Interserve has now released its interim results for the year ending 2015.

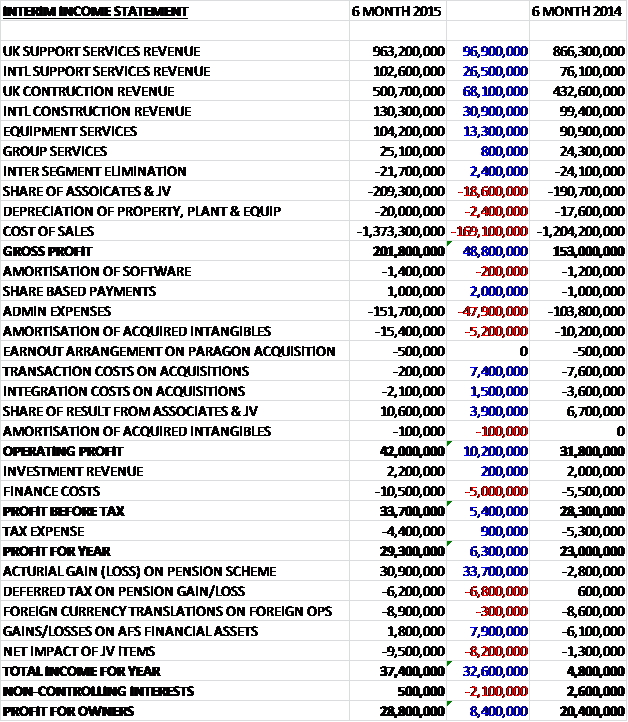

When compared to the first half of last year, revenues increased across all business segments although the proportion attributable to joint ventures and associates also increased. After cost of sales grew by £169.1M, the gross profit increased by £48.8M. We then see a £47.9M increase in underlying admin expenses and a £5.2M growth in the amortisation of acquired intangibles more than offset by a £7.4M fall in transaction costs and a £1.5M decline in integration costs but the contribution from joint ventures increased by £3.9M to give an operating profit for the first half of the year of £42M, an increase of £10.2M year on year. Finance costs nearly doubled when compared to the first half of 2014 but tax costs reduced to give a profit for the year of £29.3M, an increase of £6.3M when compared to last time.

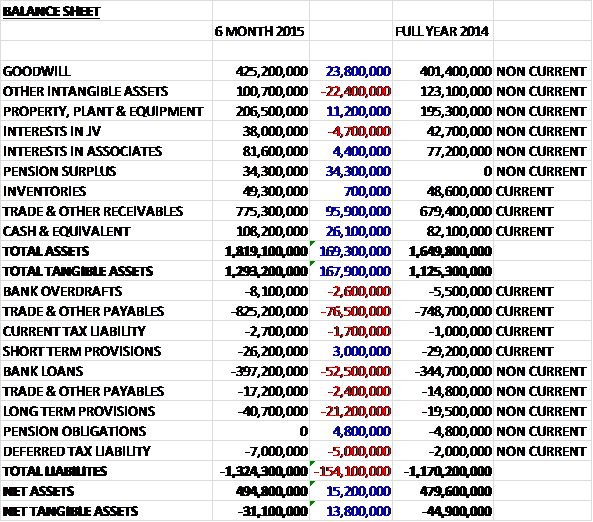

When compared to the end point of last year, total assets increased by £169.3M driven by a £95.9M increase in receivables, a £34.3M growth in the pension surplus, a £26.1M increase in cash, a £23.8M growth in goodwill due to the discovery of loss making contracts at the acquisitions and an £11.2M increase in property, plant and equipment, partially offset by a £22.4M decline in other intangible assets. Total liabilities also increased during the year due to a £76.5M increase in payables, a £52.5M growth in bank loans and a £21.2M increase in long term provisions, presumably related to the loss-making contracts discovered in the acquisitions. The end result is a £13.8M positive movement in net tangible assets but they remained negative at £31.1M.

