Kalibrate Technology has now released its final results for the year ended 2016.

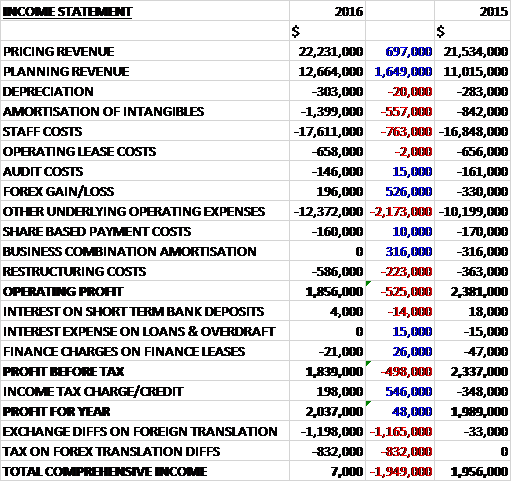

Revenues increased during the year with a $1.6M growth in planning revenue and a $697K increase in pricing revenue. Amortisation charges grew by $557K and staff costs were up $763K but there was a $526K swing to a forex gain. Other underlying operating expenses increased by $2.2m and there was a $223K growth in restructuring costs but there was no amortisation of acquired intangibles which accounted for $316K last year which meant that the operating profit was down $525K. Finance charges saw a modest decline but there was a $546K positive swing to an income tax credit due to tax losses being recognised which gave a profit for the year of $2M, a growth of just $48K year on year.

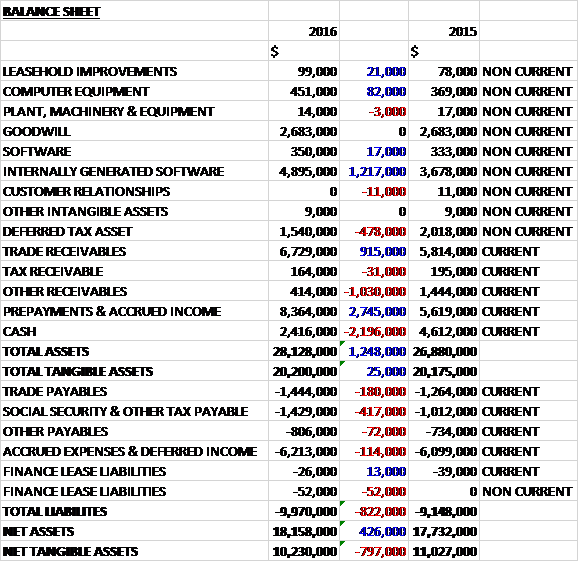

When compared to the end point of last year, total assets increased by $1.2M driven by a $2.7M growth in prepayments and accrued income, a $1.2M increase in software assets and a $915K growth in trade receivables, partially offset by a $1M decline in other receivables and a $478K fall in deferred tax assets. Total liabilities also increased during the year due to a $417K growth in social security and other taxes payable and a $180K increase in trade payables. The end result was a net tangible asset level of $10.2M, a decline of $797K year on year.

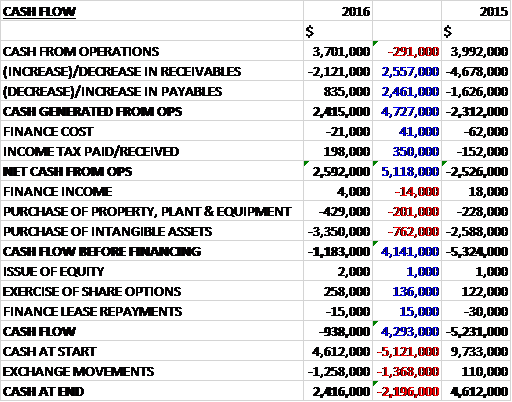

Before movements in working capital, cash profits declined by $291K to $3.7M. There was a cash outflow from working capital due to a growth in receivables but this was lower than last year and after a $350K positive swing to tax receipts, the net cash from operations came in at $2.6M, an improvement of $5.1M year on year. The group spent $3.4M on intangible assets and $429K on property, plant and equipment so that before financing there was a cash outflow of $1.2M. The group made $258K from the exercise of share options so the cash outflow for the year was $938K to give a cash level of $2.4M at the year-end.

The operating profit in the Pricing business was $727K, a decline of $1M year on year. During the year the group’s largest deals have come in the form of a perpetual license sales that have a recurring stream of associated software maintenance revenue. The core pricing platform was up 8% but a legacy service offering that provides significant recurring revenue at a low margin declined by about 22% in revenue terms.

In Q4 the group signed a $1.9M perpetual license contract with a US-based national fuel and convenience chain and a $1.6M perpetual licence deal with an independent refiner and B2B fuel retailer. They also continue to win new SaaS contracts, including a large multi-country European fuel retailer. There is ongoing progress in emerging markets with the first contract win in Chile with a multi-country South American fuel retailer and there is continued success in Mexico with one pricing and two planning contract wins following the entry into this market place in 2015. A first pricing perpetual license deal has been signed in China.

The operating profit in the Planning business was $1.9M, a growth of $389K when compared to last year. This has been largely driven by an increase in revenue following the consolidation of fuel and convenience retailers in the group’s core markets of Europe and North America. They have also signed several multi-year planning projects in Europe in this past year which provides a solid stream of recurring revenue.

