Molins has now released its final results for the year ended 2015. As the group has restructured its divisions I think it would be useful to go over the divisional split. The packaging machinery division supplies automated product handling, cartoning and robotic end-of-line packing machinery and systems, and operates from three locations in Canada, the Netherlands and Singapore. In addition it provides technical consultancy and machinery to solve packaging and processing challenges from their base in Coventry.

The Instrumentation and Tobacco Machinery division comprises both the tobacco machinery activities and the quality control, testing and analytical instrumentation business, which has customers in both the tobacco and other consumer goods sectors. The instrumentation business is based in Milton Keynes with sales and service offices in China, India, Singapore and the US. It supplies and supports process and quality control instruments and within the tobacco industry it is the market leading supplier.

The division also designs, manufactures, markets and services machinery for the tobacco industry and provides aftermarket support to its customers globally. This part of the division is headquartered in Princes Risborough where the central engineering and logistics teams are located together with the main distribution centre for spare parts. There is a manufacturing facility based in Brazil which serves the South American markets and the main machining and assembly operation is in the Czech Republic.

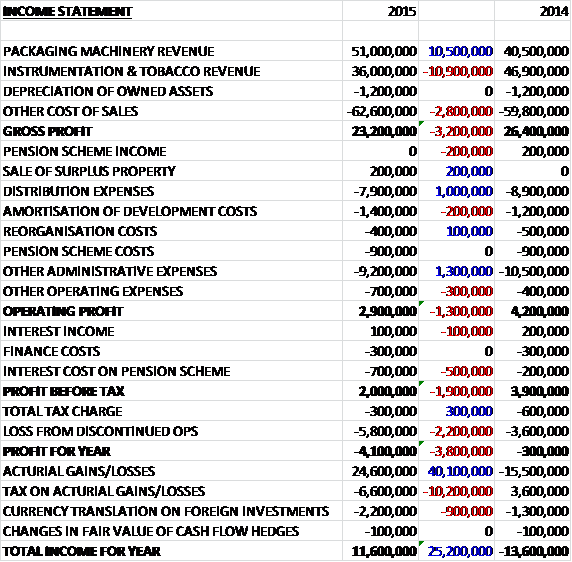

Revenues were broadly flat when compared to 2014 as a £10.9M fall in instrumentation and tobacco revenue was offset by a £10.5M growth in packaging machinery revenue. Cost of sales increased, however, so the gross profit was £3.2M below that of last year. Distribution expenses fell by £1M and other admin expenses declined by £1.3M to give an operating profit £1.3M below that of 2014. The interest on the pension scheme was £500K up but tax fell by £300K to give a profit from continuing operations of £1.7M, a decline of £1.6M year on year. The loss from the discontinued operation meant that there was a £4.1M loss during the year, however, which was a £3.8M deterioration year on year.

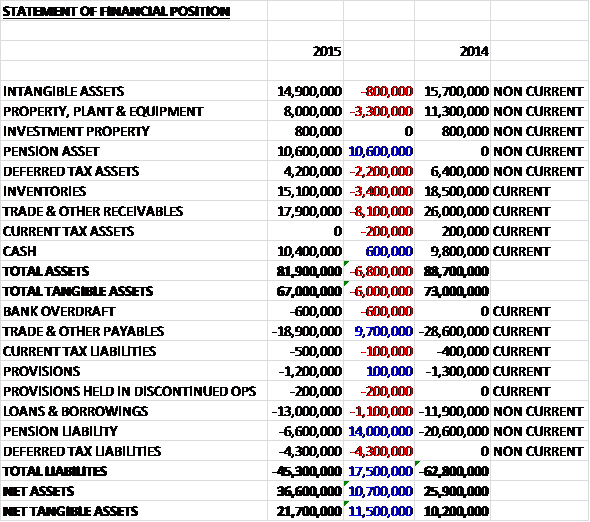

When compared to the end point of last year, total assets declined by £6.8M driven by an £8.1M fall in receivables, a £3.4M decrease in inventories, a £3.3M fall in property, plant & equipment and a £2.2M decline in deferred tax assets, partially offset by a £10.6M pension asset relating to the UK scheme. Total liabilities also declined during the year as a £14M fall in the pension liability relating to the US scheme and a £9.7M decrease in payables was partially offset by a £4.3M growth in deferred tax liabilities and a £1.1M increase in loans and borrowings. The end result is a net tangible asset level of £21.7M, an increase of £11.5M year on year.

