Newmark Security designs, manufactures and supplies products and services for the security of assets and personnel. The group has two main segments. The Electronics division is involved in the design, manufacture and distribution of access control systems (hardware and software) and the design, manufacture and distribution of WFM hardware only, for time and attendance, shop floor data collection, and access control systems with the division accounting for 33% of revenues. The majority of customers in this division are security installation companies dealing directly with end users. For WFM equipment, the majority of the customers are value added resellers but the business has the ability to work on special projects directly with end users in order to meet specific user requirements.

The Asset Protection division is involved in the design, manufacture, installation and maintenance of fixed and reactive security screens, reception counters, cash management systems and associated security equipment with this division accounting for 67% of revenues. Customers in this division range from leading blue chip organisations to single sites, including banks, building societies, post offices, police forces, railway companies, local authorities, government departments, petrol outlets, hospitals, convenience stores, retailers and supermarket chains.

Sales of equipment including hardware and software are recognised when the customer takes ownership but service, maintenance and license revenue is spread evenly over the term of the contract and the proportion related to the period after the year-end is included within deferred income. Other sales include installation and refurbishment work which is recognised on completion.

Newmark Security has now released its final results for the year ended 2015.

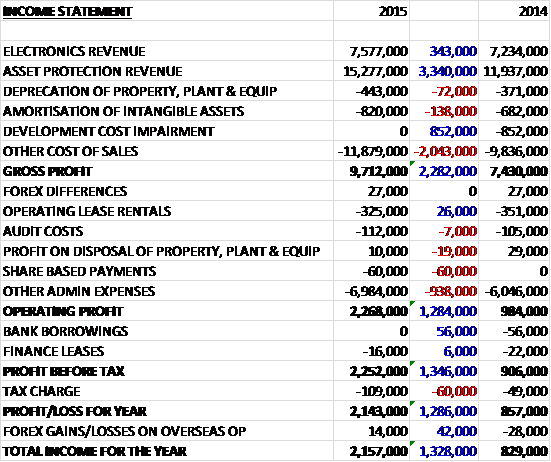

Revenues increased when compared to last year with a £343K growth in electronics revenue and a £3.3M increase in asset protection revenue. The £852K development cost impairment that occurred last year was not repeated but other cost of sales did increased by £2.2M which gave a gross profit £2.3M ahead of last year. Admin expenses were also up but the operating profit was still £1.3M above that of 2014. The fall in loan interest payable was broadly offset by a growth in the tax charge which remained low due to the availability of accumulated tax losses and R&D allowances. This all meant that the profit for the year came in at £2.1M, a growth of £1.3M year on year.

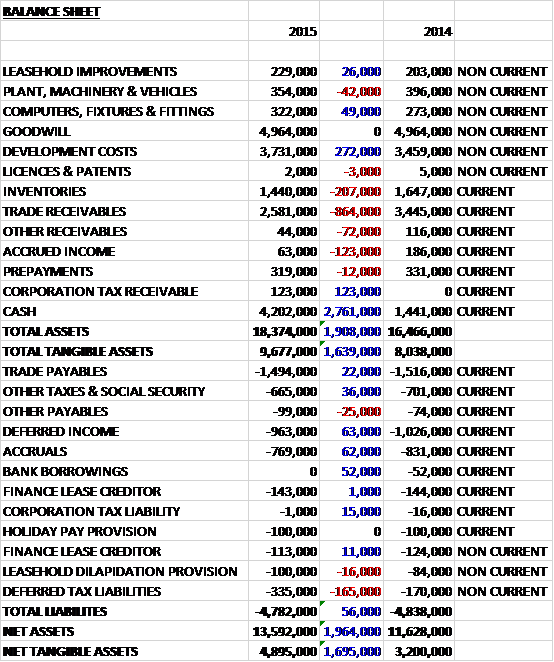

When compared to the end point of last year, total assets increased by £1.9M driven by a £2.8M growth in cash and a £272K increase in development costs as they were higher than amortisation during the year, partially offset by an £864K decline in trade receivables and a £207K fall in inventories. Total liabilities were broadly flat over the year as a £165K growth in deferred tax liabilities was offset by small falls in most other liabilities. The end result is a net tangible asset level of £4.9M, a growth of £1.7M year on year.

