Murgitroyd has now released its interim results for the year ending 2015.

Revenues were flat when compared to the first half of last year, increasing by just £61K and a growth in the cost of sales meant that gross profit was some £375K lower. Admin expenses did fall somewhat due to tight cost control, and the interest on the loan was slightly lower so that profit before tax was down by £300K year on year reflecting the ongoing investment in new business and the fact that current US margins are lower than elsewhere. After tax, the profit for the year was £1.4M, a fall of £201K.

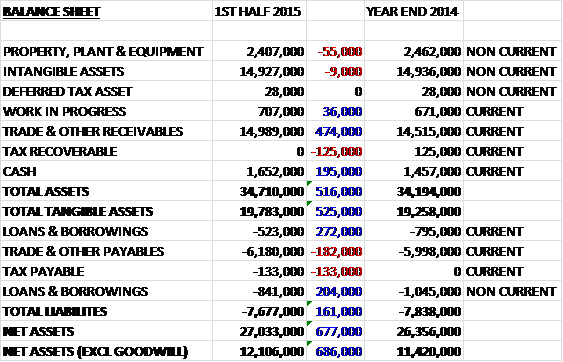

When compared to the end point of last year, total assets at the half year point increased by £516K, driven by a £474K growth in receivables and a £195K increase in cash partially offset by a £125K fall in tax recoverable. Total liabilities fell during the period as a £476K fall in borrowings was partially offset by a £182K increase in payables and a £133K growth in tax payable. The end result is a £686K increase in net tangible assets to £12.1M.

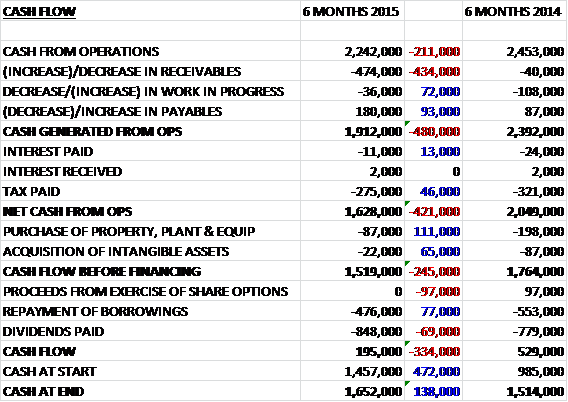

Before movements in working capital, cash profits fell by £211K to £2.2M. This was eroded further by an increase in receivables, partially offset by a smaller tax bill to give a net cash from operations some £421K lower than in the first half of last year at £1.6M. There was then negligible capital expenditure so that the free cash flow stood at £1.5M, a £245K decline. Much of this was spent on dividends but the group also managed to pay off £476K of borrowings to give a cash flow for the first half of the year of £195K. Despite the fall in operating cash, I do like the fact that the group is using its free cash flow to pay down debt.

The IP Portal filing service is proving increasingly popular amongst clients and there are adequate resources in place to provide for the growing number of larger corporate users. The investments made in internal and client facing systems continue to deliver cost reductions in a market that is facing pricing pressure. Business from the US saw significant growth of 22% in Sterling terms and the country remains a key focus for investment and an increasingly important growth market. It is the largest source of European Patent applications and its growing presence in the market is helping to offset the effects of a stagnating market in Europe with the group addressing the operating businesses on a country by country basis.

In 2014 the number of Community Trade Mark applications filed increased to 117,000 which set a new record despite the rate of growth slowing compared to previous years. The European Patent Office also reported a 3% year on year increase in Patent filings for the year with the number of applications rising to an all-time high of 273,000. Within these filings, applications from the US increased by 6.7%, Japanese applications fell by 3.8% and European applications were flat.

Apparently the group remains on track to meet its revenue and earnings targets for the full year with trading in line with expectations and an expectation of a better performance in the second half. Although markets remain challenging, the group are confident that the investments made will enable them to deliver long-term and sustainable growth. They have also pointed out that they continue to seek earnings enhancing acquisitions but so far nothing has been announced.

Following a 13% increase in the interim dividend, the shares currently yield 2.3% increasing to 2.5% on the full year ending 2015 estimate after the board have suggested they will be targeting an increase for the final dividend too. At the end of the period the group was in a net cash position of £288K compared to a net debt of £827K at this point of last year.

Again, this half year was a bit of a mixed bag for the group. Profits fell year on year as did operational and free cash flow, although the group still generates enough cash to continue paying down its debt. Net assets did rise, however. It is difficult to know what to do here. On the one hand we have a company that generates copious free cash flow and is steadily paying down its debt but on the other there is a market that is growing but experiencing increasing pricing pressure – with the growth market of the US having lower margins. I would like to buy in here but I think I would like to see some evidence of growth before I do.

On the 11th February, the group announced that non-executive director, David Gray, has resigned from the Board, effective today. A process to replace Mr Gray is underway.

The shares certainly seem to be on their way back up again but it is hard to see exactly why – a tricky one this!

On the 12th August the group announced the appointment of Gordon Stark, aged just 38, to the executive board and Dr Christopher Masters and John Reid as non-executive directors.

Gordon is the current COO of the subsidiary, Murgitroyd so it looks as though he has been promoted. Christopher was executive chairman of Aggreko and is currently non-executive chairman of Energy Assets. John founded his own consultancy, ReidStewart Associates and prior to that he was group commercialisation manager of the Intermediate Technology Institute.