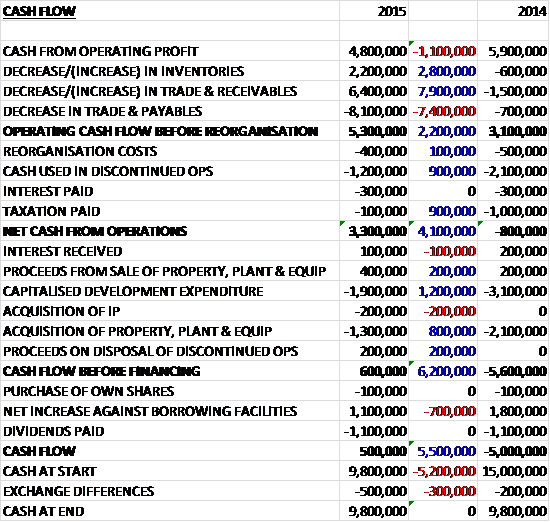

Before movements in working capital, cash profits declined by £1.1M to £4.8M. There was a modest cash inflow from working capital and after that, along with interest, tax payments that were some £900K lower, and £1.2M of cash used in the discontinued operations, the net cash from operations was £3.3M, a growth of £4.1M year on year. The group then spent £1.9M on development expenditure, £200K on the acquisition of IP and a net £900K on property, plant and equipment which left them with £600K of free cash. This did not cover the dividends, however, so they took out £1.1M of new borrowings to pay the dividends and leave a cash flow of £500K and a cash level of £9.8M at the year-end.

Overall the group’s results were in line with expectations. The performance of the packaging machinery division was strong but the challenges within the geopolitical environment and general market sector continued to impact the instrumentation and tobacco machinery division.

The underlying operating profit in the Packaging Machinery division was £3.9M, a growth of £2.1M year on year reflecting the impact of increased operational efficiencies and higher volumes.

These results benefited from the strategy of focusing on a more standardised range of products for the target sectors of nutrition, beverages, pharmaceuticals and healthcare. The international sales and service structures that have been established over the past three years have apparently helped the division to meet the needs of both multinational and regional customers in most parts of the world. They group are continuing to focus on developing their activity in Asia where customers are increasingly using mechanical packaging in order to reduce cost and improved quality.

While sales in the second half showed a significant uplift on the same period of last year, there was a distinct softening in market conditions across all regions in the period with customers taking longer to finalise purchasing decisions. As they entered 2016, this trend continued and the division started the new financial year with a lower order book than last year’s strong position. While they are now more cautious about the trading backdrop, there are a significant number of prospective projects being discussed.

The underlying operating profit in the Instrumentation and Tobacco Machinery division was just £100K, a decline of £3.5M when compared to last year which reflected lower sales across both parts of the division. Within the tobacco machinery business, the contraction in demand experienced in 2014 did not reverse and order prospects remained limited and very competitive, resulting in a reduced overall order intake. They did secure a number of projects with customers in South East Asia, North Africa and North America, however, while continuing to focus on meeting the very specific product and service needs of their customers.

Within the instrumentation business, the reduction in demand from the tobacco industry only started to be felt in Q1 2015. This reduction drove further competitive pricing pressures, which were also exacerbated by the relative strength of sterling against the euro. The order intake in the last part of the year was stronger, however, and the business has entered 2016 with a larger order book that at this point last year. The group have taken further steps to remove cost from the division and reduced headcount in the tobacco machinery business by 20% including the closure of the sales office in Russia. They have also consolidated certain activities in Richmond, USA into the UK operation during the year and will complete a relocation of their operation in Brazil to a smaller and more cost effective site in Curitiba in H1 2016.

In the tobacco machinery business the recent intensive period of investment is drawing to a close with the successful completion of the field trial of the new Alto cigarette making machine in the first half of the year and a product launch for the new Optima cigarette packing machine at the industry show held in London in November. The group are currently focused on expanding their product range in non-tobacco markets, and in the year they purchased the IP for non-invasive thermometry measuring equipment which is mainly aimed at the nutrition sector and they are in the process of bringing it to market.

