Redrow has now released its final results for the year ended 2016.

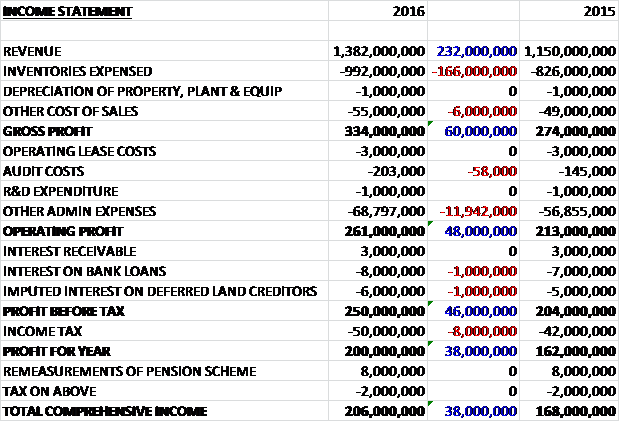

Revenues increased by £232M when compared to last year and after inventory expenses and other cost of sales increased by a more modest amount, the gross profit grew by £60M. Admin expenses increased by £12M and interest costs grew by £2M to give a pre-tax profit some £46M above that of 2015. After tax increased, the profit for the year came in at £200M, a growth of £38M year on year.

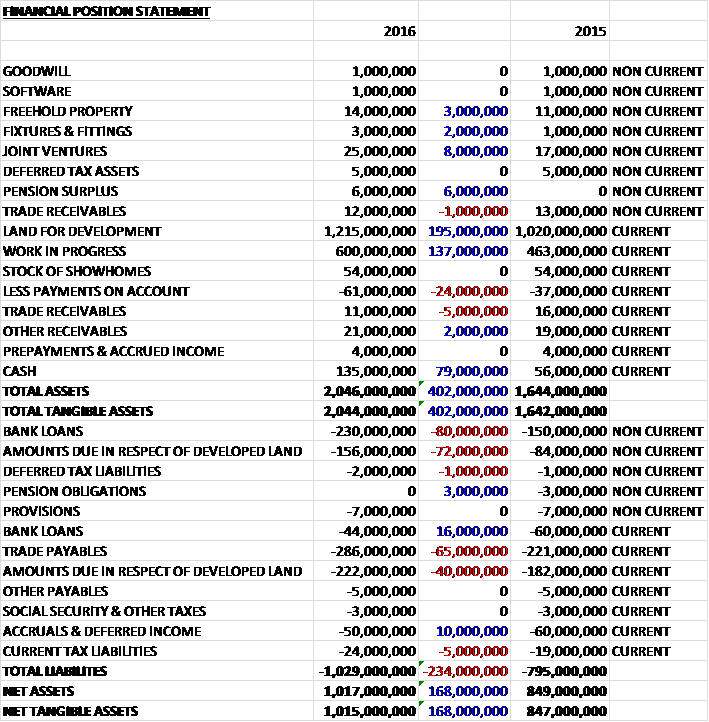

When compared to the end point of last year, total assets increased by £402M to £2.046BN, driven by a £195M growth in land for development, a £137M increase in work in progress and a £79M growth in cash, partially offset by a £24M increase in payments on account. Total liabilities also increased during the year due to a £64M growth in bank loans and a £112M increase in amounts due in respect of developed land. The end result was a net tangible asset level of £1.01BN, a growth of £168M year on year.

