Moss Bros have now released their interim results for the year ending 2016.

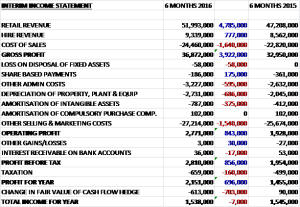

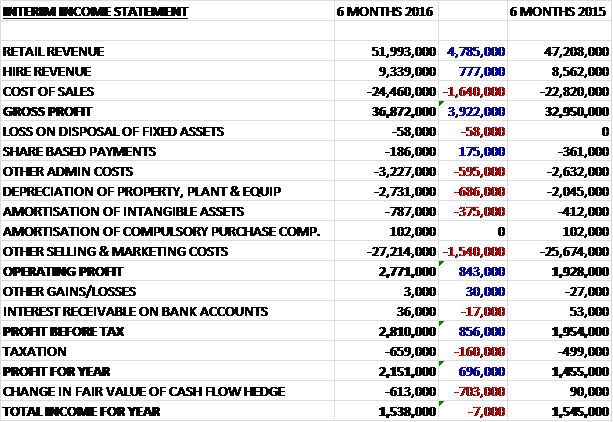

Revenue increased when compared to the first half of last year with a £4.8M growth in retail revenue and a £777K increase in hire revenue. Cost of sales also increased to give a gross profit £3.9M higher. We then see admin costs increase along with a £686K growth in depreciation and a £375K increase in amortisation. This, combined with a £1.5M increase in other selling and marketing costs meant that operating profit grew by £843K when compared to the first half of 2015. After a modest increase in tax, the profit for the period was £2.2M, an increase of £700K year on year.

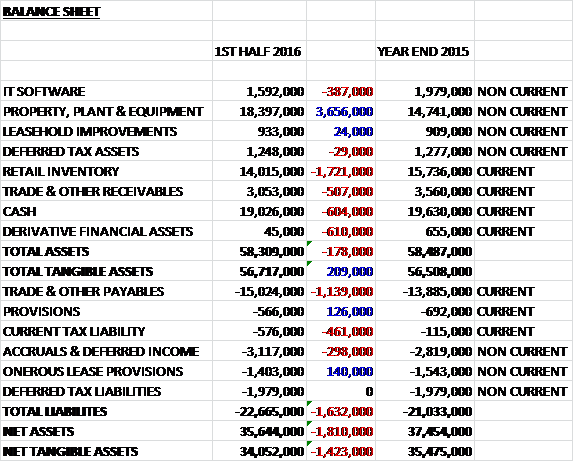

When compared to the end point of last year, total assets fell by £178K driven by a £1.7M decline in retail inventory due to a re-phasing of Autumn/Winter stock intake to better align product availability with customer demand, a £610K fall in the value of the derivative financial asset, a £604K decrease in cash and a £507K fall in payables, partially offset by a £3.7M growth in property, plant and equipment. Total liabilities increased during the period due to a £1.1M growth in payables and a £461K increase in the current tax liability. The end result is a net tangible asset level of £34.1M, a decline of £1.4M over the past six months.

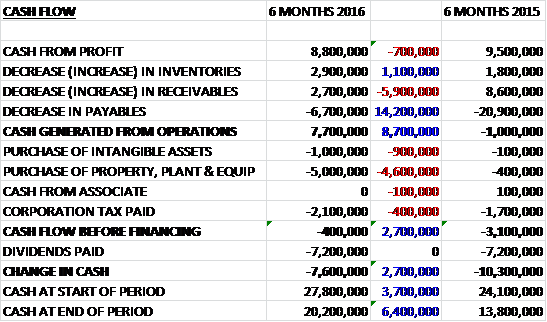

Before movements in working capital, cash profits fell by £700K to £8.8M but a much smaller fall in payables than last year meant that the cash generated from operations was some £8.7M better at £7.7M. The group then spent £1M on intangible assets, £5M on property, plant and equipment, and £2.1M on tax to give a cash outflow of £400K before financing. The dividend payment of £7.2M then meant that the cash outflow for the period was £7.6M to give a cash level of £20.2M.

Gross profit at the retail business was £29M, an increase of £3.3M when compared to the first half of last year. The launch of the new Moss Bros sub brands at the start of the Autumn 2014 season, in conjunction with the ongoing store refit programme has ensured that the customer offer is more closely aligned to the target customer groups. Additionally, the implementation of a more targeted promotional programme in conjunction with improved clearance of residual stocks through the e-commerce “Outlet” channel has enabled the group to improve their gross margin. E-commerce has grown strongly in the period and this trend is expected to continue.

