N Brown has now released its interim results for the year ending 2017.

Revenues grew when compared to the first half of last year with a £2.4M increase in services revenue and a £1.7M growth in the sale of goods revenue. Cost of sales increased by a greater degree, however, and gross profit fell by £5.1M, apparently related to the promotional stance taken during the tough trading in the first half. Marketing and production costs increased by £1.5M and depreciation & amortisation was up £1.4M but there was no loss on disposal of fixed assets which was £700K last time and the share option charge fell by £600K, offset by other admin costs that increased by £1.2M. There were no reorganisation costs (£5.3M last time) or clearance store closure costs (£8.9M) but there was a £600K growth in VAT related costs and a £9M charge relating to financial services customer redress, all of which meant that the operating profit declined by £3.1M. The group benefited from a £500K reduction in the fair value adjustment to the forex hedge and tax charges fell by £500K to give a profit for the period of £16.9M, a decline of £2M year on year.

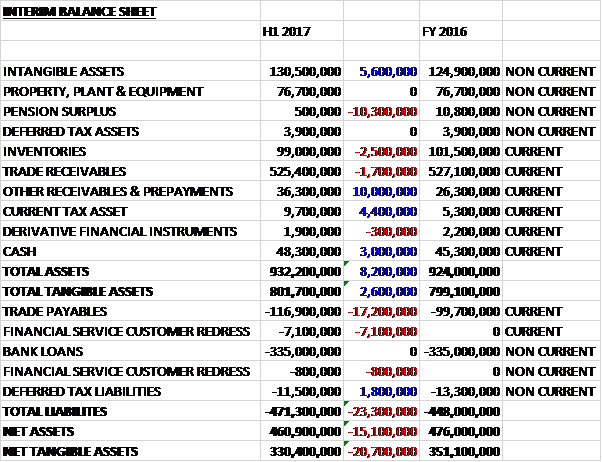

When compared to the end point of last year, total assets increased by £8.2M to £932.2M driven by a £10M growth in prepayments and other receivables, a £5.6M increase in intangible assets and a £4M growth in current tax assets, partially offset by a £10.3M decline in the pension surplus, a £2.5M fall in inventories and a £1.7M decrease in trade receivables. Total liabilities also increased during the period as a £17.2M growth in trade payables and a £7.9M financial service customer redress provision were partially offset by a £1.8M decline in deferred tax liabilities. The result was a net tangible asset level of £330.4M, a decline of £20.7M over the past six months.

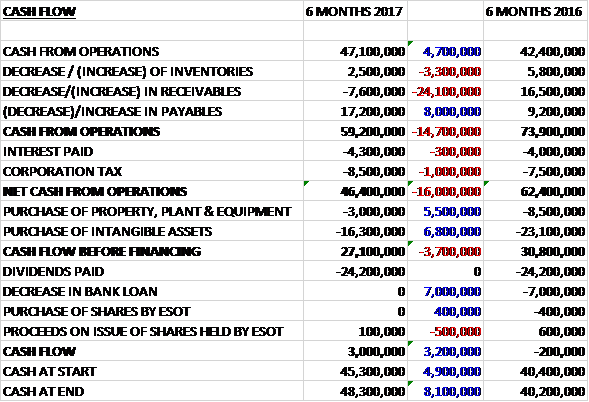

Before movements in working capital, cash profits increased by £4.7M to £47.1M. There was a cash inflow from working capital but this was much less than last year and after a £1M increase in tax payments and a £300K growth in interest payments, the net cash from operations came in at £46.4M, a decline of £16M year on year. The group spent £3M on property, plant and equipment mainly relating to warehousing along with £16.3M on intangible assets reflecting the spend on IT for the Fit for Future project which left £27.1M in free cash which covered the £24.2M paid out in dividends to give a cash flow for the period of £3M and a cash level at the end of the half of £48.3M.

The active customer file declined by 1.5% due to a weak sector backdrop and ongoing headwind from the Fifty Plus and Traditional Titles. Power Brand active customers excluding Fifty Plus grew by 14.7% reflecting the reduction in Fifty Plus customers as the group reduced marketing spend ahead of its migration into JD Williams.

Market share in Ladieswear was flat at 4.3% in a relatively weak season. Within this they gained share in younger ladieswear driven by Simply Be and lost it in the older segment. Menswear market share increased by 20bbp to 1.3%. The group continue to expand their offering of third-party brands with new introductions being Wold and Whistle, Vero Moda, Religion, Helene Berman, Not Your Daughters Jeans, Timberland, Ann Summers and Gossard.

Credit arrears were 9.8% during the first half, down 30bps driven by an improvement in the quality of the debt book. The credit provision rate was 12.7%, down 280bps against last year. This benefitted from a small quantum of high risk payment arrangement debt, which the group was able to sell for a slightly better rate than book value. Assuming no further debt sales, the group expect both the credit provision and arrears rate to remain broadly flat through the remainder of the year.