In May the group sold Arista Labs for £300K which was counted as a discontinued operation during the year. The loss of £5.8M relates to a £900K loss from trading activities, a £3.5M loss on disposal of net assets and a £1.3M impairment of goodwill along with a net £100K cost incurred on disposal.

The group’s pension schemes are worthy of mention. The IAS valuation of the UK scheme resulted in a net surplus at the end of the year of £10.6M with the valuation of the assets at £346.9M and the valuation of the liabilities at £336.3M. The accounting variations of the US pension scheme showed an aggregated net deficit of £6.6M with total assets of £14.9M. The main causes of the improvement in the valuation of the liabilities in the UK scheme were the increase in the discount rate, reflecting higher interest rates at the year-end and a gain arising from a change to the demographic assumptions.

The last completed scheme specific funding valuation of the group’s UK defined benefit scheme that was carried out in June 2012, showed a funding level of 86% of liabilities which represented a deficit of £53M. The company has agreed a deficit recovery plant which commits them to paying £1.7M per annum into the scheme and the payments increase by 2.1% per annum. The deficit recovery plant will be formally reassessed following the completion of the scheme funding valuation which is currently being carried out.

The company is also responsible for paying a statutory levy to the pension protection fund. The quantum of this levy is dependent on a number of factors, including a specific method of calculating a pension deficit for this purpose and a credit assessment of the company. The levy that will be paid in 2016 is largely linked to the group’s financial information reported in 2014 and it is expected that this will result in a payment considerably in excess of the 2015 levy but no actual estimates are given which is a pain.

The board is mindful of the challenges being faced in 2016 which they expect to include a significant rise in the statutory levy payable to the pension protection fund. There is currently little sign of an immediate recovery in the tobacco sector, although the order book at the beginning of the year for instrumentation was strong. The packaging machinery division has made encouraging progress but it entered 2016 with a lower order book and the board are now more cautious about trading conditions, although there are a significant number of prospective projects under discussion.

At the year-end, the group had a net debt position of £3.2M compared to £2.1M at the end of last year. At the current share price, the shares a trading on a PE ration of 7.7 for continuing operations which reduces to 6.5 on next year’s consensus forecast. After the final dividend was reduced, the shares are now yielding 6% which reduced to 4.1% on next year’s forecast.

Overall then this has been another difficult year for the group. Profits declined but net assets improved due to movements in the pension scheme values. Although operating cash flows improved, this was due to more favourable working capital movements and cash profits fell.

There was some free cash generated but this did not cover the dividends. The packaging machinery division performed well, aided by the group selling more standardised products but the outlook looks less certain. Conversely the Tobacco and Instrumentation division performed poorly and while the tobacco industry still looks difficult, the instrumentation division seems to be picking up in 2016.

The pension scheme is still a cause for concern. Although the group is now showing a surplus on its balance sheet, they are still paying out £1.7M a year to fund it which is a material amount for a company of this size. The valuation of the scheme is currently ongoing so it will be important to see the results of that and what kind of deficit reduction payments are required going forward but I would have thought the swing to assets on the balance sheet is a good sign. Of concern though is the fact that the levy to the pension protection found is going to be much higher in 2016. Sadly no ballpark figures are given but the board are cutting the dividend to conserve cash so this is likely to be material.

Going forward, there are no signs of recovery in the tobacco sector and while the instrumentation outlook is looking healthier, the packaging machinery division is entering 2016 with a lower order book. With a forward PE ratio of 6.5 and yield of 4.1% makes the shares look rather cheap but given the softening in the packaging machinery market and the uncertainties surrounding the pension protection levy, I have sold my speculative purchase at a loss.

On the 22nd April the group released a trading update for Q1. Trading was at similar levels to the prior year and while the board continue to be cautious about market conditions, their expectations of group trading for the year as a whole remains unchanged, supported by the current level of order prospects.

On the 11th May the group announced the appointment of Tony Steels as CEO from June 6th with current CEO Dick Hunter stepping down after eight years in the role. In addition, they have announced the appointment of Andrew Kitchingman as a non-executive director. Tony joint the group from Cytec, part of Solvay SA, a chemicals and advanced materials company where he was global business director of the process materials division. Andrew worked in corporate finance with companies including KPMG, Brewin Dolphin and WH Ireland.