Johnson Service Group provides textile services to both businesses and the consumer. The two services are textile rental and laundry, along with retail dry cleaning. Textile rental is the supply and laundering of work wear garments, premium linen to the hotel, catering and corporate hospitality markets, linen to the volume hotel market and sale of ancillary items. Dry Cleaning is the provision of dry cleaning, laundry and ironing services, carpet cleaning, upholstery cleaning, wedding dress cleaning and suede and leather cleaning. They are listed on the AIM exchange and have now released their final results for the year ending 2014.

Within the textile rental business the group has a number of brands. Apparelmaster is the UK’s market leading work wear rental, protective wear and workplace hygiene services provider with some 40,000 UK based customers operating in a wide cross section of industries. Stalbridge provides a wide range of products to the premium hotel, catering and corporate hospitality markets, including chef’s wear, linen, towels and a range of table linen. The newly-acquired Bourne business provides linen to various hotels including city and town centre establishments, holiday village resorts and the budget hotel sector.

Within the dry cleaning division, there are two brands. Johnsons Cleaners is the UK’s number one dry cleaner with a network of branches nationwide and Jeeves is a premium dry cleaning service that holds the royal warrant.

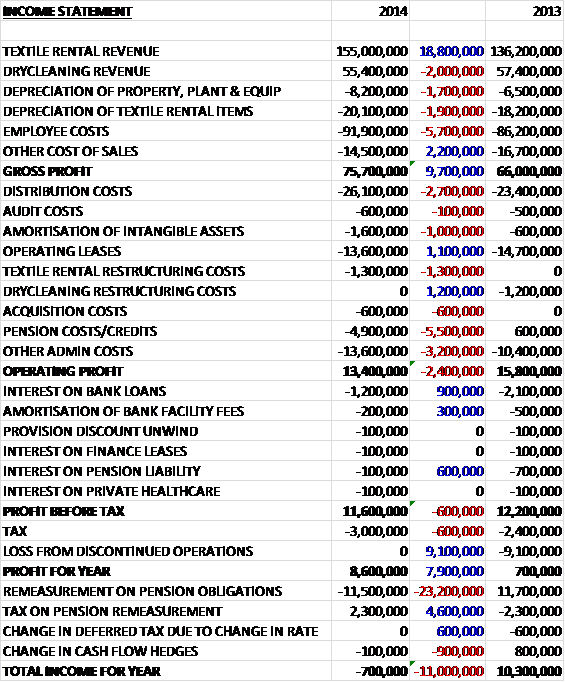

Overall revenues increased year on year as a £2M decline in dry cleaning revenue was more than offset by an £18.8M growth in textile rental revenue, benefiting from ten months of trading from Bourne. We then see a big increase in depreciation and a £5.7M growth in staff costs to give a gross profit some £9.7M ahead of last year. Distribution costs then increased by £2.7M and there was an increase in amortisation counteracted by a fall in operating lease payments. Other admin costs then increased by £3.2M and the textile rental restructuring costs that occurred this year were broadly the same as the dry cleaning restructuring costs that occurred last year but a £4.9M pension scheme cost pushed the operating profit down by £2.4M year on year. We then see a much smaller interest on bank loans and the pension liabilities to give a profit before tax just £600K ahead. After tax and the lack of the £9.1M loss from discontinued operations, the profit for the year stood at £8.6M, an increase of £7.9M when compared to 2013.

