Keller has now released their interim results for the year ending 2017.

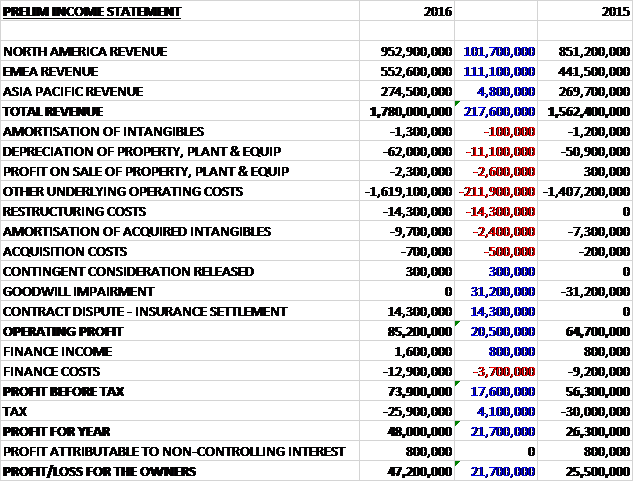

Revenues increased when compared to the first half of last year with an £84.7M growth in EMEA revenue, a £47M increase in Asia Pacific revenue and a £9.7M growth in North America revenue. There was a £1.7M improvement in profits on the sale of fixed assets but depreciation was up £3.3M and other underlying operating costs grew by £132.1M. There was also a £20.5M increase in earnings surrounding the contract dispute which meant that the operating profit grew by £29.5M. Finance income was up £1.3M with finance costs increasing by £600K and tax charges growing by £4.5M to give a profit for the period of £41M, a growth of £25.3M year on year. Although removing the contract dispute items, profit would have grown by £4.8M.

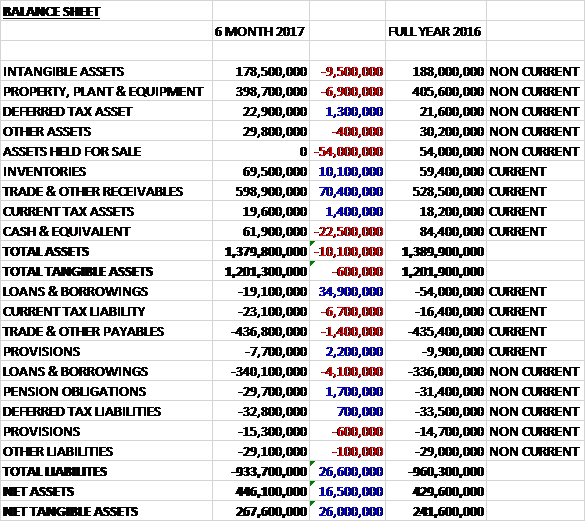

When compared to the end point of last year, total assets declined by £10.1M driven by a £54M elimination of the asset held for sale, a £22.5M fall in cash, a £9.5M decline in the value of intangible assets and a £6.9M fall in property, plant and equipment, partially offset by a £70.4M growth in receivables and a £10.1M increase in inventories. Total liabilities also declined during the period as a £6.7M growth in current tax liabilities was more than offset by a £30.8M decline in borrowings. The end result was a net tangible asset level of £267.6M, a growth of £26M year on year.