The refit programme to modernise the portfolio continued and the refitted stores continued to achieve payback targets. Eleven were refitted during the period and a further fourteen are planned to be refitted in the second half of the year. In total, 74 stores now trade in the new format and there are apparently signs that this is helping to change customer perception of the business. During the year, four stores have been relocated to larger premises and five have been closed with the estate currently running at 125 stores.

The gross profit at the hire business was £7.8M, an increase of £600K year on year. Hire bookings for the 2015 wedding season are ahead of last year and the average price achieved on hire continued to improve as a result of the introduction of new premium product lines. The introduction of lounge suits in particular has been very successful and has enabled them to broaden the wedding hire offer. Royal Ascot and eveningwear also showed growth. The impact of the improvement in wedding hire bookings will reduce in the second half, however, as they move out of the wedding season and into the evening wear season.

The online capability continued to grow with e-commerce retail sales up by 55% on the previous year. Traffic flow, conversion and customer retention all continued to improve. The group have launched a country specific US site during the period to add to the sites serving Ireland, Sweden, Denmark, Netherlands and Australia with international sales now making up 3.1% of the online total. Mobile traffic continued to grow strongly and is now 23% of online sales. A number of upgrades were made to the hire website during the period and online hire continues to gather momentum. Overall, online sales now comprise some 10% of the total group revenue.

The group are at the early stages of testing the retail proposition in international markets and will ensure they understand the resonance of the brand before jumping in. A two store pilot in the Middle East is being undertaken with a franchise partner and the first one is expected to open in the second half of the year.

One thing to bear in mind is that the introduction of the living wage in 2016 could lead to higher employment costs. The group are undertaking a review and redesign of remuneration to align potential reward with the achievement of their objectives and incorporate the living wage. Given the intended improvement in the design of the remuneration packages to reward improved performance, together with operational efficiencies, it is not expected that the introduction of the living wage will have a material impact in the short to medium term.

It was announced that Finance Director Robin Piggott is intending to retire at the AGM next year.

The early response to the Autumn/Winter retail range is positive with trading in the first eight weeks of the second half has been good with like for like sales up 10.4% (compared to 9.7% in the first half of the year) and the financial performance continues to be in line with the board’s expectations for the full year.

At the current share price the shares have an impressive dividend yield of 5.4% which is expected to remain the same for the full year. The shares currently trade on a PE of 26.3 which looks rather expensive but this is forecasted to come down to 18.4 for the full year this year which looks a bit more palatable.

Overall then this was a good update from the group. Profits increased year on year as did operating cash flow but in the case of the latter, this was only due to a huge increase in payables last time and underlying cash profits actually fell during the period. Net tangible assets also fell modestly which is perhaps a symptom of the large dividends. The retail business continued to grow with the refits and new brands driving this growth, along with the speedy clearance of old stock online. More pleasingly perhaps, is the growth seen in the hire business as the wedding season improved and new products added to the offering. Of course, there will be less weddings in the winter months but hopefully the evening wear can pick up the slack.

The online business really seems to be making progress and the tentative international expansion is intriguing. So far in the second half trading has been good and with a dividend yield of 5.4% these shares look rather tempting to me. The rather high valuation with regards PE ratio is something to look out for though.

Is this is a bit of a recovery I see here?

On the 14th January the group issued a trading update covering August to mid-January where they stated that they continued to make good progress and were trading in line with market expectations. Like for like sales were up 4.2% and total sales were 4.8% ahead of last year. Retail sales, comprising 86% of total revenues, continued to benefit from the increasing number of refitted stores now trading and the more authoritative brand and price proposition with total retail sales up 3.5% on a like for like basis. Hire sales increased by 9.5% like for like with a successful eveningwear season maintaining the momentum achieved in the first half of the year.

Overall gross margins for the half year to date improved by 2.8 percentage points, am improvement of the 1 percentage point increase in the first half of the year largely due to an improvement in retail gross margins which have benefited from the continued focus on more coordinated and targeted promotions despite the unseasonably warm autumn weather. E-commerce sales were up nearly 33% in the year to date with mobile and tablet sites continuing to grow strongly. A total of 21 stores were refitted during the year to date and a further 20 are planned next year with the refitted stores continuing to achieve the expected turnover increases.

The group expects to end the year with a net cash balance of £17M compared to £19.6M at the end of last year.

On the 19th February the group announced the appointment of Tony Bennett as finance director. He is currently finance director at Charles Tyrwhitt, a multi-channel menswear retailer. The group has also appointed Paula Minowa as COO, which is a newly created role. She was previously CEO of Strauss Innovation, a German multi-channel lifestyle retailer.