Mission Marketing is predominantly a UK based communications agency group. Their board is comprised of the entrepreneurs who run the agencies which is something I have never seen before. They earn project income which is recognised by apportioning the fees billed or billable to the time period for which those fees were earned by relationship to the percentage of completeness of the project to which they relate, which sounds sensible to me. Where recorded turnover exceeds amounts invoiced to clients, the excess is classified as accrued income within receivables and where amounts invoiced to clients exceed recorded turnover, the excess is classified deferred income within accruals. With the exception of the recent acquisition in Asia, the group almost entirely earns its profits in the UK. It has now released its final results for the year ended 2014.

The group has a number of self-contained agencies including April Six, the UK’s leading technology channel marketing agency working with brands on an international basis; Big Dog, a full-service integrated agency creating ideas from insight across all channels with a focus on brand payback; Bray Leino, working with clients through every channel and across the business spectrum and is apparently the number one B2B agency in the country; Proof, a specialist PR agency helping science, engineering and technology organisations communicate complex subjects; RLA, specialising in automotive and also offering the capability of a full-service agency;

Robson Brown, one of the North of England’s major advertising brands; Solaris, a specialist full service medical communications agency for UK, European and Global clients; Speed, a commercially driven PR agency specialising in business and brand transformation with expertise in sport, technology, media, health and wellbeing, food and drink, financial and business services; Splash, based in Singapore with offices in Shanghai, Hong Kong, Malaysia and Vietnam, a digital agency aiding multinational brands build websites and market their products across all digital channels; Story, an award-winning integrated agency working with consumer brands and services from its Edinburg base; and Thinkbdw, the leading property integrated marketing agency in the UK, working with developers across all aspects of their sale support programmes from advertising to show homes.

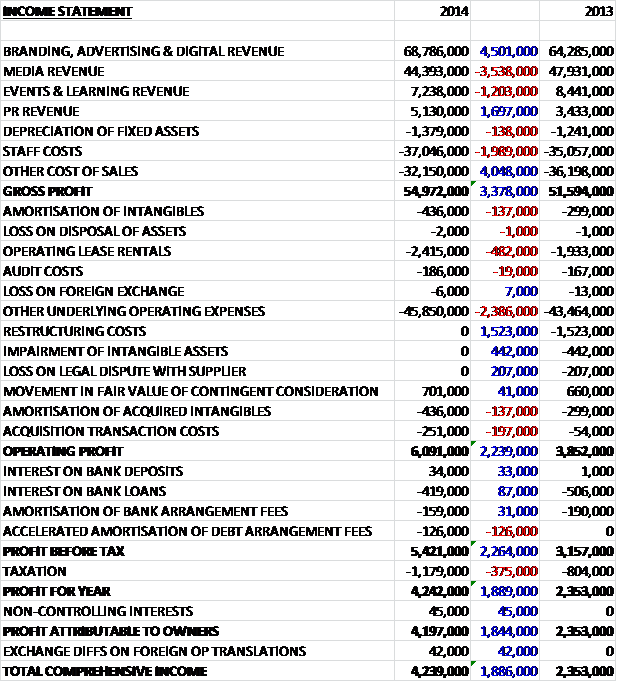

Overall revenues increased year on year as a £4.5M increase in branding, advertising and digital revenue and a £1.7M growth in PR revenue was partially offset by a £3.5M fall in media revenue and a £1.2M decline in events and learning revenue. Staff costs increased when compared to last year but other cost of sales declined to give a gross profit some £3.4M ahead. We then see a £482K increase in operating lease rentals and a £2.4M growth in other underlying admin expenses but various one-off costs fell year on year with no restructuring costs, impairments on intangible assets or legal disputes so that the operating profit increased by £2.2M year on year. We then see declines in interest from loans counteracted by the acceleration of the amortisation of debt arrangement fees and a tax bill some £375K higher to give a profit for the year of £4.2M, an increase of £1.8M when compared to 2013.

