acceleration in new player acquisition through H2 along with lower attrition and increased revenues per customer. December was particularly strong and this momentum has continued into 2017.

The bingo brand Foxy has had a challenging few years. In the second half of the year they brought in a new head of bingo and significant work has already been undertaken to reinvigorate the brand and customer proposition. New creative and media agencies have been appointed and in March 2017 a new marketing campaign was launched.

Casino has established a leading position in German speaking markets and last year saw the brand take control of its software platform, previously provided by a third party, while delivering a positive top line performance. Gioco Digitale is the second largest bingo brand in Italy and is aimed at the casual player. There was some restructuring after the acquisition with improved marketing, promotions, CRM and product and as a consequence, NGR grew strongly. All of the gaming labels are also benefiting from the many new content deals signed over the past year.

As with sports labels, mobile revenue from games labels grew strongly in the year and is expected to continue to do so. Looking ahead, the focus will be on continue product development across all the brands along with improved customer service. As well as the significant amount of new third party gaming content already secured, the group is also accelerating the development of its own unique in-house products.

The contribution from the B2B business was €13.1M which represents a maiden contribution although on a pro-forma basis it represents a €100K growth. The board will pursue B2B opportunities that are meaningful but only where there is no distraction to their core B2C operations or those that do not compromise their long term strategy. As such, the B2B agreement with Betfred was mutually terminated.

At the end of the year, they strengthened their B2B relationship with Borgata and the MGM Group. Under the new deal, they will provide an expanded offering beyond Borgata to additional MGM brands in New Jersey with the potential for the partnership to be extended into other US states as and when regulation permits. They are still committed to B2B and have an active pipeline of opportunities in line with their strategic focus.

The loss from the non-core business was €1M. This business comprises the financial business, Inter Trader. It undertook a restructuring during the year consolidating to a single brand and brining in-house a significant part of the operation that was previously outsourced. Whilst this created some disruption in Q3, the business enjoyed its strongest trading period of the year in Q4. In December they announced the disposal of payments processor Kalixa for a cash consideration of €29M which is expected to complete in the first half of 2017.

A key driver of the business during the year was the performance of the bwin sports label across its core European markets. Whilst sports results were generally positive, this was just one component part of their success in the year. During the year the value of first time deposits across the acquired bwin sports labels rose 37% while improved product and more effective cross sell saw games revenue from sports customers increase 26%. Historically partypoker and partycasino were some of the most challenging parts of the acquired group, partly reflecting the structural challenge in the poker market. During the year, NGR from partypoker increased 14% in constant currency, however, as a result of a change in management, increased investment and a more focused approach.

Obviously the key event from the year was the acquisition of bwin.party for a total consideration of €1,506.6M in February. This included €1,201.5M of GVC shares, €278.5M in cash and €26.6M of cash settled options. In 2015 the business made a loss of €40.2M but following the acquisition the group has already achieved significant synergistic savings through integration and restructuring of operations and expects further benefits in 2017. The acquisition generated goodwill of €963.9M.

The integration of the business was a key focus of the year and whilst all such large scale transactions present challenges, the assimilation of the business progressed positively and is ahead of initial expectations. They remain on target to secure €125M of synergies by the end of 2017 with the full impact being derived in 2018. Additionally, annual capex is expected to be about €20M lower per annum than the combined group spend in 2015.

The preparatory work to migrate the Sportingbet and associated brands onto the bwin platform has largely been completed with three countries already switched over. Given the strong underlying performance of the business the board have decided to further mitigate the risk of disruption by starting the migration of the larger territories once the relevant football seasons have finished. The synergy target of €125M by the end of 2017 remains on schedule, however.

The board felt the organic growth opportunity of the enlarged group is greater than originally expected and a key strategic theme in 2017 will be increased investment in marketing to fully exploit this potential. They are also excited about the cross-sell opportunities presented by the migration of Sportingbet and other associated brands to the bwin platform. This platform has proven to be particularly effective in enabling the cross-sell of other products to sports customers and penetration rates are now double that achieved across the Sportingbet platform.

In February a further €380M was drawn down under the Cerberus loan facility which had a repayment date of September 2017 but the loan was repaid in January 2017, just after the year-end, and an alternate bridge financing facility of €250M provided by Nomura was drawn down. This loan itself was then replaced with a long term institutional loan in March consisting of a €250M term loan and a €70M revolving credit facility. Given the refinancing agreement there is considered to be a minimum sensitivity of the inputs to the valuation. The value of the early repayment at the year-end was €22.5M.

Following the drawdown of the Cerberus loan the group held a large position in GBP to meet working capital requirements. This resulted in a forex loss following the devaluation of sterling during 2016. This amount has subsequently been used in 2017 to hedge against significant GBP liabilities which have arisen including the dividend paid in February and repay the Cerberus loan. The group is exposed to currency movements in the euro, arising out of changes in the fair value of financial instruments which are held in non-euro currencies.

In August the group was admitted to the premium segment of the official list and a month later joined the FTSE250.

The group has classified its Kalixa business as held for sale. The business, a fully integrated digital payments company was acquired as part of the bwin.party acquisition. Certain of the assets of the business relating to a beneficial shareholding in Visa Europe were realised in the year on the sale of that business to Visa Inc.

Management have agreed a sale of the majority of the remaining Kalixa business and believe a disposal in Q1 2017 will be achieved with the remainder of the business also being actively pursued for disposal in the year.

During the year the group disposed of its joint venture investment in Conspo which has also previously been classified as held for sale. Proceeds of €16.4M including deferred consideration of €1.9M gave rise to a profit on disposal of €12.4M.