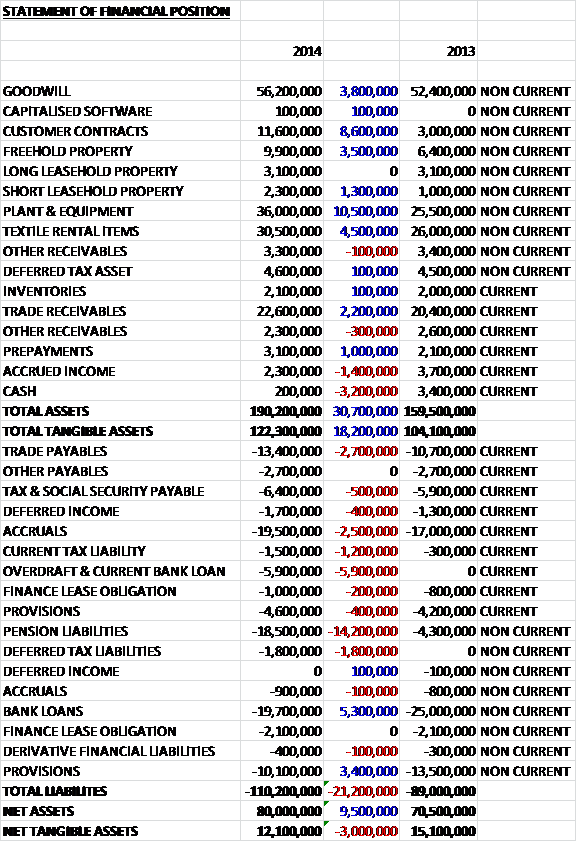

When compared to the end point of last year, total assets increased by £30.7M to £190.2M driven by a £10.5M increase in plant and equipment, an £8.6M addition to customer contracts, a £4.5M increase in textile rental items, a £3.8M addition to goodwill and a £3.5M growth in freehold property, partially offset by a £3.2M fall in cash levels. Liabilities also increased during the year as a £14.2M increase in pension liabilities, a £2.7M increase in trade payables and a £2.6M growth in accruals was partially offset by a £3M decline in provisions, mostly relating to property provisions. The end result is a £3M fall in net tangible asset to £12.1M.

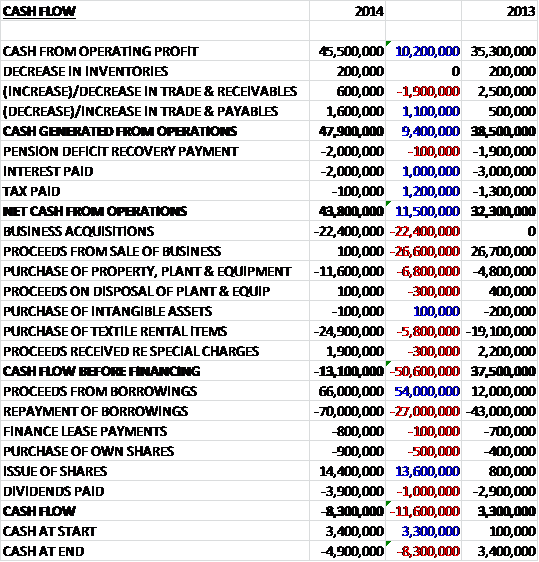

Before movements in working capital, cash profit increased by £10.2M to £45.5M which became £47.9M and £9.4M higher after modest working capital movements. The group then paid £2M in pension deficit recovery payments and the same amount in interest but tax was very low during the year to give a net cash from operations of £43.8M, an increase of £11.5M year on year. The group then spent £24.9M on textile rental items, £11.6M on property, plant and equipment and £22.4M on business acquisitions to give a cash outflow of £13.1M before financing. We then see £3.9M paid on dividends and a net £4M of loans paid back but clearly they were running out of cash at this point so more shares had to be issued which brought in £14.4M to give a cash outflow of £8.3M during the year and a negative £4.9M of cash at the year end. On this evidence, I don’t think the group could really afford that acquisition.

The operating profit at the textile rental division was £20.3M, an increase of £2M when compared to last year. Apparelmaster had a good year with higher levels of new business wins, increasing sales to existing customers and improving customer retention levels to in excess of 95% resulting in both operating profit and margin improving. A number of large national contracts renewed their agreements during the year resulting in additional spend on textile rental items with a corresponding increase in rental stock depreciation levels. The increased costs associated with this were offset by production efficiencies together with improved energy unit prices and consumption, however.

