Majestic Wines has now released its final results for the year ending 2015.

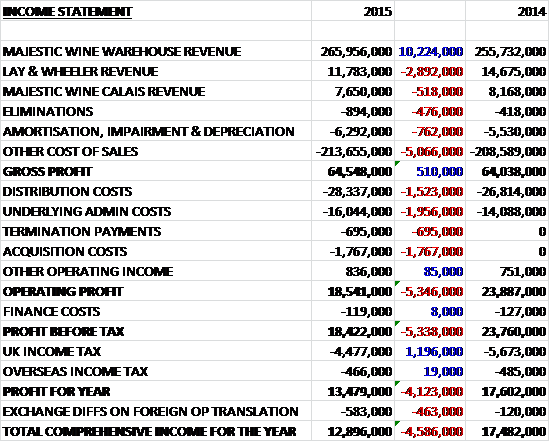

Overall revenues increased year on year as a £10.2M growth in Majestic Wine Warehouse revenue was only partially offset by falling revenues at Lay and Wheeler and Calais. We also see cost of sales increase year on year to give a gross profit some £510K higher than last year. We then see distribution costs increase by £1.5M and underlying admin costs increase by nearly £2M which was not helped by a £695K termination payment and £1.8M worth of acquisition costs. Finance costs were broadly flat but tax was £1.2M lower than last year to give a profit for the year of £13.5M, a decline of £4.1M when compared to 2014.

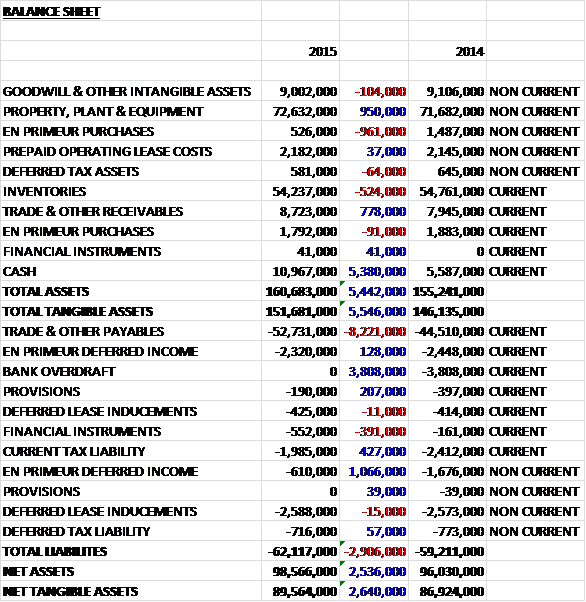

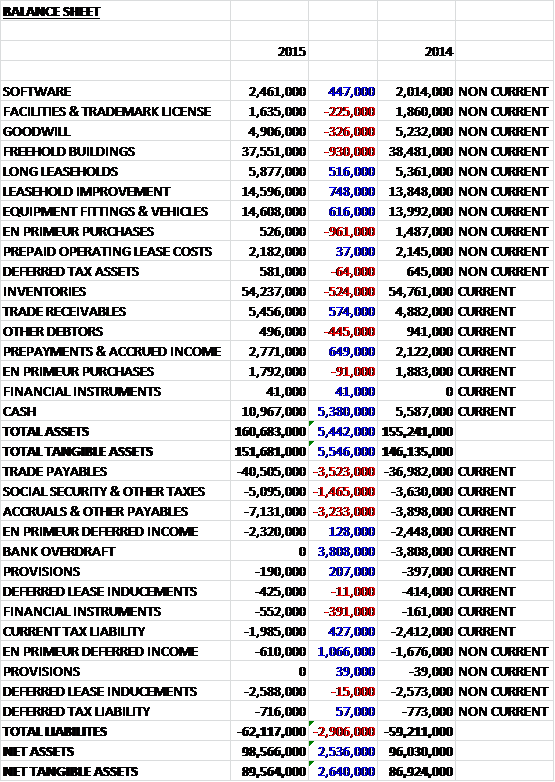

When compared to the end point of last year, total assets increased by £5.4M driven by a £5.4M growth in cash, a £950K increase in the value of property, plant & equipment, and a £778K increase in receivables partially offset by a £1.1M fall in en primeur purchasers and a £524K decline in inventories. Liabilities also increased during the year as an £8.2M grown in payables was partially offset by a £3.8M reduction in the bank overdraft and a £1.2M fall in en primeur deferred income. The end result is a £2.6M increase in net tangible assets to £89.6M which looks good until it is remembered that last year, operating lease liabilities were about £90M.

