GVC has now released its interim results for the year ending 2016.

Revenues increased when compared to the first half of last year with a €176.6M growth in sports revenue, a €70.5M increase in gaming revenue and a €5.6M B2B revenue. Variable costs were also up but gross profits increased by €135.5M. Wages and salaries were up €41.4M, professional fees increased by €6.2M, technology costs grew by €20.9M and office, travel and other costs increased by €8.8M with a €4.4M positive movement in forex. We also see a €6.3M growth in share option charges, a €10M increase in depreciation and a €53.3M hike in amortisation. There was a also a plethora of non-underlying costs with the most significant being an €8.6M increase in fees arising on the Bwin acquisition, a €42.3M of other acquisition costs, €12.5M on accelerated depreciation relating to a new IT contract which will save on licensing costs going forward, and €7.6M of “progressive jackpots” following a change in accounting judgements to give an operating loss with a detrimental movement of €79.2M. We then see a €31.1M interest charge from the Cerberus loan which meant that the loss for the period was €84M, a detrimental movement of €100.8M year on year.

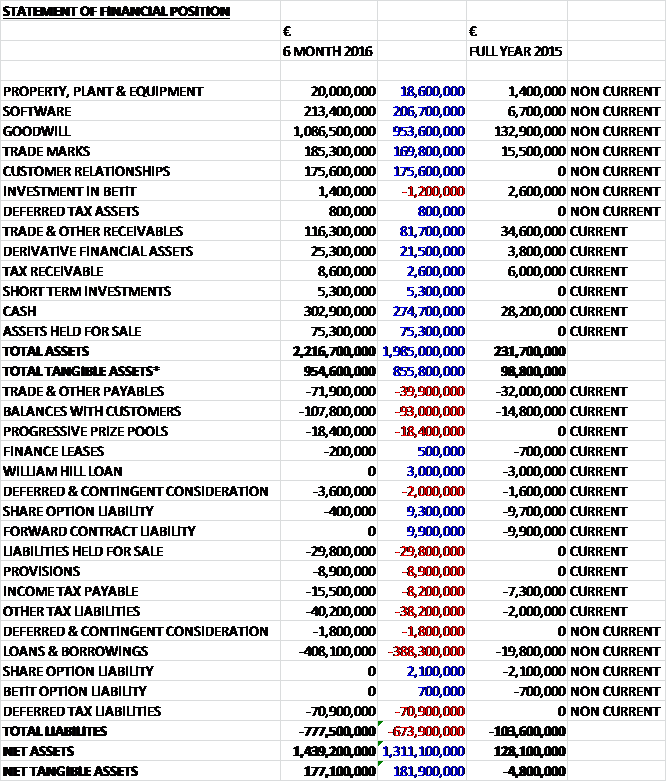

When compared to the end point of last year, total assets increased by €1.985BN to €2.216BN driven by a €953.6M growth in goodwill, a €206.7M increase in the value of software, a €169.8M growth in the value of trademarks, a €175.6M increase in customer relationships, a €274.7M growth in cash, an €81.7M increase in receivables and a €75.3M growth in assets held for sale. Total liabilities also increased due to a €388.3M growth in loans, a €93M increase in balances with customers, a €39.9M growth in payables, a €38.2M increase in other tax liabilities, a €70.9M growth in deferred tax liabilities arising on intangible assets acquired in the acquisition and a €29.8M increase in liabilities held for sale. The end result was a net tangible asset level of €177.1M, a growth of €181.9M over the past six months.

