Laura Ashley has now released its second set of interim results or the year ending 2016. This encompasses the results for the past year or so.

Revenues declined when compared to last year as a £2.6M growth in e-commerce and mail revenue, and a £600K increase in hotel revenue was more than offset by an £8.4M fall in store revenue and an £8.9M decrease in non-retail revenue. Cost of sales also declined but gross profit was still some £4.3M below than of 2015. Amortisation and depreciation both increased modestly but other operating expenses fell to give an operating profit £1M below that of last year. The loss from the associate increased by £800K and finance costs were up £400K along with exceptional items which showed a £1.9M detrimental swing to a £1.3M expense which related to the license partner in Australia being placed into voluntary administration. After the tax charge fell by £1.1M the profit for the year came in at £15.3M, a decline of £3M year on year.

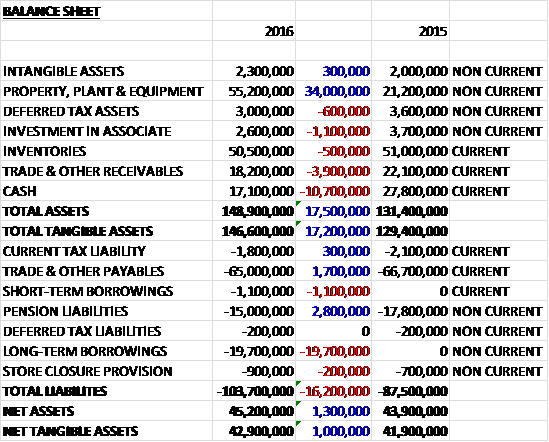

When compared to the end point of last year, total assets increased by £17.5M driven by a £34M growth in property, plant and equipment partially offset by a £10.7M decline in cash, a £3.9M fall in receivables and a £1.1M decrease in the investment in an associate. Total liabilities also increased during the year as a £20.8M growth in borrowings was partially offset by a £2.8M decline in pension liabilities and a £1.7M fall in payables. The end result was a net tangible asset level of £42.9M, a growth of £1M year on year.

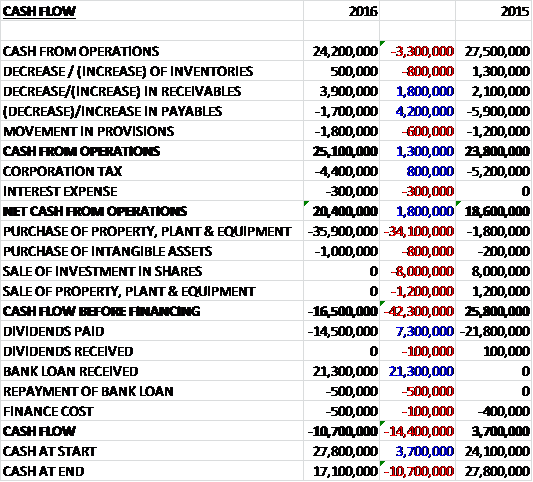

Before movements in working capital, cash profits declined by £3.3M to £24.2M. There was a modest cash inflow from working capital compared to an outflow last year so that after tax payments fell by £800K and interest costs increased by £300K, the net cash from operations came in at £20.4M, a growth of £1.8M year on year. This did not cover the £35.9M spent on property, plant and equipment along with the £1M spent in intangible assets so before financing, there was a cash outflow of £16.5M. Despite this, the group still spent £14.5M on dividends so after a net £20.3M of new borrowings, there was a cash outflow of £10.7M and a cash level of £17.1M at the period-end.

The contribution from the retail stores was £19.7M, broadly flat year on year with an increase of just £100K. There are currently 193 stores in the UK compared to 205 at the same point of last year as during the year, three new stores were opened and fifteen were closed, reducing total selling space by 3.8%. Total UK sales decreased by 2% due to the reduction in store numbers and one week less of reported trade. The UK retail business performed in line with the overall retail market but ahead in some product categories.

Furniture sales increased by 2.8% over the same period last year with like for like sales up 4.8%. The depth of choice within this category has enabled this growth with 24 wooden furniture ranges, six of which are new and various other new products. Further product development has been added to the range for this year. Home accessories sales for the period increased by 5.6% with like for like sales up 8.7%. This category continues to grow on the back of innovative product development, range additions, and in particular, seasonal offerings and the group outperformed the market in this category.

Decorating sales fell by 1.1% with like for like sales up 1.3%. The best performing products in this category were the made to measure and readymade curtains as well as the extensive paint collections. Fashion sales decreased by 4% over the same period last year, with like for like sales up 2.6%. The group are pleased to have maintained like for like growth in what has been their most challenging product category. They plan to broaden exposure of their fashion ranges as they forge new partnerships with other retailers.

The contribution from the e-commerce and mail order division was £11.9M, a growth of £2.3M when compared to 2015 and the division now represents 19.5% of total UK retail sales. The loss from the hotel business was £300K, an improvement of £100K year on year and continued to improve steady with a strong growth in sales.

The contribution from the franchising, manufacturing and licensing business was £10M, a decline of £3.4M when compared to last year. At the period-end, there were 270 franchised stores in 29 different territories worldwide compared to 303 at the same point of last year. The primary reason for the shortfall in performance compared to last year was the Japanese market were a rise in local sales tax, a weak Yen and a subdued domestic economy meant that demand was weak and the slow down continued through the year. Also, political instability and economic difficulties in other territories have contributed to a weak performance. Work continues on establishing the brand in new territories, however, and the board believe that the acquisition of the Asian head office in Singapore will help lead the brand expansion into the Asian territories. The share of loss from the associate was £1.3M, an increase of £800K year on year.

In August the group purchased a commercial property in Singapore at a total cost of £36.2M. The acquisition has been partly funded by a SG$42.9M debt facility provided by DBS Bank (currently translated at £20.8M. The loan is repayable on a monthly basis for a term of fifteen years with a prevailing interest of LIBOR plus 2% per annum. The remaining consideration of £14.9M was funded from the group’s cash reserves.

So far this year, trading in the first seven weeks of the period is down 0.4% on a like for like basis. At the current share price, the shares trade on a PE of 12 which falls to 11.1 on the full year consensus forecast. After the interim dividend remained the same this year, the shares are yielding a hefty 7.9% but I can’t find a forecast for the dividend going forward.

Overall then, this has been a bit of a mixed year for the group. Profits were down but net assets increased, as did the operating cash flow, although this was due to a comparatively favourable movement in working capital and cash profits declined. The group is very cash generative and if they did not purchase the office building in Singapore, the dividends would have been just about covered although the office building meant there was a cash outflow for the year.

The performance in the UK has been fairly good – the stores have been flat but e-commerce has increased profits. Within the individual categories, furniture and home accessories have done particularly well with decorating and fashion struggling a bit more. The hotels are still loss making but the real issue is the performance of the overseas franchises with the Australian franchise now in administration and poor sales in Japan.

Going forward, the 0.4% LFL fall in trading does not fill me with confidence but perhaps a PE of 11.1 and dividend yield of 7.9% prices this in. A tricky one this – I am tempted to buy back in here for the covered yield.