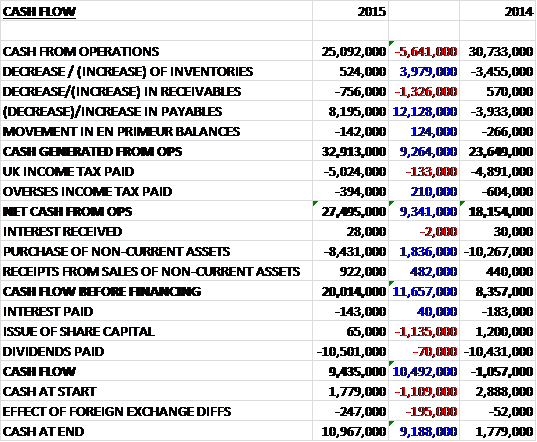

Before movements in working capital, cash profits fell by £5.6M to £25.1M. A large increase in payables, however, due to certain calendar year end payments worth around £4.4M falling into the 2016 financial year, meant that after tax, net cash from operations stood at £27.5M, a £9.3M increase year on year. The group then spent £8.4m on intangible assets to give a free cash flow of £20M, more than enough to pay the £10.5M worth of dividends to give a cash flow for the year of £9.4M. Even when the £8.2M worth of increased payables is taken into account, this is not a bad result.

The operating profit at the Majestic Wine warehouses was £19M, a decline of £2.4M year on year. Despite this decline, the commercial business which sells to restaurants, hotels and pubs, saw a strong growth in sales, up nearly 13% to £42.1M. Sales in e-commerce also showed a return to strong growth, increasing by 12% year on year and now representing 12% of total UK retail sales. One area of focus has been on customer communications and in order to increase leverage of an upcoming programme, the number of customer email addresses being held increased by 46% to 394,000. Towards the end of the year the group launched their first app, “myMajestic”. This allows customers to store their purchase history both online and in store. It has so far been downloaded by 19,000 customers and initial feedback has been good. They intend to continue to invest in enhancing the functionality of the app with development based on feedback from customers.

The operating loss at Lay & Wheeler was £67K, a negative swing of £1M when compared to last year. This loss was recorded after recognising a reduction of £500K in the balance sheet carrying value of stocks of fine wine for which market values have fallen below acquisition costs, primarily in the Bordeaux 2010 vintage. During the year the Bordeaux 2013 campaign was very disappointing and despite the quality of the vintage being good, sales were down across the industry. The group has increased the frequency of offers and had some successes such as the launch of Penfolds Grande 2010, though. They have now rebranded the business as Cellar Circle with enhanced membership benefits and customer sign up rates have improved.

The operating profit at Majestic Wine Calais was £1.4M, broadly flat year on year. During the Autumn of 2014 the group simplified their pricing structure highlighting to customers where they can make substantial savings on the UK market price. Customers have been encouraged to order through the click and collect proposition which now accounts for over 44% of sales, up from 41% last year.

Despite the rather disappointing result with growth in online and commercial sales not enough to offset the underlying sales decline in the more mature Majestic stores, the group continued to grow market share, increasing by 0.1% to 4.3% with UK like for like sales growing by just under 2%. They have also seen an increase in the number of active customers of 35,000 with an average spend per transaction remaining at £129. The group have opened in ten locations during the year and closed three bringing the total number of stores to 212. They now believe that the optimum number of stores is between 225 and 250 as opposed to 330 previously indicated. The group has implemented a new CRM strategy following the appointment of a new marketing agency and they aim to build a more engaging, personal and relevant relationship with their customers. The first stage of this strategy was implemented by enhancing and segmenting the database to enable better targeted multichannel communications with a new customer welcome programme being launched in November.

The transformative news that occurred after the end of the balance sheet date was the acquisition of Naked Wines for a total consideration of £70M which includes £50M payable in cash on completion and up to £20M in contingent consideration. Naked Wines is a customer funded international online wine business with over 300,000 customers. In an unusual move, former CEO of Naked Wines Rowan Gormley has been appointed CEO of Majestic. The acquisition will significantly accelerate the planned development of the group’s online capabilities whilst providing Naked Wines with the infrastructure to enable a click and collect delivery option. Additionally, it opens up attractive markets in the US and Australia. There is no doubt that Naked Wines is a great and exciting acquisition for the group but it does seem very expensive to me. Following the acquisition the group entered into a facility with Barclays and HSBC for £85M with some £50M drawn down so far.

As well as a new CEO, Anita Balchandani has joined the board as non-executive director. She is a partner and sector head of the UK Retail Practice at OC&C Strategy Consultants, an international consulting firm. She has experience of working with clients to make the transition towards successful multichannel operating models and unlocking insight and value from customer data so I can see where the board are coming from with this appointment.

Following Rowan’s arrival he is conducting a thorough strategic review of the business and a number of new initiatives have been designed to restore the group to profitable growth, such as one off trial and learn initiatives and the creation of in-house expertise in key areas. In all, the initial priorities are to make the shopping experience simpler, easier and more fun; invest in staff training and retention; build sustainable sales growth through more personalised service and recognising loyalty; rebuilding the supply chain to optimise on shelf availability; deliver robust IT to support ongoing innovation; and to limit new store openings to the 20 to 30 locations that can deliver a good return on investment. Initial costs of this are expected to be £3M in 2016 with most of the costs falling in the first half of the year, which will clearly constrain profit in the short term.