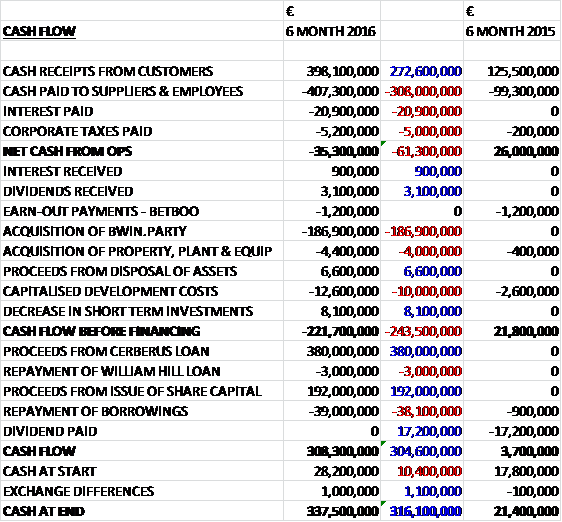

The group received cash of €398.1M from customers but paid out €407.3M to suppliers and employees with some €20.9M in interest payments and €5.2M in cash to give a €35.3M cash outflow from operations, a detrimental movement of €61.3M year on year. They did receive €3.1M in dividends but paid out €186.9M on the acquisition and €12.6M on development costs to give an outflow of €221.7M before financing. They received €192M from issuing new share capital and a net €338M in new loans to give a cash flow of €308.3M and a cash level of €337.5M at the period-end.

The sports betting business contributed €157.6M in the period, a growth of €103.4M year on year with the pro-forma increase being 19% to €177.7M. Sports wages in the half increased by 5% on a pro forma basis despite an increase in win margin from 8.1% to 9.1% as the group exited some unprofitable bwin turnover. Whilst sports results were a factor in the higher win margin, there was also a significant impact from improved trading and risk management practices within the bwin business.

The Euro Championships were a key highlight in the period with the group taking some €162M in wagers on the event across the whole of the tournament (65% in H1) with a gross win margin of 18.3%. Throughout the period both Sportingbet and Bwin significantly increased player acquisition, while customer acquisition costs were also reduced, with a particularly notable reduction recorded by bwin, which benefited from a greater focus on measurable acquisition.

The integration of the group’s CRM strategy and technology into bwin.party was an early priority. Having begun this progress in Q2, incremental improvements are now being integrated on a weekly basis. Initial results are encouraging; during the period as a whole, player reactivation was up, player cross-sell to casino increased while player churn was reduced. Gaming NGR derived from sports labels rose 20% during the period, driven by the improved cross-sell as well as an improved product offer.

During the first half the group signed new contract deals with a number of suppliers, including Evolution, Play n Go and Yggdrasil with over 500 new casino games available to the group’s sports label customers.

The cumulative effect of these improvements in Q2 saw bwin achieve its highest level of quarterly customer deposits and NGS of the last three years, while Sportingbet recorded an all-time high in player acquisition, customer deposits and NGR. Improved cross-sell has already begun to drive revenue growth and much more is expected to come through the combination of further product and marketing enhancements.

The online gaming business contributed €38.2M in the period, an increase of €27M when compared to the first half of last year but pro-forma contribution fell by 19% to €44.4M with the reduction driven by currency weakness and a competitive bingo market along with increased gaming taxes in Austria and Germany. The group have introduced some new products, improved the marketing toolset and hired a number of experienced industry professionals. They began to see the benefits of this come through late in Q2 with performance accelerating in Q3. Indeed, Q3 games labels revenue was up 6% in constant currency in the period up to mid-September.

Casino Club has taken ownership of its software platform which will give them greater flexibility going forward. Meanwhile, after a number of challenging years Party Poker has stabilised with revenues in constant currency ahead of the first half of 2015. A competitive market and sterling weakness meant a tough backdrop for Foxy Bingo, however. The Italian gaming business performed well with an improving performance through the period. While the progress being made in terms of product improvement and the strengthening personnel is significant, the real benefits of this are yet to come through. There is more still to come, with additional games and content to come on stream in the coming months.

The B2B business contributed a maiden €5.5M during the period, although the pro forma contribution reduced by 12% to €6.4M. The group have already delivered new content to their B2B customers and expect this to increase following changes made in the business. During the period they signed their biggest B2B contract top date with Betfred, who signed a ten year contract for them to provide a full turnkey online B2B solution for sports and gaming.