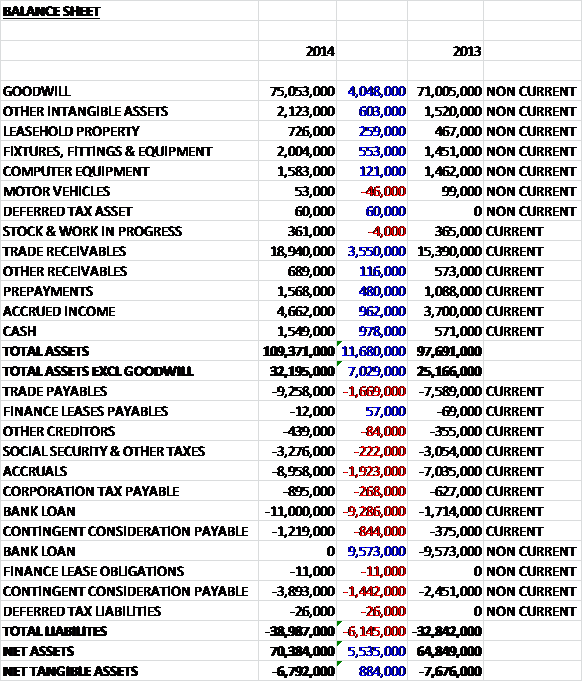

When compared to the end of last year, total assets increased by £11.7M driven by a £4M increase in goodwill and a £3.6M growth in trade receivables with accrued income and cash also increasing year on year. Liabilities also increased due to a £1.9M increase in accruals, a £1.7M growth in trade payables and a £2.3M increase in contingent consideration payable to give a £884K improvement assets excluding goodwill, although they remained a negative £6.8M.

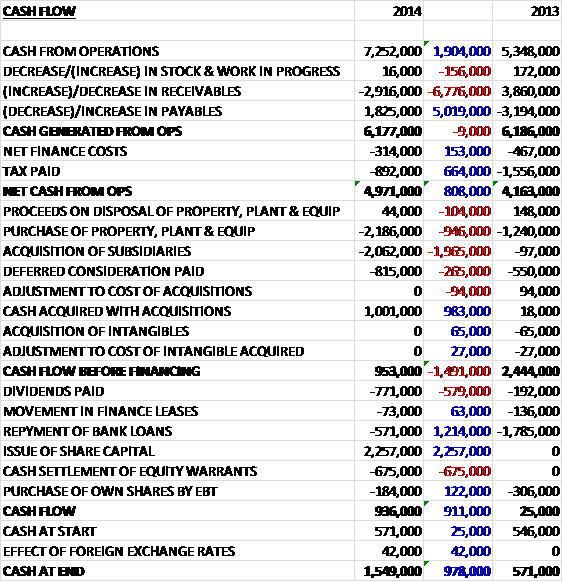

Before movements in working capital, cash profits increased by £1.9M to £7.3M. We then see an increase in payables more than offset by an increase in receivables so that cash from operations was flat year on year at £6.2M. When we take account of lower finance costs and tax, however, the net cash from operations is £808K higher than last year at £5M. The group used this cash to pay for capital expenditure (£2.2M), which was higher than previously due to the relocation of two agencies, and deferred consideration (£815K) and even managed to spend a net £1.1M on new acquisitions and still have a free cash flow of £953K. This was enough to cover the dividends but the group also used cash from the issue of share capital to pay off some debt, including the equity warrants to give a cash flow for the year of £936K and a cash level of £1.5M at the year-end.

Operating profit at the branding, advertising and digital business was £6M, a growth of £300K year on year. Operating profit at the Media business was £949K, a decline of £198K when compared to 2013. Operating profit at the events and learning business was just £89K, flat when compared to last year. Operating profit at the PR business was £632K, a hike of £522K year on year. Within the overall increase in profits, some 5% was delivered through an increase in like for like profit.

Having traditionally focussed on the UK, the group has been expanding its international reach in recent years. The technology agency April Six has opened an office in San Francisco to service their existing and potential clients based there and now they are in Asia with Brey Leino having already opened an office in Singapore and the acquisition of Splash which brought with it offices in Singapore, Shanghai, Hong Kong, Malaysia and Vietnam.

The board structure is really interesting at Mission, the executive board is made up almost entirely from the founders of some of the individual agencies under the Mission umbrella, with the exception of the Finance Director who joined from UK Mail and one non-executive who also heads up Pittards and Pure Wafer. As such, the chairman’s statement is much less formal than I am used to including words like lallygaggers and using cricketing puns – I quite like that! I am not so keen on the lack of information about how each of the agencies are actually doing. This is probably not helped by the lack of a CEO with the group instead opting for an executive chairman structure which I am not really a fan of either.