The business has continued to invest in equipment to drive higher productivity and lower energy consumption and as part of the investment strategy, a new £8.5M work wear processing facility in Leeds has been completed which replaces an existing facility and considerably increases garment processing capability. The business has also continued to invest in IT support which has improved the ability to communicate with customers in a simple manner.

Stalbridge had a strong performance as a result of new sales wins and an improvement in customer retention levels which were aided by productivity and efficiency benefits from the capital investment made in Q1 this year. A further investment of £1.2M in plant and machinery was approved for Q1 2015 which should increase capacity and reduce operating costs. The business continues to focus on the premium hotel, restaurant and catering industries and to improve the customer experience a new extranet and field based mobile technology solution has been developed and a new marketing campaign is planned for the new year.

Bourne traded very strongly throughout the ten months since acquisition, delivering increased volume from existing customers as a result of buoyant hotel occupancy levels and new hotel openings. The business has also made some new sales wins despite some competitive headwinds. It is expected that the business will continue to perform ahead of original expectations throughout 2015 in term of business development, adjusted operating profit and margin.

The operating profit at the dry cleaning division was £1.6M, an increase of £1.2M year on year. The group has attempted to develop their business model away from the high street towards alternative routes to market. During the year, the business developed a front of store presence in Waitrose and following successful trials, Johnson Cleaners had opened facilities in 78 Waitrose locations by the end of the year with the numbers increasing to 122 since the year-end. The business has also established collection and delivery points in a small number of corporate office premises with a high concentration of staff and as a preferred supplier with a number of facilities management companies who offer multiple services to their clients.

In addition to these initiatives, they have also made progress with their website development which now incorporates the capability of online transactions across various services which will enable home collection and delivery of bulky items in the near future. As mentioned elsewhere, the group are closing 109 branches by the end of H1 2015 with the expected net cost expected to be £6.5M with the bulk of that (excluding £1.8M) relating to already contractually committed cash spend in the current and future years such as rents, rates, insurance and dilapidations so I am a bit confused as to why there will be an extra charge for them as surely they are already provided for?

As can be seen there was a number of one-off costs during the year. The restructuring costs in the textile rental division includes part of the relocation costs following the construction of a new processing facility in Leeds to replace an existing textile rental plant and of the £1.3M charge, some £700K relates to the impairment of property plant and equipment. There is expected to be a further £1M charge relating to this in 2015. Acquisition costs of £600K related to professional fees of £400K and stamp duty of £100K following the acquisition of Bourne. The remainder of the cost relates to fees and expenses incurred during negotiations with undisclosed targets. The pension service cost of £4.7M was incurred after the closure of the defined benefit scheme to future accrual. In my view the restructuring and acquisition costs are just costs incurred in the day to day running of the business and I will include them in my calculations but that pension cost can probably be taken off to better ascertain the underlying performance of the group.

The pension scheme could be a potential risk to the group and it showed a deficit of £17.2M on assets of £198.3M this year compared to £3M last year due to a significant reduction in the discount rate applied to liabilities, and the group are expected to make £1.9M of deficit recovery payments next year after paying £2M this year. The group should be able to absorb these costs but there is still potential for further costs despite the closure to further accrual. As well as the pension, the group is also somewhat susceptible to interest rate hikes due to its large debt levels, although it does hedge some of this risk but the biggest risk is probably a slowdown in the UK economy as this would have a substantial effect on the group.

During the year the group acquired Bourne Services group for a cash consideration of £26.7M. The acquisition came with customer lists apparently worth £10.2M and it generated £3.8M in goodwill. Bourne’s operations are focused on the volume hotel linen market and serves customers in the Midlands, South Yorkshire, East Anglia, North London and the Home Counties. Since the start of March, Bourne has generated a profit of £2.4M and had the business been acquired at the start of the year, it would have generated £2.5M. Since the group comes with net intangible assets of £14M, including goodwill, the consideration does not look too stretched.

