Havelock Europa has now released its interim results for the year ending 2015.

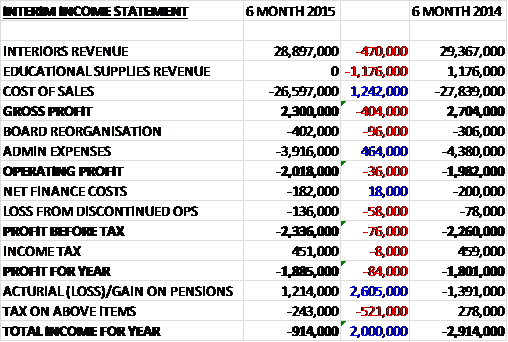

Revenues declined when compared to the first half of last year with a £470K fall in interiors revenue and a £1.2M decline in educational supplies revenue as the Stage Systems division is consolidated into the interiors segment. Cost of sales also fell to give a gross profit some £404K below that of last time. The board reorganisation relating to loss of office compensation and fees for the recruitment of a new CEO and finance director, cost some £402K and the slight increase was more than offset by the £464K decline in admin expenses so that the operating loss increased by just £36K. Finance costs fell, but tax was up slightly and the loss from the discontinued operation (Teacherboards) grew by £58K so that the loss for the half year came in at £1.9M, a growth of £84K year on year.

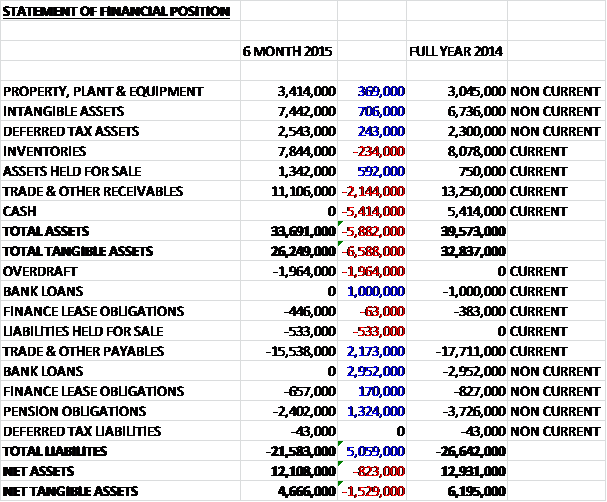

When compared to the end point of last year, total assets fell by £5.9M driven by a £5.4M decline in cash and a £2.1M decrease in receivables, partially offset by a £706K growth in intangible assets and a £592K increase in assets held for sale. Liabilities also fell during the period as a £4M fall in bank loans, a £2.2M decline in payables and a £1.3M decrease in pension obligations was partially offset by a £2M new overdraft and a £533K growth in liabilities held for sale. The end result is a net tangible asset level of £4.7M, a fall of £1.5M when compared to the end of 2014.

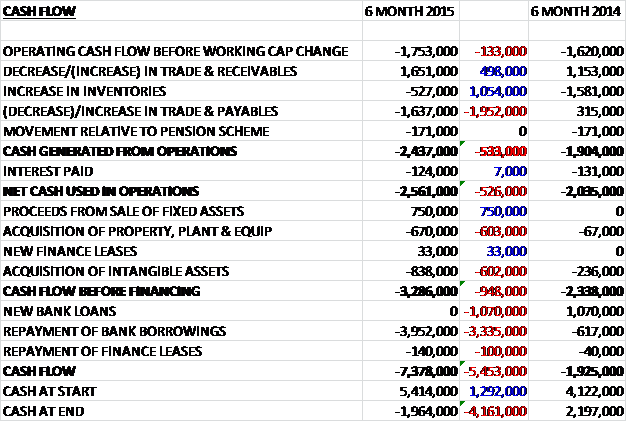

Before movements in working capital, cash losses widened by £133K to £1.8M. A large fall in payables then meant that the net cash outflow from operations was £2.6M, an increase of £526K year on year. The group then made £750K on the sale of property, plant and equipment, most of which was spent on more fixed assets and an £838K acquisition of intangible assets drove the cash outflow before financing even higher, at £3.3M. After the repayment of nearly £4M of borrowings, the cash outflow for the half year stood at £7.4M to an overdraft position of £2M.

Subdued demand in the UK retail and financial services sectors was the main reason for interiors sales reducing by 5% but a £460K reduction in overheads resulted in a slightly lower loss before tax of £1.8M. Within the retail sector, demand from the existing UK client base was soft with many clients now re-evaluating their business cases before committing to invest in their projects. To counter this, the group are focusing on developing the number of customers that they trade with within each sector. Within Retail, they have had some success with this strategy, and began supplying three new major retailers. Within international retail they are beginning to see the benefits of the work done previously and are on track to deliver the 15% of group revenue targeted from this business stream.