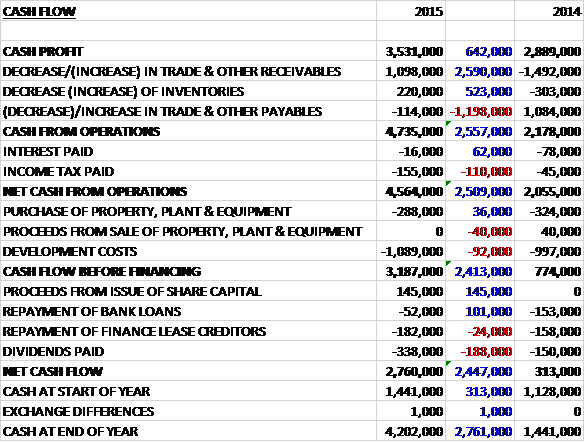

Before movements in working capital, cash profits increased by £642K to £3.5M. There was a cash inflow from working capital compared to an outflow last year, mainly attributable to a fall in receivables following an exceptionally high figure last year due to the advance billing of customers and high sales prior to the year-end, and after a £62K fall in interest paid was offset by a growth in income tax, the net cash from operations came in at £4.6M, a growth of £2.5M year on year. The group then spent £288K on capex and £1.1M on development costs so that free cash flow was £3.2M. Of this, £182K was used to pay finance leases and £338K went out in dividends to give a cash flow for the year of £2.8M and a cash level of £4.2M at the year-end.

The pre-tax profit in the Electronics division was £48K, a decline of £164K year on year partly due to a £138K growth in amortisation charges. Access control revenues grew by 1.3% to £4.1M during a transitionary period. The SATEON range was expanded to include the newly launched SATEON Pro and creating separate and specific offerings focused on the high-tier and mid-tier sections of the market and the business has upgraded some existing customers from the JANUS legacy systems.

During the year SATEON version 2.7 and 2.8 were released. Version 2.7 featured a number of updates that included improved reporting and search functionality and integration with two major elevator companies. Version 2.8 featured new graphical tools, real time maps, time patterns, custom reports and several integrations including Honeywell’s Galaxy Intruder panel, Tyco’s Simplex Fire Alarm plane and Assa Abloy’s Aperio offline locks. Version 2.9, to be launched in August 2015, will contain photo verification via the Stateon Faces feature and will look to build the group’s wireless locks capability through integration into Salso’s offline locking solutions. SATEON has become the solution of choice for a number of public sites including museums and several local authorities along with a major data centre have also chosen to partner with Grosvenor for their access control needs.

Overseas, sales and technical resource has been increased in the US operation with a healthy pipeline of sales opportunities being established. A contract with a major Middle East systems integrator in the UAE was won during the year, securing a robust long-term pipeline for projects in the region. Grosvenor’s Asia Pacific operations have been set up with Hong Kong activing as the hub as an office was established in June. It is envisaged that networks of systems integrators will be established in Japan, South Korea, Singapore and China.

Workforce Management revenues grew by 9.1% to £3.5M. Grosvenor continues to benefit with healthy revenue from the long standing relationship with one of the world’s largest retailers as they continue to roll out their workforce management solutions in their stores globally. A further opportunity exists with this client in terms of an additional roll out with a product designed to meet their specific requirements. During the year the business also completed a long term project for Tesco which was carried over from the previous year.

In principle terms were agreed with a major US channel partner in July for the exclusive supply of a workforce management terminal, which is expected to begin in the year ending 2017. This is the largest single contract secured to date by the group in this line of business. It is also expected that significant revenues will be generated from this customer during 2016 on the existing range of workforce terminals. Cross-selling opportunities began to be recognised during the year with Grosvenor being chosen to supply Workforce Management and Access Control in sites such as a major library, food group and charity.