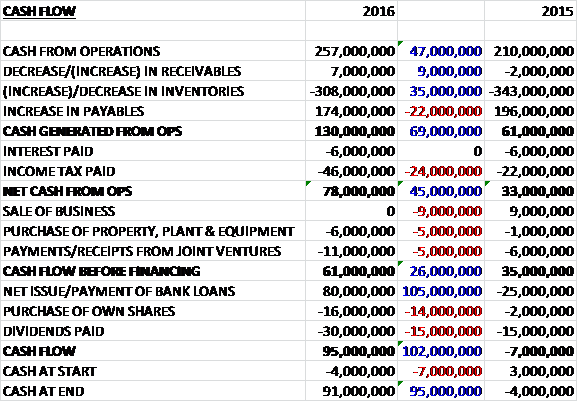

Before movements in working capital, cash profits increased by £47M to £257M. There was a cash outflow from working capital with a growth in inventories, but this was less than last year and after tax payments grew by £24M, the net cash from operations came in at £78M, an increase of £45M year on year. The group spent £6M on fixed assets and £11M on joint ventures to give a free cash flow of £61M. They then took out £80M in new loans to purchase £16M of their own shares for director bonuses, and they spent £30M on dividends to give a cash flow of £95M and a cash level of £91M at the year-end.

Revenues from residential legal completions increased by 26% due to a 17% rise in legal completions to 4,716 combined with a 7% increase in the average selling price to £288.6K. The gross margin improved to 24.2%, mainly due to most of the completions coming from sites purchased after the downturn with the remaining plots purchased before the downturn likely to be sold by the end of 2017. The divisions in the South grew most strongly and the new SE division made a valuable contribution to results in its first year of trading.

The market in the year was stronger than in 2015 with a seasonally stronger performance in the second half of the year. Demand for new homes was strong throughout the year and the growth in output has benefitted from the government’s Help to Buy scheme which has continued to be a major support. At the higher end of the market, in particular in Central London, sales have slowed, mainly as a result of the Stamp Duty changes that came into effect last year and further hikes that came into effect in April this year. Activity in this section of the market remains sluggish but the group’s exposure is very limited and other operational areas such as Outer London have shown strong growth. They have seen very little impact as a result of the Brexit vote.

The group had a successful year in acquiring land and obtaining planning permission on their forward land holdings with the owned and contracted land bank increasing to 26K plots, although obtaining planning through Local Authorities remains tortuous. They benefited from an exceptional pull-through from the forward land portfolio that included 2,900 plots at Colindale in North London.

The group entered the new year with a record private forward order book of £807M, up 54% on the previous year; including social housing, the total forward order book is £897M, up 51%. Sales in the first ten weeks are encouraging and up 8% on a strong comparison last year. They have recently launched a number of significant new sites and have a strong pipeline in the planning process. The strategy continues to grow the business, increasing the number of outlets and the number of homes they build. This process is on track and the board are confident that this will be another year of significant progress for the group.

At the current share price the shares are trading on a PE ratio of 7.4 which falls to 7.2 on next year’s consensus forecast. After a 67% increase in the full year dividend, the shares are yielding 2.5% and I can’t find a forecast covering the dividends. At the year-end, the group had net debt of £139M compared to £154M at the same point of last year.

Overall then this has been a strong year for the group. Profits were up, net assets increased and the operating cash flow improved with plenty of free cash being generated. Legal completions were up strongly and selling price also increased, albeit more modestly. The group are working through their legacy plots purchased before the downturn and should be finished with them next year. The housing market is pretty decent, although the stamp duty changes have weakened the Central London high end market and although Redrow don’t have much of an exposure to this, the risk is that the slow-down trickles down.

So far this year, sales are up again and the shares look cheap with a forward PE of 7.2. The dividend yield of 2.5% is not much to get excited about nut nonetheless, the shares look interesting to me.

On the 9th November the group released a trading update where they stated that the encouraging sales trend reported earlier has continued. Net private reservations are 6% ahead at 1,660 and the sales rate for the 19 weeks to 4th November is 0.71 per outlet per week, up 4%. Demand remains strong across the majority of sites with buyers continuing to make purchasing decisions well ahead of build programmes. The private order book is currently at £941M, a 29% increase on this time last year.

The average selling price of private reservations in the year to date is £355K compared to £334K, including the sale of the last of the high value apartments in Central London. Excluding these sales, the selling price was up to £341K. Net debt is currently £92M an expected to be at a similar level at the end of the year.

Overall, things seem to be ticking along well here and I am tempted to make a

purchase.