Trading in the first two months of the new year has been in line with management expectations and despite the near-term headwinds, the CEO is confident of delivering significant shareholder value in the medium term (although he would say that of course)

At the current share price the shares trade on a P/E of 20.7 which reduces to 17.6 when we take out the non-recurring costs – either way this looks a little pricey and even on next year’s consensus 15.5 the market seems to be valuing some considerable growth. After the final dividend was cancelled, the yield for the year as a whole stood at a measly 1% which is expected to grow to 3.9% next year. That seems a little optimistic to me given the board have already signalled their intent to not have an interim pay out next year with future dividends “progressively” re-instated by 2018. At the end of the year, the group enjoyed net cash of £11M compared to £1.8M this time last year, although the acquisition of course changes that.

Overall then, the results were fairly lacklustre with a fall in profits but an increase in net assets. Operational cash flow did increase but this was only because some payments were shunted into next year and underlying operational cash flow fell year on year. The group still generates a decent level of free cash flow, however. Operationally the online and commercial businesses are both doing well but the store portfolio is faring less well and the Lay and Wheeler business really seems to be struggling due to a lack of demand for the recent Bordeaux vintages. The acquisition of course was the most important part of this update and Naked Wines looks to be an exciting company, although as I have said the price paid certainly seems to be on the high side. There is headroom of £35M which will certainly cover day-to-day trading but the likely £20M of contingent consideration will have to come from somewhere. In conclusion, there are enough short term headwinds to make me think that the valuation here has got a bit ahead of itself so I will not be rushing in to buy just yet.

The shares have been boosted by the acquisition announcement and seem to be undergoing some consolidation now.

Majestic Wine has now released its annual report.

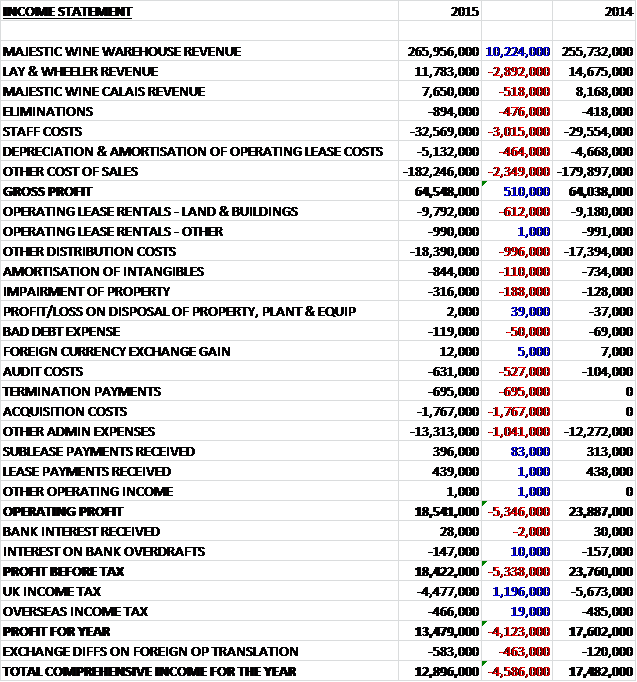

We can see some more information about those costs with depreciation and amortisation of operating lease costs up £464K, staff costs increasing by £3M and operating lease rentals themselves increasing by £612K. There was also a £188K, representing more than double last year, increase in the impairment of property and the group paid much more to their auditors than in last year for corporate finance services.

Within intangible assets there was an increase in software valuation, more than offset by falls in the value of licenses and goodwill. Within tangible fixed assets, we see increases in long leaseholds, leasehold improvements and equipment, partially offset by a £930K fall in the value of freehold buildings. Within receivables, a £445K fall in “other debtors” was more than offset by a £574K increase in trade receivables and a £649K growth in prepayments and accrued income. Within payables, we see a £3.5M increase in trade payables, a £3.2M growth in accruals and other payables and a £1.5M increase in tax payable so all types of payable are on the up.

There was a bit of a mixed bag with regards the KPIs. Total revenue increased along with like for like UK store sales, which increased by 1.9%. The number of trading stores in the UK increased by seven and the number of active customers increased by 35,000. The average transaction value remained flat, however, and the profit before tax fell year on year.

We also see a net £84.3M of operating leases not on the balance sheet so these would have the effect of bumping net debt up to £73.3M, which is still an improvement on last year.

On the 21st September it was announced that Chairman Phil Wrigley purchased 10,000 shares at a value of £38K. This doubles his shareholding top 20,000 shares. Also, non-executive Ian Harding acquired 2,000 shares at a value of £7.6K to give him an interest in 10,000 shares.

On the 1st October it was announced that Greg Hodder had been appointed as a non-executive director. He is currently CEO of Charles Tyrwhitt Shirts Ltd but probably of more relevance he was previously CEO of Direct Wines for 14 years.