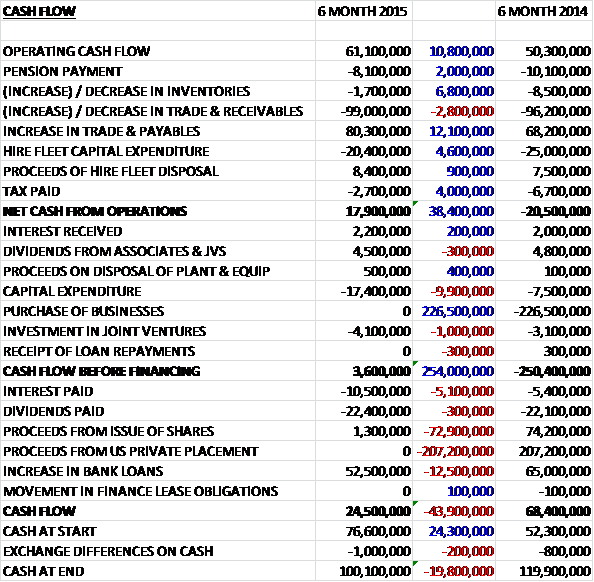

Before movements in working capital, cash profits increased by £10.8M to £61.1M. After an £8.1M increase in pension deficit payments, a £99M increase in receivables and a net £12M spent on hire fleet capital expenditure, the net cash from operations stood at £17.9M, a positive swing of £38.4M. The group then paid a net £8.3M in interest and £17.4M on capital expenditure (with £7M spent on the first stage of investment in a new UK Midlands office) with a broadly neutral contribution from/to joint ventures to give a negative free cash flow of £6.9M. Clearly there was not cash left to pay the dividends so some £52.5M more was taken out against the bank loans to pay the £22.4M in dividends and to give a cash level at the period end of £100.1M. This is not that impressive really.

The profit at the UK Support Services division was £40M, an increase of £6.1M year on year; the operating margin increased from 4.2% to 4.3% and the future workload increased by 7% to £6.2BN – this is now by far the most important contributor to group profit. During the year the group further developed their portfolio of private sector clients, for instance in the transport sector where they won a number of long-term contracts in the rail sector with MTR Crossrail and KeolisAmey Docklands in addition to their existing contract with London Underground. In total these contracts added some £100M to the future workload.

They made good progress in the retail sector too. They secured a three year, £35M extension with B&Q, doubling the scale of the cleaning service and adding catering at around a quarter of the estate. The relationship with Debenhams was extended, in which the group have delivered facilities services across its UK stores and offices for over 25 years. In addition, they have mobilised their contract with Sony Europe to manage the company’s estate in 27 countries.

The public sector business has evolved significantly over the past year and a half with the main changes relating to reductions in revenue from the loss last year of the South East Regional Prime contract and the decrease in size of the new MoD National Training Estate contract compared to previous arrangements. In recent years the group have, though, built capability in the provision of frontline public services across healthcare, welfare-to-work, skills and justice. This growing part of the business includes the expansion of Learning and Employments following last year’s acquisition of the Employment and Skills group. The recently announced pooling of budgets in the Greater Manchester area, covering transport, housing, planning, policing and public health is an early example of how the group’s breadth of capability could be highly relevant to more “place-focused” commissioning.

The profit at the International Support Services division was £4M, an increase of £800K when compared to the first half of last year. The operating margin fell slightly, from 4.3% to 4.2% and the future workload increased by £200M to £300M. During the period the group won an oil and gas services contract with Petrofac in Oman, having initially worked for them solely in the UAE. The focus on servicing essential production facilities as opposed to exploration and helped provide the increase in profits seen in the division.

Other highlights during the period included winning fuel pipeline construction and installation contracts with BP Khazzan, Gulf Petrochemicals Services Company and RasGas, as well as a sea water treatment works contract with Veolia Water. The facilities management businesses won contracts with new clients including the Abu Dhabi Equestrian Club, the Environment Agency of Abu Dhabi and secured further work with IKEA in Qatar. The newly established facilities management business in Saudi Arabia mobilised its first contracts in the period to manage services at the IT and Communications complex and King Abdullah Financial District in Riyadh for the Al Ra’idah Investment Company. The board are encouraged by the prospects for their recently launched joint venture with the Rezayat Group which adds to their delivery capability in the Kingdom.