A saleable bi-product of the planning business is the vast amount of traffic counts, demographic, retail volume statistical data that is collected as the group complete market study models for their clients. This data is then packaged into separate analytical offerings that clients purchase on a recurring basis although a relatively small segment it is growing.

In North America, pricing revenue was up 9% attributable to several significant perpetual license deals with four premier retailers and planning revenue increased by 9.7% mostly as a result of cross-selling planning products to existing pricing customers and due to the consolidation that continues throughout the region.

In Europe revenue was relatively flat year on year. This was mainly due to a large deal originally designed as perpetual that came in as SaaS, although this decrease was partially offset by the implementation of two large planning deals. The significant acquisition activity in the market has been driving considerable interest in the group’s planning segment. In Q2 2017 they will start another multi-year planning engagement with one of their pricing customers for a new significant cross-sell opportunity.

The most notable occurrence in the ROW market was the quick deregulation in Mexico. As the market deregulated, there was an immediate response from the retailers to accelerate their level of preparedness to meet the changing market requirements. The other significant deregulation revolves around the more measured approach demonstrated by the retailers in India. During the year the group re-entered and transacted business in China for a retail pricing contract. While it was a relatively small deal for them, it marked a in the way Chinese retailers view petroleum retail competition.

During the year the group sold ten clients under a SaaS contract for total booking of about $2M while four significant contracts were signed in North America as perpetual licenses. Even under a perpetual license arrangement, the group increased its recurring revenue as all licenses have a multi-year maintenance contract. They increased their annualised recurring revenue by $2M to $23M.

During the year the group introduced a new in-store merchandise pricing and promotion offering. This offering should assist convenience retailers in gaining more visibility into their merchandise categories within their stores. They have already experienced significant interest both from existing clients and new convenience store operators. They will therefore invest in this offering so as to ensure that they are able to capitalise on this anticipated demand.

Additionally, in the upcoming year the group will be modifying their existing wholesale pricing platform to accommodate global business to business pricing analytics for the oil and gas industry. They have witnessed clear global interest from existing clients and potentially new customers for this solution as evidenced by a deal signed in the second half of the year. These new offerings, in addition to the regular updates and enhancements to their cloud suite of products will provide the cornerstone of future global growth.

This coming year they will place particular emphasis on improving the global breadth of their business, focusing their attention on areas with higher growth potential. As such, they plan to increase investment from operating cash flow into the ROW, the merchandise pricing and promotion platform and they wholesale pricing solution.

Following the Brexit vote, sterling has lost a lot of value. They report in US dollars with about 15% of revenue and 27% of costs in sterling so they anticipate only a minimal impact going forward.

The restructuring costs relate to a plan where the group eliminated the long term cost associated with a group of employees in order to reallocate the capital resources towards the merchandise pricing offering and the global initiatives that include more global sales and support.

After the year-end the group formed an entity with its long-time agent in India to sell locally as they position the group for future growth in this recently deregulated market.

The board are confident in their ability to grow the group in accordance with expectations but increasingly their ability to do this requires them to secure significant wins from the emerging markets and countries with higher growth potential such as India, Asia and Africa. For the current financial year they are seeing encouraging signs that this will prove to be the case but often sales cycles in these markets tend to be more prolonged in terms of timing for closing deals.

At the current share price the shares are trading on a PE ratio of 12.5 but I can’t find any forecasts. There is no dividend on offer here. At the end of the year the group had a net cash position of $2.4M compared to $4.6M at the end of last year.

On the 24th January the group released a trading update covering the first half of the year. Revenue and EBITDA have been impacted by adverse forex movements coupled with delays to signing of certain new contract and the start of some backlog projects. A number of these are now expected to close and start in the second half of the year. As a result the board now expects revenue and EBITDA to be materially lower than market expectations at $14M and just $100K respectively.

Going into the second half contracted year to date revenue is $26M and the group enters the period with a strong pipeline. The range of outcomes for the full year will depend on the closing of further business, the timing of which is difficult to predict. The group are therefore reducing the cost base.

During the period the group saw encouraging sales in their core markets, particularly in their newer product offerings. In December they signed the first contract for their new merchandising pricing and promotion offering with Ricker’s, a fuel and convenience brand in Indianapolis. They are also making encouraging progress with their planned B2B/Wholesale pricing proposition which remains on track for launch in the summer of 2017.

The group also continue to push ahead with their strategy to invest in sales growth in their ROW region. Progress here has been slower than anticipated, however, with a larger portion of the delayed contracts located in these regions.

Overall then this has been a bit of a sluggish year for the group. Profits were up due to positive movements in deferred tax – pre-tax profits declined year on year. Similarly the operating cash increased but this was due to more favourable working capital movements and cash profits declined with no free cash being generated. The reduction in profit seems to have come from the pricing division but it is not clear as to why – perhaps the lower legacy sales have affected profits.

So far this year, things have been tough. The group has suffered with forex movements and delays in order and are not expecting to make much of a profit at all in the first half. They also don’t sound that confident about timings of orders in the second half and I can’t find any forecasts. All of this leads me to think that perhaps now is not the time to invest here.

On the 13th June the group announced a recommended cash offer to be bade by Hanover Active Equity Fund. Under the terms of the offer, Kalibrate shareholders will be entitled to receive 85.5p in cash per share, which is a premium of 50% over last night’s price and values the group at £29M. The directors intend to unanimously recommend that shareholders accept the offer and Hanover has received irrevocable undertakings representing about 40% of the issued share capital.