The shareholder structure is also quite interesting, many of the business founders on the board own considerable numbers of shares with many owning about 1% of the company. Executive chairman David Morgan, along with Robert Day both own about 7.3% of the company each with the other large shareholders being made up of institutional holders that I have not head of – Herald Investment Management, Objectif Investissement Microcaps and the Polar Capital Forager Fund.

The improved economic conditions seen during the year had a largely positive effect on the group and nearly all agencies reported growth in revenues but it was not always possible to maintain profit margins in the face of continued downward pressure on pricing. The boom in the property market perversely resulted in a marked reduction in the level of marketing spend by developers and estate agents as demand outstripped supply. As well as a decline in spend with the property clients, the group also saw a decline in media spend too. Of the 7% growth in operating income, 5% was achieved from the full year’s contribution from Solaris and the various acquisitions with like for like revenue increasing by 2% year on year.

In addition to the myriad acquisitions, the group have also made some internal changes. They have created a sports marketing consultancy to advise clients in that area and have strengthened their technology offerings. More recently, agencies Big and Balloon Dog were combined under the Bigdog brand to create a single business. Overall, client retention has been strong which bodes well for 2015. The group achieved all of its KPI targets during the year which included increasing operating income, achieving operating margins at least in line with industry averages (11% achieved), year on year growth in profit before tax, a ratio of net bank debt to EBITDA of less than 2 (it was 1.5) and a ratio of total debt to EBITDA of under 2.5 (it was 1.7).

During the year there were three main acquisitions. In August the group acquired Proof Communication, a specialist science, engineering and technology PR business to extend the services already being provided by April Six in the technology sector. The group spent £1.5M on the acquisition comprising initial cash of £923K, shares worth £59K and contingent consideration of £511K with a possible maximum of £1M dependent on Proof achieving a profit in 2015. I think I would rather the group provided for the whole possible consideration rather than just about half of it. The acquisition came with £334K of intangible assets and generated goodwill of £576K. Since the acquisition the business has contributed £121K in profit so this looks like a good value purchase to me.

In September the group acquired 70% of the issued share capital of Splash Interactive, a specialist digital agency operating through five territories in Asia in order to support the group’s existing Asia based clients. The group spent £2.6M on the 70% interest comprising initial cash of £443K and contingent consideration of £2.2M. In addition, there is an option to purchase the remaining 30% of the business from 2018 at an estimated future cost of £1M. The maximum contingent consideration is a whopping £6.9M depending on various profit targets to the end of 2017, of which £4.7M has not been provided for. The business came with intangible assets worth £694K and generated goodwill of £2.4M. Since the acquisition date the business has contributed £197K to operating profit so this is another nice purchase, perhaps at the upper end of the appropriate valuation.

At the end of October the group purchased Speed Communications Agency in order to bring greater scale to their existing PR capabilities. The total paid was £815K with £435K in initial cash, £240K in shares and £140K in contingent consideration, which refreshingly is the maximum amount of contingent consideration possible depending on the business achieving certain profit targets to the end of 2015. The acquisition came with £274K of intangible assets and generated goodwill of £601K. Since the date of the acquisition the business contributed an operating loss of £40K on turnover of £327K so some work looks like it needs to be done here. There were also some smaller acquisitions totalling £480K, £225K in cash and £255K in contingent consideration.

After the year-end the group signed new bank facilities replacing those in place at the end of last year which meant that the remaining unamortised bank debt arrangement fees of £126K were fully written off during the year – these fees have already been paid in cash anyway so I am not going to count them as exceptional (unlike the management here). The main risk facing the group is probably the possibility of adverse economic conditions leading to a reduction in client’s marketing budgets and the potential loss of a key client, although none represent more than 10% of group operating income.