A currency option was taken out in 2015 in order to meet the cash confirmation requirements of the offer for bwin.party. Under the terms of the contract, the group would sell €365M and buy £260.7M and on valuation at the end of 2015, there was a fair value liability of €9.9M. The option was exercised in February 2016 and the movement of the exchange rate between the end of 2015 and that date created an additional fair value loss of €900K. The combined cost of the instrument of €10.8M was recognised as an exceptional item.

One thing that is still an issue at this company is the huge amount of money and shares that the directors pay themselves. There are currently 22,619,227 options outstanding, most of which have an option price of 422p so I make the value of these at 713p around £65.8M! Sadly, though, Finance Director Richard Cooper is retiring from the board having joined in 2008. He is being replaced by Paul Miles.

The regulatory landscape is changing at a rapid pace, particularly across Europe with the regulatory regimes across the EU member states differing significantly due to the lack of harmonising gaming rules at an EU level. During the year about 69% of NGR was derived from territories where the group pays gaming taxes or where a licensing structure is in the process of being implemented. They are currently licensed in more than 18 territories.

In Germany, bwin was among the twenty successful applicants for a sports betting license in 2014 but this process was subsequently suspended after being challenged by operators who failed to secure licenses and licenses were never granted. Nevertheless, all 35 operators that fulfilled the minimum criteria in the licensing procedure will receive temporary sports betting licenses at the start of 2018. With the exception of one state, licenses for casino and poker are still not available in the country but it was announced in November that the German federal states agreed to evaluate a legal framework for the regulation of online casino and poker which will most likely be concluded in the autumn of 2017. The group pays tax on all of its German revenues.

In the year the group received a permanent license in Romania having previously operated under an interim license. A license application has also been made in the Czech Republic following new legislation that came into force at the start of 2017. The group will consider applying for a license in Poland in light of amendments to their gaming legislation.

In August the UK government will start levying the point of consumption tax on gross gaming revenue on all online gaming products (previously it was just betting) as opposed to NGR. If this had been in place at the start of 2016 the estimated increased tax charge would have been €7M. Also in the UK, the CMA is undertaking a review into the advertising of gaming and operators terms and conditions, particularly in the area of promotions to customers.

Beyond the impact of currency movements, there has been no visible impact on the business from the UK’s decision to leave the EU. The group has higher sterling costs than revenues so the impact is a net positive so far. The detail of how the UK intends to exit the EU is yet to be decided but management believe the group’s global footprint gives it significant flexibility to face any challenges that may arise.

So far this year, in Q1 daily NGR is up 15%, daily sports labels NGR is up 18% and daily games labels NGR has increased by 6%. This growth has been achieved despite some high profile customer friendly results in Europe. Although there is no major football tournament this year, the trajectory in the business together with a return to more normalised levels of marketing means that the board expect to achieve further growth in the coming year.

As the group made a loss there is no PE ratio for this year but on next year’s consensus forecast the ratio stands at 14. Due to the acquisition the group didn’t pay any dividends last year but so far this year have declared 30c and this year’s consensus forecast puts the shares on a yield of 3.8%. Going forward the group are aiming pay out no less than 50% of free cash flow in dividends. At the end of the year the group had a net debt position of €183.5M compared to €6.4M at the end of the prior year.

Overall then this has been a very important year for the group with the transformational acquisition of bwin.party. Due to the acquisition the group made a loss this year and the operational cash flow declined (although it remained positive). Sports NGR was up, aided by improved risk management in the acquired business and the FIFA Euro championships. Games labels saw a decline in NGR, partly due to a host of new taxes imposed on the industry, but this improved in the second half with a lot of the acquired brands benefiting from new operational improvements. The B2B business was broadly flat and does not seem to be a major focus for the group.

The integration of bwin.party seems to have gone very well and the finance has been sorted early, moving away from the crippling Cerberus loan. There will be some headwinds this year in the form of no major football tournament and the UK POC taxes but Q1 has started well and the group are on track to make considerable synergy savings. With a forward PE of 14 and yield of 3.8% I think these shares offer decent value and continue to hold.

On the 25th May the group released a trading update covering Q1. Sports daily NGR was up 13%, sports brands gross win margin increased by 1.1% to 9.6% despite customer friendly results at the end of march, sports brands daily NGR was up 16% and games brands daily NGR increased by 4% with partypoker seeing a particularly impressive performance. So far in Q2, group daily NGR is up 16%, sports gross win margin increased further to 10% and daily sports wagers are up 10%. Comparatives will get more challenging as the group moves through the rest of the year, particularly in the absence of a major football tournament this summer but overall things seem to be going well here.

On the 1st June the group announced that it sold its payment processing business Kalixa for a total consideration of €29M in cash. The sale will have a neutral effect on EBITDA and Kalixa will continue to provide payment processing to the group after the sale.

On the 6th July the group released a trading update for the first half of the year. Group daily NGR was up 12% at constant currency with Q2 daily NGR up 10%. Overall trading is in line with management expectations.

In Q2, daily NGR was up 10% at constant currency despite the absence of a major football tournament. Excluding Euro 2016 revenues, daily group NGR was up 15%. Within sports brands, daily wagers were broadly flat against a comparator that contained Euro 2016 but daily gaming NGR increased by 18%, continuing to benefit from improved product and CRM.

Games brands daily NGR increased 15% driven by partypoker and an improving performance from the standalone casino brands. Overall this is a good performance and with an increase in marketing investment in H2 to more normalised levels gives the board confidence of delivering another year of strong progress. I continue to hold but may buy more following a recent decline in the share price.