Demand in Financial Services has continued to decrease as customers continue to downsize their estates. In addition, a significant framework contract won in late 2014 has not yet delivered the expected turnover as the end client’s programme has been delayed. On a positive note, they are continuing to support the Network Transformation Programme being undertaken by the Post Office and the office fit out market has been targeted as an area for potential growth. They have been successful on a number of projects and are directing resources to maximise this opportunity.

As part of the business reorganisation plan, the board have amalgamated the education, accommodation and healthcare sectors into one public sector services business stream. Activity within these sectors has benefited from a strong 2015 order book and the challenge from the second half of the year is to maximise revenue from these projects as some of them have suffered from on-site client delays which doesn’t sound good. Operationally the business relocated to its new head office and the expected benefits from the relocation are being realised and the group are trying to standardise and simplify the business to make it easier to do business with.

A customer survey undertaken during the period identified the need for immediate changes within the business. Some changes include a proposed reorganisation of the business to reflect changes in the market place with a 10% reduction in staffing levels; a simplification of the business model designed to focus on the customer experience; and the sale of Teacherboards.

Contracts have been placed for future capital expenditure amounting to £306K. After the period-end the group sold Teacherboards for a consideration of £1.4M to Sundeala ltd. The borrowing covenants have been met during the period and the board expect to be able to comply with the conditions in the future based on the most recent forecasts and taking account of mitigating actions that could be taken in periods when headroom is tight – this doesn’t sound that confident.

During the period, David Ritchie succeeded Eric Prescott as CEO and due to overseas commitments the largest shareholder, Andrew Burgess resigned from the board.

Demand within the UK Retail and Financial Services sectors remains subdued and the board expect this situation to continue until the end of the year. Progress on the business reorganisation is being made and they expect to have the major changes implemented by the end of the year which should ensure they enter 2016 with a stable, more efficient business that is better placed to take advantage of any opportunities with annualised cost savings of £3M.

Net debt increased by £500K to £3.1M due to an increase in finance lease obligations relating to the investment in ERP. Obviously there was no interim dividend declared.

Overall then this was a difficult six months for the group. The loss widened but this was due to the board reorganisation and without this, the loss would have fallen slightly. Net assets fell during the period and the operating cash outflow increased year on year. The UK retail and financial services demand was weak and is expected to remain so for the rest of the year. It is difficult to see much positivity here at all actually, I suppose the replacement of Eric Prescott with David Ritchie as CEO is one glimmer of hope and the cost savings achieved by 2016 may set the groundwork for a better performance next year but I will not be buying in just yet.

This chart doesn’t really offer much optimism either…

On the 6th October the group announced the appointment of Peter Dillon as non-executive director. He is a chartered accountant and was finance director of Hargreaves Services from 2003 to 2007, including during the period of their IPO. Ominously, he has was also a director of Parkview Construction which was placed into administration; Underbank Park Farm which was struck off in 2001 and fined for the late filing of accounts; and a consultant to Idess Retail which was places into administration. Mr. Dillon’s family trust, Gold ltd, owns 1.76% of the shares in Havelock.

I am not sure what to make of this, Mr. Dillon’s past directorships do not seem to be that auspicious to me…

On the 17th November the group released a profit warning. The company has been informed by its largest financial services client that it will be substantially reducing its anticipated spend on refurbishment and development next year. As a result, it is forecast that the contracting revenue the group will receive from this client for undertaking branch refurbishment and development programmes will be negligible for 2016 although they will be retained as the preferred furniture provider to the client. The contracting revenues from these programmes this year will be about £14M and will be unaffected but the impact next year will be material before mitigating actions are undertaken. This is a big blow for the company and I don’t think these are investable at the moment. Unless things radically change I will not be doing any more updates on this company.

On the 24th November the group announced that non-exec Peter Dillon purchased 85,000 shares at a cost of £7,650. He now owns some 763,070 shares which is nearly 2% of the entire company. Although nice to see a director buying shares, the amount here looks nothing more than a token gesture to me.

On the 25th January the group released a trading update covering the year of 2015. The business simplification programme is gaining momentum and the cost reductions identified as a result of the programme were achieved by the end of the year. Trading in Q4 was as expected so the board expect the results to be in line with its expectations at the last update. As of the year-end, the group was debt free with net cash of £1M compared to a net cash position of £200K at the end of last year. Although trading remains challenging, particularly in the retail sector, they group is entering 2016 with an order book of £23M for delivery within the year which is 15% up on 2015.

Overall, not a bad update but things remain brutally tough for the group and I am not rushing in to chase the shares higher.