JD Williams product revenue was £75.8M, broadly flat year on year with the JD Williams brand itself up 11% and Fifty Plus down 18% as the group reduced marketing investment ahead of its migration into JD Williams. Trialling has commenced but given the size of the customer file the migration will take place over two seasons. The group expect the headwind to unwind as they go through this proves and the key priority will be optimising the customer experience to secure future growth potential. There is good momentum in the JD Williams brand itself with a 20% growth in active customers. Last month they introduced a collection of their best priced, current season clothes to further reinforce their value for money credentials and sales of these lines have exceeded expectations, with sales up 75%.

Simply Be product revenue was £53.3M, up 6.2%. In line with the wider sector, spend per customer in Spring Summer was down year on year but the business was helped by a single digit increase in active customers. The fast fashion sub-range continues to perform strongly with revenues near doubling during the period. The new share and sculpt denim range, launched in July, has seen sales exceed expectations. The group have also announced that they will be launching a Simple Be shopping app ahead of peak trading this year.

Jacamo product revenue was £31.4M, up 3.3%. Sportswear was particularly strong, driven in part by expanded ranges in this category. The collaboration with Jonnie Peacock last season was well received and they launched their Autumn campaign with rugby player Dan Biggar. Social engagement is increasingly important for this brand with FlintoffVsSavage in June a particular highlight in the period. As part of a wider opportunity to access new customers through selling their brands on partner website, they will be trialling a capsule collection of Jacamo on ASOS from January.

Secondary brand revenue was £75.2, up 0.4% year on year. The best performing brand in the first half was Fashion World, which has the highest credit usage across all brands. High and Mighty is transitioning from a predominantly stores to online model. Figleaves went live with a new Demandware web platform in September which will allow them to be more effective in driving future customer recruitment.

Revenue from the traditional segment was down by 4.2% to £65.2M in line with expectations and an improvement from the 5.5% decline last year. Amongst a number of improvements the new mailing materials feature more age appropriate models, copy text that resonates with the traditional audience and strong value messaging throughout the publication. All this is backed by bespoke email campaigns. The group have reinvested back into the product choice, particularly jersey and nightwear and have seen significant increases in sales as a result. The actions taken to improve performance are starting to have a positive impact as they enter the new Autumn Winter season.

The US continues to represent a significant growth opportunity. Revenue was £7.7M, up 24.5% and 14.7% on a constant currency basis. The operating loss was reduced to £500K compared to £900K last time. The majority of the US revenues are generated by the Simply Be brand but in March they launched the JD Williams brand in the country and performance to date has been encouraging. They have reduced their marketing programme during the post-launch period of the new website which will impact performance. Ireland revenues of £7.2M were up 12.4% or just 3.8% at constant currency, driven by improvements to the product offering.

Store performance in the period was disappointing with like for like revenue down 9%, although following corrective actions, performance is improving. During the period they reduced the High and Mighty store portfolio and overall thee was an operating loss of £900K compared to £200K last year.

An exceptional charge of £9M was recognised during the period reflecting costs incurred or expected to be incurred in respect of payments for historic financial services customer redress. There were also costs related to taxation matters which are legal and professional fees related to ongoing disputes with HMRC. It is important to note that the group is actually recording an asset of £28.7M relating to cash payments made under protective assessments raised by HMRC which based on legal opinion they believe they can recover in full. Clearly this is open to some uncertainty and risk.

With regards the Fit 4 the Future programme, to date they have landed Cybersource and Power Curve which are key parts of the Credit transformation; phase 1 of the new merchandise systems; the Simply Be Euro foundation site and the new US website. They re-platformed the US website to Hybris and this went live in late September. Through the process of implementation and testing they realised they required more time to deliver the customer experience required for the brands than originally expected.

The rollout timetable for the remaining Fit 4 the Future programme has been extended due to what has been learned from the US launch. The additional cost will be incorporated into 2018 capex of around £40M compared to previous guidance of between £30M and £40M. The new timetable will see the launch of the first UK site with an integrated credit proposition in Q1 2018; this was previously planned for launch prior to the 2017 peak trading period. The planned timing of the Simply Be release has moved from Q1 to Q3 2018 but as this will represent the point of the project when the majority of the online customer functionality has landed, they will then be able to significantly step down the programme. Sire rollout will then be moved into normal business activity which is planned to finish by summer 2018.

The Brexit vote and the subsequent weakening of Sterling represents a challenge for the entire retail sector. The group have now almost entirely hedged their dollar purchases for 2017, which has resulted in a smaller headwind than the previous guidance of £3M, with these savings reinvested into promotional activity. For 2018 they have hedged 50% of their dollar purchases at a rate of £1.30 per dollar. At a rate of £1.25 per dollar this would result in a £7M headwind and every five cent move from this rate results in a profit sensitivity of £1.5M although a number of mitigating activities are underway including fabric and production planning, markdown optimisation and ongoing work on supplier consolidation.