The dry cleaning business continues to operate in a difficult high street environment and despite several initiatives to reach new customers, like for like sales fell during the year. After a review, some 109 branches were identified, the majority of which have leases expiring within the next two years, where renewal of the leases will not be financially viable. A consultation exercise with affected employees is underway and it anticipated that the affected branches will close during the first half of 2015 which is expected to result in a charge of £6.5M during that year. In the medium term, this has got to be a good move from the company though.

The strong performance of the textile rental business has continued into 2015 and the board has identified areas for further growth and investment, particularly in sectors of the market where they are underrepresented. The streamlined branch network, together with a focus on highly convenient drop off and collection locations should help improve the performance of the dry cleaning business and the board expects that they will deliver a strong performance for 2015.

At the current share price, the shares trade on a PE of 19.1, falling to 15 on Investec’s forecast which seems rather rich to me. After a 41% increase in the total annual dividend, the shares currently yield 2%, increasing to 2.2% on next year’s forecast. At the end of the year the group was in a net debt position of £28.5M compared to £24.5M at the end of last year and there is £64.4M of outstanding operating lease payments off the balance sheet which is quite considerable.

Overall then this has been a decent year for the group with a number of “buts”. Profit was down year on year but this was only due to the one-off pension charge following the closure of the scheme to future accrual so underlying profit did improve during the year. Similarly net tangible assets fell year on year but once again the pension scheme was to blame for this and if we take out the large increase in the deficit then net assets would have improved. Operational cash flow improved year on year and the group managed to generate some £7.3M in free cash but then spent a load more on the acquisition, which I didn’t think the group could really afford – although it seems a quality purchase.

The textile rental business is doing well and despite the relatively low profitability in the dry cleaning that also improved during the year with the new non-high street initiatives looking good to me. I do think that operationally things are going well here, and there could be a bright future but my reservations are on the financing side of things. The pension scheme is becoming a problem and the £2M annual payments to reduce the deficit are being noticed. Similarly the debt levels seem a bit too high for my liking given the fact that the balance sheet is not looking amazing for a company that is actually quite asset-heavy.

On the 1st May the group announced the acquisition of London Linen Supply, a specialist supplier of table linen and chef’s wear to the restaurant, catering and hospitality market, based in London. The total consideration payable amounts to £69.4M in cash.

London Linen currently supplies some 900 customers at over 3,400 locations and processes about 1.6M pieces of linen a week. The directors believe that there is a 20% additional processing capacity available before any further investment. The company services customers predominantly in the London area but also covers major cities in the Midlands, the North and the West. The profit before tax for the acquired business is £5.5M for the year ended 2014 and the board expects it to be immediately earnings enhancing immediately and significantly earnings enhancing from 2016 onwards.

In order to fund the acquisition the group has opened a new banking facility which is a £100M revolving credit facility which runs to April 2020. In addition there is a year-long short term facility for £20M. The group is also undertaking a placing of just over 30M shares in order to raise £21.1M. The new shares will represent about 10% of the company’s existing share capital and will be priced at 73p per share.

It does seem as though London Linen is a quality outfit but I am getting more concerned about the levels of debt seen here. Following the acquisition the group has a net debt position of £73.7M and the chairman has stated that the group are continuing to look for further acquisitions. I am a bit risk averse by nature and feel that they may be over extending themselves here. In addition, the acquisition also looks a little pricey to me so I am staying on the side lines here.

On the 7th May the group released a statement covering trading during the first four months of the year. All of their businesses have traded in line with management expectations and they remain confident in the prospects for the full year.

On the 2nd July the group released a statement covering trading in the first half of the year. They have delivered a strong result for the period and expect the full year results to be slightly ahead of expectations. The acquisition of London Linen is trading as expected and the integration of the wider textile business is underway. Net debt stood at £73M at the half year point which is slightly below the previous estimate, but still too high for my liking!

It has to be said that this is a good looking chart – obviously the market doesn’t share my concerns abut the company.