The pre-tax profit in the Asset Protection division was £3.4M, an increase of £1.5M when compared to last year, partly as a result of the £852K impairment in development costs that was incurred in 2014 as a consequence of the redevelopment of a product design. Product revenue increased by £3.5M to £12.2M which included a growth of £1.2M in CSI revenues after it was acquired in November 2013. Excluding CSI, revenue increased by 29%, principally due to the timing of orders received for time delay cash handling equipment from the Post Office and accelerated installation of equipment at Post Office branches in Q3 and Q4 to meet their targets. Sales of new cash handling products developed for a high street bank in 2012 continued despite competitor products being introduced to the market.

Orders for new Eclipse Rising Screens and screen reconfiguration work increased by 120% after a long term customer accelerated its branch refurbishment programme planned for several years. Sales of Eclipse Rising Screens also increased to financial institutions who previously opted to have no security screens and trade over open counters after they reviewed the security risk at branches that fall in high crime areas. There was also an increase in sales to public sector clients as the government released money for capex programmes.

Eye2eye sales continued to decrease as a results of a reduction in train station refurbishment programmes. Counter Shield sales decreased substantially due to increased demand for Eclipse Rising Screens and Fixed Glazing solutions but they received a substantial order of £174K from a local authority at the end of the year for installation in Q1 2016. Sales of Fixed Glazing and Counter Protection Systems returned to previous levels after the inclusion of a single large order of £373K from a foreign embassy based in London in the previous period. Sales of other non-standard products increased by 26.4% with the benefit of a programme for non-traditional work from a large financial institution.

CSI sales in the year were lower than expected due to the cut backs from a major supermarket chain after poor financial results. The cut backs included the reduction in store numbers as well as the cancellation of plans to open new stores. The business did successfully obtain government CPNI certification on a blast door, however, and this product as well as other products developed during the year will provide significant revenue streams in future years. Continuous produce development and certification as well as a re-certification will reduce margins but they are essential requirements to ensure products are updated to withstand new methods of attack and meet customer demand.

Revenues from the Service stream declined by 4.1% to £3.1M but profitability was higher due to margin improvements driven by reduced unit labour costs. During the year Safetell signed a new service contract with a long standing customer for a further three years and since the year-end the business has also renewed a four year service contract with a large facilities management company to support one of the high street financial institutions. These contracts provide the foundation of the group’s service business.

It has taken longer than expected to enter the more competitive CCTV and access control markets but these products have added to the group’s counter and screen offering which will provide product revenue, as well as additional service revenues in the future. The upgrades to older Eclipse Rising Screen systems have proven successful for two long term customers who will embark on roll-out programmes during the next year to replace the pneumatics and control systems on units that have been installed for many years. These upgrades extend the life of the Eclipse product while reducing the cost of replacing the product and the board believe this will provide revenue streams going forwards. The business continues to receive reactive call outs on the Post Office Transformation Programme.

The two new STATEON lines both operate with a single software platform allowing a simple movement from one door system to the most complex multi-site installations. This will facilitate growth in a far larger number of installers, many of whom currently use different manufacturers to satisfy their small and large system needs. Annual recurring software agreements pave the way for an “Access Control as a Service” model significantly increasing opportunities for new and recurring revenue for both Grosvenor and the systems integrator companies. A leading CRM is being installed to provide capability to manage this increased demand and in the medium term e-commerce technologies will also be adopted, negating the requirement to create costly and complicated distribution channels.

In Workforce Management Systems, growth will be achieved through emphasis on securing new business with high value VARs. Market research has demonstrated specific customer groups where success is more likely and a focused approach has been adopted to target these.

The strategy in the Asset Protection division is to broaden the customer base and product range. Safetell is looking to extend into sectors outside the financial services sector following the acquisition of CSI who address supermarket and retail chains, particularly with ATM pods, BR doors and walls, and fire exit doors. By obtaining government CPNI certification on the blast door, the business had broadened the scope for the ballistic and blast product range and has already received a substantial order for these doors from Iraq.