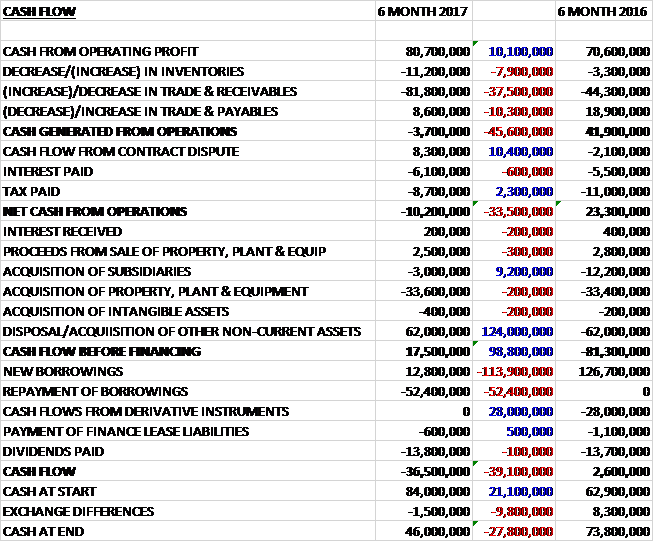

Before movements in working capital, cash profits increased by £10.1M to £80.7M. There was a big cash outflow from working capital, with an £81.8M increase in receivables. This meant that despite tax payments reducing by £2.3M and a £10.4M positive swing to a cash inflow from the contract dispute, there was a net cash outflow of £10.2M from operations, a detrimental movement of £33.5M year on year. The group received £2.5M from the sale of fixed assets and £62M from the warehouse sale at the centre of the contract dispute. They also spent £33.6M on property, plant and equipment along with £3M on acquisitions and £400K on intangibles to give a free cash flow of £17.5M. This covered the dividends of £13.8M but the group also repaid a net £39.6M of borrowings so there was a cash outflow of £36.5M in the half year and a cash level of £46M at the period-end.

The operating profit in the North American division was £28.6M, a decline of £5M year on year, which would have been even worse were it not for the £4.3M gain from favourable forex movements. The US construction market as a whole is solid but with regional and sectoral variations. Residential construction continues to grow strongly, infrastructure spending has slowed and commercial construction market rates vary by region. The profit fall was largely a result of a slowdown in construction activity in two major metropolitan areas where the group has a strong market position.

Hayward Baker had a solid first half with revenue and profit slightly ahead of last year. Case and HJ Foundation both recorded lower profit, however, as their core geographical markets saw a reduction in construction activity, particularly of high end residential apartments. The group’s largest job in the US, Bencor’s $135M diaphragm wall and grouting contract at a Dam in Pennsylvania is performing well. Suncoast had another good period, taking advantage of the ongoing increase in housing starts. Across the US bidding activity remains healthy and the US constant currency order book to be undertaken over the next year is up about 8% so the board expect revenue in H2 to be ahead of H2 last year.

The Canadian business continues to operate in a difficult market and made a small loss in the seasonally weak first half. The major $42M subway contract in Toronto, which finally mobilised in Q2 after more than a year of delays, has started well. In June the group announced further cost-cutting measures, including moving their admin centre from Edmonton to Toronto which better reflects where the bulk of the business opportunities now lie.

The operating profit in the EMEA division was £20M, an increase of £6.4M when compared to last year, helped in particular by the good execution of the $180M contract in the Caspian region which is due to be substantially finished by the end of the year. Whilst a number of markets remain challenging, the most significant European businesses all had a good first half. There has recently been a slowdown in the UK business, but the others in the region all begin the second half with strong order books and good prospects.

Elsewhere market conditions and performance is more mixed. Construction markets in the Middle East are patchy but the business has had a busy period in the region, starting work on major projects in Abu Dhabi and Egypt, and is will set for a strong second half. The political conditions in South Africa and Brazil are holding back construction activity in those markets. Whilst the major project near Durban is progressing well, activity generally in Sub-Saharan Africa is at a low ebb. The Brazilian business made a small loss in the period.

The division has had a number of good project wins in the period. The constant currency order book of work to be undertaken over the next year is over 30% ahead of 2016, giving the board confidence of a good second half. The completion of the major Caspian project at the end of 2017 means that the division’s 2018 profit will be materially down on what is expected this year, however.

The operating loss in the Asia Pacific division was £3.8M, an improvement of £5.8M when compared to the first half of 2016 despite a £1.6M cost relating to unfavourable forex movements and very difficult markets in Australia and Singapore. The loss was mainly related to two significant loss making projects, a joint venture in Australia and a legacy piling job in Singapore. In Australia the revenue run rate increased in the first half, in a large part due to higher market activity. Whilst this pick up is yet to feed through into higher pricing, the Australian business broke even, an improvement of £5M.

In Asia, revenue was broadly flat with a significant increase in India being offset by a reduction in Singapore as a result of the major downsizing of Resource Piling over the last year. As a whole the Asian business recorded a loss as a result of piling contracts in Singapore won in 2016. The Singapore and Malaysian Heavy Foundation businesses have now been merged with tendering being managed out of Malaysia.

Q2 saw some good contract wins in India, including a £14M dam grouting project in Polavarum and an £11M stone column contract to improve the ground for the new Navi Mumbai airport. Looking forward, the division’s order book for the next year is about 30% up which should result in a continuing improvement in performance.