Obviously the big event during the period was the acquisition of Bwin.Party for a total consideration of €1,506.6M. This included the raising of new capital from new shares to the tune of €1,201.5M with the rest coming from a cash settlement. The acquisition generated goodwill of €960.1M and last year the business made a loss of €40.2M on revenues of €576.4M. Following the acquisition, the group expects to generate significant synergistic savings through integration and the restructuring of operations.

Plans include the migration of GVC’s sportsbook onto bwin.party’s technology platform, the termination of all sponsorship programmes, restructuring bwin.party’s casino and poker operations including integrating GVC’s poker operation onto the bwin.party platform, operational efficiencies in customer services, IT and marketing functions, and the integration of some back office functions. Since the date of the acquisition, the business has contributed a loss of €7.8M to the group. The integration will be completed by the end of Q2 2017 and the annualised synergy target of €125 will be secured and the ongoing capex requirement of the enlarged group is expected to be around one third less than the €64M pro forma spent in 2015.

The group has classified some of its non-core assets as held for sale. This includes the investment in the Conspo joint venture, a provider of sports content, and its Kalixa business including its investment in Visa Europe. The Kalixa business, a digital payments company, was transferred to assets held for sale and has a net valuation of €41.2M with management pursuing a disposal within the next year. The carrying value of the Conspo investment is €3.9M but it was disposed of shortly after the period-end for a total of €15.3M, of which €13.5M was received in cash.

During the period about 70% of revenues were derived from markets that are regulated or in the process of becoming regulated or where they pay gaming taxes or VAT. They have had their New Jersey license acquired with Bwin confirmed in May and in August they were granted a permanent license in Romania. They expect the Czech Rep, Netherlands and Poland to regulate in the coming year. VAT has been imposed since the start of 2015 in a number of countries, the most significant being Germany and France. VAT at the rate of 21% has also now been introduced in Belgium, a market where the group operates through a locally licensed partner although the financial impact is not considered to be material.

A currency option was taken out last year in order to meet the cash confirmation requirements of the acquisition. Under the terms of the contract the group would sell €365M and buy £260.7M. The derivative, a current liability, was valued at €9.9M at the end of the year. The option was exercised in February 2016 and the movement in exchange rates since the end of the year created an additional fair value loss of €10.8M.

The group also have a number of other options. The Winunited option is valued at €2.8M compared to €3.8M at the end point of last year. The Cerberus loan early repayment option is related to an early repayment of the loan subject to a “make-whole” premium on the interest. Changes in the group’s credit rating will have an impact on the value of the option for early repayment and at the half year point the value of the option stood at €22.5M. The group also had a call option to acquire the balance of the outstanding shares in Betit with the minimum price set at €70M. During the period they disposed of their investment in Betit and the call option which was disposed of as part of the arrangement. The net loss on the disposal has been included within changes in available for sale assets.

As usual the directors of this company have done very well through share options. Some legacy options were cash cancelled during the period on the acquisition of Bwin and the proceeds of £5.4M were re-invested in new GVC shares. There were also a lot of new options issued which vest depending on performance. The share based payment charge of the new options was €6.5M and the value of the options is €15.8M.

After the period-end, the group disposed of its investment in the Sportsman Leisure Industry Solutions with a profit on disposal of €11.5M. Under the terms of the Cerberus loan facility, the group has an obligation to utilise the cash proceeds of a business disposal as a mandatory repayment so the net cash proceeds were used to repay €13.5M of the outstanding loan balance.

In August the group announced they had entered into a commitment with Nomura for a replacement of the existing financial arrangements. The €250M proceeds of the new financing are to be applied towards the repayment of the Cerberus loan with the balance being repaid from existing cash reserves. The new facility has an initial maturity of one year from the signing of the loan agreement with options to extend for up to twelve months. After the period-end the group was also admitted to the premium section of the official list and joined the FTSE 250 in September.

It was also announced that CFO Richard Cooper is to step down from the board in February, to be succeeded by Paul Miles.