Since the period-end, the group have been granted full unconditional FCA authorisation for their financial services model. In addition the US website went live. Going forward the group have started the Autumn Winter season on plan and at this stage the board are comfortable with current market expectations for the full year.

At the current share price the shares are trading on a PE ratio of 9.8 which falls to 8.3 on the full year consensus forecast. After the interim dividend was left unchanged, the shares are now yielding a hefty 7.5% which is expected to remain the same for the full year. At the period-end net debt stood at £286.7M compared to £239.8M at the same point of last year.

Overall then this has been a rather difficult period for the group. Profit fell, as did net assets but although the operating cash flow declined, this was due to working capital movements and cash profits actually grew with a decent amount of free cash being generated. Operationally, Simply Be, Jacamo and the US business have performed well, although the latter remains loss making. JD Williams had a flat year, but its performance was dragged down by Fifty Plus which could be a temporary issue? The stores and the traditional segments are more concerning, both seeing revenues drop although the board say performance is turning around.

The fit for the Future scheme is still ongoing and has been delayed so this represents a real risk factor and now that performance seems to have turned a corner I think it is this uncertainty that is dragging down the share price. On the surface the forward PE of 8.3 and dividend yield of 7.5% look very cheap but it is a risk given the above with the added issue that the debt levels are close to being problematic. Could be worth a punt though?

On the 19th January the group released a trading update covering the Christmas period. Group revenue increased by 4.1% which included a 5.9% increase in product revenue and a 0.5% reduction in financial services revenue. Overall the group are on track to meet full year expectations.

Power brands revenue was up 10% and the active customer file increased by 13%. The group are in the process of migrating customers from the Fifty Plus title into the JD Williams brand. This process is on track and, although it still represents a headwind, this has materially lessened with Fifty Plus broadly flat year on year. Simply Be revenue grew double digit year on year, driven by continued improvements in the product range and a strong online marketing campaign. Jacamo grew mid-single-digit against a tough comparative last year.

The support brands and traditional segment both recorded low single digit revenue growth. Within the support brands the strongest performer was Fashion World. The traditional titles are now back into positive year on year growth, benefiting from the actions taken to improve product and presentation over the season.

At the category level, ladieswear recorded the strongest growth by some measure, up double-digit. Menswear and Homeware both recorded mid-single digit revenue growth and Footwear was flat. There was a further improvement in group returns rate year on year. Total online sales were up 12% and order frequency and units per basket both record good year on year growth, although average selling price was down slightly as the group “invested in price”.

They launched their new US website in September, slightly later than initially planned. This impacted performance through peak, as expected, with revenue down 3.5% and 19% on a constant currency basis. The site is performing well and the board remain confident in the market opportunity going forward.

During the period financial services revenue was marginally down year on year. This masks two moving parts, with interest received up and non-interest lines such as admin charges down as the quality of the debt book continued to improve. This resulted in higher overall gross profit from financial services, and they have therefore upgraded their gross margin guidance for the year. During the period they launched a trial of differing interest rates for new customers. Whilst it is too early to assess the trial fully, the initial view is encouraging.

The systems transformation project is on track. The first UK site, which will be High and Mighty, is still planned for Q1 2018. In Q3 they will now be launching Fashion World instead of Simply Be as previously announced which has a greater proportion of financial services usage. There is no change to the overall programme costs and benefits. The launch of the new Fashion World site represents the point in the project where the majority of the online customer functionality will have landed, and they will then be able to significantly step down the programme. Site rollout, including Simply Be, will then be moved into normal business activity and they continue to expect the rollout to finish by summer 2018.

The updates to full year guidance include gross margins narrowed to -100bps to -150bps (from -50bps to -150bps) due to more promotions; financial services gross margin improved to +75bps to +125bos (from +50bps to -50bps) due to continued improvement in the quality of the credit book; group operating costs range narrowed to +3% to +4% (from +2% to +4%) due to higher volumes an depreciation/amortisation slightly lower from £29M-£30M to £28M – £29M. All other guidance remains unchanged.

Overall then, this seems to be a solid update and the group is progressing well. There remains considerable headwinds including the national living wage and the systems upgrade but I am tempted to think the low share price adequately provides for this. I am considering a purchase here.

On the 11th April the group released a statement where they said the exceptional costs relating to financial service customer complaint redress was likely to increase from £9M to more than £22M! The expected amount has increased because the FCA deadline for complaints has been announced as August 2019, a year later than previously indicated; they have experienced a greater number of complaints than expected due to wider public awareness; and the age profile of complaints received is typically older than previously experienced.