During the period the group made a profit on the contract dispute. The income represents the gain on disposal of the freehold of the processing and warehouse facility acquired last year along with rental income. The gain was £8M on a consideration of £62M, the same amount that it was acquired for. During the period the group reached an agreement to receive £11.7M of insurance proceeds, of which £8.8M has already been received. The group has now recovered £35.3M of the original £54M but not further recoveries are expected. The net cash cost to date of this dispute is £14.3M.

In March the group acquired GEO Instruments, an instrumentation and monitoring business based in North America, for a cash consideration of £2.5M. This generated no goodwill.

Going forward, the US construction market and most of the major European markets are robust whilst elsewhere a number of markets remain difficult. Contract awards have been strong during the period with a 20% increase year on year. As a result, the board expect full year results to be in line with their expectations.

At the period-end the group had a net debt position of £297.3M compared to £339.7M at the same point of last year. At the current share price the shares are trading on a PE ratio of 11.3 which falls to 9.8 on the full year consensus forecast. After a 5% increase in the interim dividend, the shares are yielding 3.4% which increases to 3.5% on the full year forecast.

Overall then this has been a decent period. Profits increased, net assets were up and although there was an operating cash outflow, cash profits increased as this was due to a big increase in receivables. The EMEA region is performing well, but this mainly seems to be due to one large contract in the Caspian region and I am a bit concerned about what happens next year when it has been completed. Asia Pacific is still loss making but this has Improved due to the business breaking even in Australia. North America saw a slow-down in certain markets which has affected profits.

There are a few potential concerns here, as noted above, but the forward order book looks good and the forward PE of 9.8 and yield of 3.5% seems to account for the concerns to some extent. I remain a holder.

On the 16th November the group released a trading update covering the first four months of H2. Both revenue and profit are ahead of the same period of last year. Tendering activity and contract awards remain healthy and the order book for work to be undertaken over the next year is around 10% higher. Overall they remain on course to meet board expectations for the full year and there have been no major changes in their markets since the interim results stage.

In North America, the US construction market as a whole remains solid but with continuing regional and sectoral variation. The two large hurricanes resulted in lost production on some sites in Florida and Texas for up to two weeks in Q3 which has led to a negative one-off profit impact of £3M. Operating profit in North America will decline this year as a result of the previously noted weakness in specific regional markets, as well as the one-off effect of the hurricanes. Looking ahead, bidding activity remains healthy and the order book is around 10% above the level at the same time last year. The group is expected to benefit from the proposed US corporate tax changes, if enacted, as well as in the medium term from any uplift in infrastructure spending in both the US and Canada.

In EMEA the group are still seeing strong revenue and profit growth, helped by continued excellent execution of the $180M contract in the Caspian region which remains on track to be completed by the end of 2017. As a result, profit for the division in 2018 will be materially below this year’s result.

In Asia Pacific, pricing remains challenging in certain market segments but the division continues to make progress in reducing its losses as the results of restructuring and a higher workload materialise. The business in India is growing strongly and in Australia they are seeing an upturn in investment from the resources industry. They continue to expect that the region will return to profitability in 2018.

Overall, pretty decent but I am a bit concerned about the reliance on the Caspian contract so may look to sell up if possible.

On the 5th January the group announced that they expect new US tax reform legislation will benefit their future after tax earnings. This is mainly due to the future reduction in US corporate income tax from 35% to 21%, partly offset by a net adverse impact from other changes. Their current estimate is that the changes will reduce the group’s future overall effective percentage tax rate by around 5% to a number in the high twenties.

In addition, they expect that the group’s 2017 earnings will benefit from a one-off non-cash credit to the income statement as a result of the revaluation of US deferred tax liabilities, which is expected to be around $10M.

They also announced that they are in discussions to acquire Moretrench, a geotechnical contracting company operating predominantly along the east coast of the US. Last year the business had an operating profit of $9.3M and it is envisaged that the acquisition will be funded wholly in cash using existing borrowing facilities.

The enlarged entity will be the largest geotechnical solutions provider on the east coast and will give the group access to new niche geotechnical products as well as new industrial customers and should have good revenue and cost synergies. The two businesses have partnered on a number of successful joint venture projects in the past.