Beyond the impact of currency movements there has been no visible impact on the business from the Brexit vote. The group has greater sterling costs than revenues and therefore the impact of sterling weakness is a net positive. It is worth noting, however, that further changes as a result of the referendum may reduce the group’s ability to operate in certain EU markets without a change in domicile which could carry a higher tax burden. The average daily NGR in the eleven weeks since the end of the half was up 12% on a pro-forma basis and 15% at constant currency. Organic growth opportunities from bwin.party are greater than expected and will be exploited through increased marketing investment and as a result the board are confident of achieving a result at the upper end of market expectations for 2016.

As a result of the acquisition and a combination of the debt covenants and the intended restructuring of the group, the directors have not proposed any further dividends during 2016 but they are committed to the resumption of dividend repayments in 2017. Net debt at the period-end came in at €165.1M but was reduced to €154.3M by the end of July.

On the 3rd November the group released a trading update for Q3 and announced their intention to pay a special 10c dividend in February. Absent of any significant capital allocations or investments and consistent with maintaining appropriate capital ratios, the group plans to adopt a dividend policy of distributing 50% of annualised free cash flow, starting in 2017. It is expected that payments with be biannual.

Pro forma daily NGR for the quarter increased by 12%, and was up 15% in constant currency. Sports gross win margin was 10.5% (9.3% last year) with daily amounts wagered 3% higher year on year. Games and other daily NGR saw growth of 12%. Trading in Q4 has begun positively with pro forma group daily NGR up 8% and 10% at constant currencies despite strong comparatives.

Overall then this has been a period of great change for the group. They are now loss making, although it is hard to get at the underlying situation following the acquisition. The sports betting business is performing well with both margin and wagers up, although both of these were boosted by the Euro Championships. Online gaming seems a little more difficult and in the first half contribution fell due to a tough bingo market and higher taxes in Austria and Germany, although this seems to be improving in the second half.

The integration seems to be going well and the reintroduction of dividends is a welcome move although the increasing taxes and the potential effects of Brexit along with the loss of the CFO are all reasons to be a bit weary. Altogether though, I am happy to remain a holder here.

On the 15th December the group released a trading update where they announced that the strong performance recently reported has continued through Q4. As a consequence the board now expects proforma NGR for the year to be at the upper end of market expectations. In addition, the positive momentum across the business combined with strong cash generation gives the board confidence to announce a 49% increase in the proposed special dividend to 12.5p per share. Over all group daily NGR was up 14% at constant currency, sports daily NGR was up 19% and gaming daily NGR increased by 11%. This all seems positive to me.

On the 19th December the group announced that it has agreed to sell the Kalixa business to Senjo, a global payments operator headquartered in Singapore for a total consideration of €29M payable in cash on completion.

The sale does not include the wallet business which will be closed post-completion. In addition, prior to completion, an amount equal to the free cash over €2.1M in the Kalixa business will be retained by the group by way of a dividend. The sale proceeds will be applied towards reducing the group’s net debt and the sale will have a neutral effect on EBITDA. Kalixa will continue to provide payment processing services to GVC after the sale under an existing contract.

Last year the business generated a loss of €7M and the sale will result in a book loss of around €4M, although €19.2M of the book value of the business was made up of intangibles.

On the 5th January non-executive director Norbert Teufelberger sold 1.3M shares at a value of £8.4M! This is a huge sale but not too unexpected given he was a director of bwin. He retains 1,455,276 shares.

On the 2nd February the group released an update covering the full year. The group has now repaid in full the outstanding loan of €386M provided by Cerberus through a combination of existing cash resources and the drawdown of the €250M loan from Nomura. The loan payments will be some €40M lower in 2017 than would have originally been the case.

NGR per day increased by 7% in Q4 despite some adverse sports results. At constant currency, total NGR was up 9% with sports NGR increasing by 6% and gaming NGR up 11%. The board now expects to report pro-forma group NGR of €894M, an increase of 9% year on year and slightly ahead of previous guidance. The board expect pro-forma clean EBITDA to be towards the upper end of market expectations and net debt of about €140M.

The positive trading momentum experienced in 2016 has continued into 2017 with pro-forma daily NGR up 21% in January. This sounds very good and I continue to hold.