As mentioned above, after the year-end the group refinanced its borrowing facilities into an £8M term loan and a revolving credit facility of up to £7M, both repayable by Feb 2019. The interest rate terms on the new loans are improvement on the old ones, being 2.25% as opposed to LIBOR + 2.75% previously. There is no significant exposure to foreign exchange differences but there is no hedging against interest rate rises. Also after the year-end the group acquired Weather Digital and Print Communications, a digital marketing agency based in Edinburgh. The consideration payable is up to £880K in cash and shares, of which a £255K cash payment has been made with a contingent consideration dependent on the business achieving profit targets in 2015. The net assets are estimated to be about £100K.

Going forward, it is expected that 2015 will be another busy year, consolidating the acquisitions made, streamlining some of the existing operations and planning further acquisitions. As usual the profits are expected to be second half weighted (this year profit margins were 8% in H1 and 14% in H2 which exactly matches the pattern seen in 2013). The group expects to see further growth in the coming year in both revenues and profit but in order to underpin this growth, the board has restructured certain activities with the consequence of an extra £600K of costs in Q1 2015.

At the current share price the shares trade on a PE ratio of 8.8 which falls to 8 on next year’s consensus forecast. After a 10% increase in the total dividend for the year, the shares enjoy a yield of 2.4%, increasing to 2.7% on next year’s prediction. Net debt at the year-end stood at £9.4M compared to £10.7M at the end of last year. There were also outstanding operating leases of £3.9M at the end of the year, an increase from the £1.9M at the end of last year.

Overall then, I am warming to this company more than I expected. Profits increased year on year as did operational cash flow. Indeed there was even some free cash left over after the acquisitions were paid for, although a lot of the consideration is deferred and the free cash didn’t cover the debt repayments and dividends. The balance sheet, in common with all marketing companies it seems is wafer thin and stuffed with goodwill. This year net assets improved slightly but remained negative once goodwill is taken out. The board structure is very interesting and what it lacks in corporate experience it should make up for in enthusiasm, with most of the board founders of their own agencies and holding a lot of shares.

It seems that all marketing companies rely on acquisitions for growth and that is certainly the case here – three in one year with another after the year-end. Most of these acquisitions do look decent but I am a little concerned with the contingent consideration being racked up, particularly as not all of the potential consideration has been accounted for. The debt levels look fairly substantial but manageable and there does not seem to be any particularly hefty operating leases outstanding, although they are increasing so something to watch maybe. Operationally the group did OK, although growth was not that amazing as apparently it was too easy to sell houses so estate agents and developers didn’t need to bother paying for marketing which took its toll. Despite this, the shares offer a forward dividend yield of 2.7% and trade on a PE ration of 8.8, falling to 8 which looks very cheap to me.

On the 1st July the group announced that they were launching Mongoose, a specialist sports and entertainment agency. Focused on brand-led marketing and sponsorship campaigns, the new agency will source, negotiate and manage customised sponsorship and events programmes for B2B and B2C clients. It will be led by Chris O’Donogue, previously MD at WSM Communications, and John Beddington, former tournament director of the Canadian Open Tennis Championships will become chairman. Based in London and Singapore, Mongoose will be working with an impressive line up of major national and international brands including the sponsor of the London Triathlon, AJ Bell; Chestertons Polo in the Park, the O2 sponsor, CEWE photobook and Thomson Reuters which is partner of the LTA.

This is something I like to see, the group is not just buying established agencies but is launching its own, hopefully it will be a success.

On the 22nd July the group released a statement covering trading in the first half of the year. Revenue and profit are expected to show double digit growth, benefiting from both organic growth and the acquisitions made in the second half of last year. The debt level fell from £9.4M at the year-end to £8.3M at the half year point and the leverage ratios remain comfortably within the limits set by the board. It has been a busy period and the recent focus has been on bedding the new businesses into the group. Going forward, they will seek to exploit the opportunities for further growth the new business bring and in addition will continue to explore opportunities to extend their range further in response to client demand. In all, the board remain confident of meeting market expectations for the full year.

Additionally it was announced that non-executive director Stephen Boyd was stepping down to focus on his other business interests. This is a bit of a shame as Stephen was one of only two board members externally sourced and I felt brought something different to the group. Hopefully he will be replaced with a similar candidate. Overall though, I like the sound of this update and the company as a whole actually. Clearly as soon as the economy takes a dive, the shares will too but for now I am looking to take my maiden position.

The share really haven’t done much over the year, it has been one of consolidation but this update could have been the catalyst to propel them a bit higher?