The profit at the UK Construction division was £5.3M, a decline of £2.7M when compared to the first half of 2014 with the wafer thin margins falling from 1.9% to 1.1%, although the future workload has increased by 22% to £1.7BN. Market demand continued to strengthen during the period which drove revenue growth up but the challenges of the current trading environment, combined with marked supplier cost inflation resulted in margins falling below the medium term expected range. Although tender pricing is improving and the risks associated with supply chain insolvency and pricing inflation are beginning to recede, it is expected that margins will remain tight in the short term.

Work winning in the period was strong and significant items within the additional workload included the group’s appointment as preferred bidder to build a new £200M complex at the Defence and National Rehabilitation Centre at Stanford Hall, further wins in the EfW market at East Lothian and Rotherham, and a contract to build seven secondary schools across Hertfordshire, Luton and Reading.

The profit at the International Construction division was £4.9M, a growth of £600K year on year with operating margins increasing from 2.4% to 3.3% and the future workload edging up 2% at £200K. Demand continued to strengthen across the region and strategic development plans such as Qatar’s Vision2030 and the UAE’s plans for Expo 2020, along with the ongoing need for infrastructure development to keep pace with rapid population growth are all gaining traction and stimulating activity in the market.

Work winning during the period included projects to expand the Doha West sewage treatment plant for the Marubeni Corp, to build a seawater pumping station for a desalination plant in Doha for the Toya Thai Corp and an executive jet terminal at Al Maktoum International Airport for Dubai Aviation City Corp. The group also secured further works with clients such as Dubai’s Road and Transport Authority, Siemens, Petron Gulf and the British School Muscat.

The profit at the Equipment Services division was £18.6M, an increase of £4.6M when compared to the first half of 2014 with the decent operating margin increasing from 15.4% to 17.9% as the division benefited from the fleet investment in improving global infrastructure markets. The group continued to invest in risking markets, albeit at a more modest pace than last year with net capital expenditure of £10.4M which means that over the last year and a half, the group has invested £51M in stock, working capital and net capex, however, it is expected that the rate of expansion in the asset base will continue to ease in the second half of the year.

In Asia Pacific, the group delivered strong performances in Hong Kong and the Philippines driven by increased investment in infrastructure projects including the Kowloon Rail Terminus, the Hong Kong Macau Bridge and the Manila Bay Development. Demand in Oceania, however, remains muted following the conclusion last year of a series of major mining related projects with no current prospect of future capacity expansion.

The group continued to see strong growth in the Middle East, benefiting from increased demand in Qatar where a number of large scale infrastructure projects are now underway, including the East West Highway project where Interserve are supplying equipment on several bridge structures. Demand also continued to grow in the UAE where work has been delivered on the Dubai Opera House, the Saadyatt Resort in Abu Dhabi and on the new Dubai-Abu Dhabi highway. In Saudi Arabia, the group started work on a new 14 storey transport hub being built in Mecca. The UK continued to benefit from increasingly confident construction markets with a significant pipeline of road projects offering potential to replace work on more mature schemes such as Crossrail. Work continued on sizeable rail improvement projects in Reading and on the Stockley Viaduct project near Heathrow airport.

The losses at the group segment widened by £2.8M to £12.5M year on year. This segment now includes the investments which were formerly reported separately but following the disposal of the majority of the PFI portfolio are longer judged individually material. The increased costs were driven by the initial investment in the construction of a new Midlands office where the group will consolidate their back office activities.

For the acquisitions of Initial Facilities and Esg last year, the fair value of the assets acquired was provisionally assessed at the time and included in the 2014 accounts. Since the year-end these assessments have been updated by £19.7M to reflect the impact of loss making contracts on which constructive and legal obligations existed at the time of the acquisitions. There is no profit/loss associated with this as it has just been added to the goodwill paid for the acquisitions (as it should be given the accounting treatment of goodwill). I have to say this just underlines what a ridiculous asset goodwill is and why I always discount it when determining net assets – due to loss making contracts being discovered which will lead to a reduction in the performance of the acquired businesses than expected, the goodwill asset goes up! I really think there should be a change to the treatment of goodwill but I am not an accountant so perhaps I am missing something.

During the period the company concluded negotiations on the triennial valuation of the pension scheme. Since the last time the exercise was carried out they have undertaken considerable efforts to de-risk the liability position and increase the asset strength through the pension buy-in and contribution of £55M of PFI assets respectively. The effect these actions had was to recognise a pension asset of £34M on the balance sheet compared to a deficit of £93M three years ago and an actuarial deficit of £64M compared to £150M at the end of 2011. In addition it has been agreed that the existing recovery payments of £12M per annum would continue until the next valuation. This is a huge amount of deficit reduction payments, I didn’t actually realise they were so high but the progress made on the deficit reduction so far is rather impressive in my view and it is much less of a risk than it has been in the past.

The future workload rose by 11% over the past year to £8.3BN and demand in the group’s main markets continued to strengthen which gives the board confidence in their positive outlook. This is the good news. The not so good news is the fact that the board expect the national minimum wage announced in the recent budget to have an adverse impact on margins in the UK support services segment of between £10M and £15M next year, receding over the next few years thereafter as the change is prices in to relevant contracts. This will not affect the second half of 2015, however, and the board’s expectations for growth in 2015 overall remains the same.

At the period end net debt stood at £297.9M compared to £268.9M at the end of last year and £243.1M at the half year point of 2014. After a 5% increase in the interim dividend, at the current share price the shares are yielding 4.2% which increases to 4.5% on the full year consensus forecast.

Overall then this is a bit of a mixed update. Profit for the half year increased but when last year’s transaction and integration costs are taken out of the equation, profit fell year on year. Net assets did improve though, mainly due to the revaluation of the pension which validates a lot of the hard work done on the scheme in recent years, but net tangible assets remained negative which is never great for this kind of company. The operating cash flow also improved but there was no free cash available and the payment of the dividends pushed the net debt level ever higher.

Operationally, the UK support services business and the equipment services business are pretty much driving the group now, both improved year on year, no doubt helped by the Initial acquisition in the case of the former. Internationally, the group seems to be doing well in Qatar and the UAE with Saudi Arabia now offering some decent work. The problems are in the UK construction division, however, with wafer thin margins made even worse by supplier cost inflation. The discovery of the loss making contracts in both of the acquisitions is disappointing and the fact that the minimum wage announcement will cost the group between £10M and 15M next year is a real blow, especially considering that division is where most of the growth is coming from.

The shares unsurprisingly took the above news badly and now yield 4.5% on the full year consensus which is a nice amount to have but I have to say the concern over profitability next year is keeping me out at present.

This is quite an interesting chart. The recent uptrend seemed to break down in mid-June and the share price has gapped down following yesterday’s update.

On the 13th November the group released a Q3 trading update. The group’s markets have experienced mixed conditions over the past three months but the group’s outlook for the full year remains unchanged with expectations for continued growth.

Construction has continued to strengthen in the Middle East, reflecting their focus on key clients in retail, leisure and infrastructure so the board expect results in the international construction division to show positive progress year on year. In the UK, while the performance of the building and fit-out business is encouraging, this year’s result will be impacted by three loss making energy process contracts within the infrastructure business. This is due to sub-contractor insolvencies and the consequential impacts in project timing and costs. The group’s involvement in the delivery of these contracts is substantially complete, however. Due to these issues, the board expect a break-even performance for the full year in the UK construction segment.

Equipment Services has continued to deliver good growth, fuelled by strong demand and benefiting from the increased scale of the hire fleet in which they have invested in recent years. Trading is particularly strong in parts of the Middle East, the Far East and the UK, more than offsetting volume reductions from the downturn in Australia.

Anticipated year-end net debt remains unaltered in the range of £270M to £300M and the visibility of future workload remains encouraging with 60% of 2016 consensus revenues secured by the end of Q3. Since the half year results, the group have won new contracts and extensions with Siemens, Hilton Hotels, Petrofac, Qatar Cool, the Department for Transport, Durham Uni, York Uni, Warwick Uni, Scottish Power and Northern Powergrid.

The group have also announced that Glyn Barker will join the board as Chairman after Lord Blackwell announced his intention to stand down. Glyn is a non-executive director of Aviva and Berkeley Group and until December 2011 was vice Chairman of PWC UK. He also held a number of other senior positions at PWC including UK Managing Partner and UK Head of Assurance.

There is nothing in this update that encourages me to buy back in here.