The Cash Deposit Device developed last year received good reviews from retailers in the UK who are slow to take up new technology whilst still maintaining current cash handling practices. The service provides real cost savings including same day credit, but this is dependent on the UK banks offering the service and currently they are reluctant to move forward with an offering that is already applied by banks in the rest of the world. This networked point of sale cash deposit device provides secure cash holding and device sharing between several cashiers resulting in substantial cost savings.

The group still has some £2.2M in trading losses that can be offset against future trading profits along with £786K of management expenses. They do not currently have any bank borrowings, with the only debt being finance leases but there are undrawn borrowing facilities of £750K which expires within a year. The net cash position stood at £3.9M at the year-end compared to £1.1M at the end of last year but there are £1.6M of outstanding operating leases relating to properties.

There is a modest risk of changes in forex movements. A 10% weakening of the US dollar and Euro against sterling has the effect of reducing profits by just £6K. It is worth noting that as part of loan note facility taken out in 2011, the company entered into a warrant instrument with the loan note holders whereby the company granted then 30,000,000 warrants to subscribe for the same number of new shares until the end of November 2016 at an exercise price of 1p per share. As of the year-end there 29,250,000 warrants outstanding with non-executive Michael Rapoport having 7,500,000 and Chairman Maurice Dwek having 21,750,000 outstanding.

The group is reliant on customer refurbishment programmes within the financial sector which are currently acting as an underlying positive trend for many of their products and the business is reliant on the timing of these programmes. Operating performance is also impacted by the pricing and availability of key raw materials which include electronic components, steel and security glass, the pricing of which can be quite volatile.

Revenue was lower in the second half of the year than in the first half due to the timing of customer projects and roll out programmes. The group therefore focused on new business and products in order to maintain their position in the market. They have agreed in principle terms with a major US channel partner for the supply of a new workforce management terminal which is expected to begin in the year ending 2017 which will be the largest single contract secured to date by Grosvenor Technology.

The asset protection revenues going forward are expected to be lower than during this year due to the completion of some major customer programmes, although revenue from CSI is expected to increase. Overall the board believe that profits in the new year will be lower than in 2015 whilst they develop new markets and products from which the benefits will be seen in the following year.

At the current share price the shares trade on a PE ratio of 6.8 which increases to 13.2 on the full year consensus forecast. After the final dividend (there is no interim dividend here) was increased by a third, the shares are currently yielding 3.4% which remains the same on next year’s forecast.

Overall then, this has been a good year for the group. Profits were up, net assets increased and a growth in operating cash flow gave rise to a decent level of free cash. The profit in the electronics division did decline, however, mainly as a result of increased amortisation and flat sales in the access controls division, although there seem to be some exciting international opportunities with a big contract being signed in the US. Profits in the Asset Protection division grew, mainly as a result of the timing of orders from the Post Office.

This impressive performance doesn’t look as though it is going to be repeated in 2016, however, as the board have guided to lower profits as new products work their way through the system. More generally, the group is dependent on refurbishments from bank customers and the number of stores at their grocery clients, which are obviously under strain at the moment. These issues do seem to be somewhat priced in, however, with a forward PE of 13.2 and dividend yield of 3.4% the shares do not look that expensive to me – this is an interesting one.

On the 18th September the group announced that it had secured a contract with a major global workforce management partner for the development, manufacture and supply of one of Grosvenor’s next generation terminals. The contract is for a period of ten years with guaranteed revenues of $6M over the first five years with the partner having exclusivity for the terminal for six months form its launch, with the exception of one existing major customer.

Example applications for the terminal include attendance recording, collaborative shift planning, shop floor data collection, health and safety briefings and staff training. Overall, this looks to be a positive development for the company.

The group also announced a grant of options over 1,142,857 new shares to CEO Marie Claire Dwek at an exercisable price of 3.325p per share. Given the exercise price I have no qualms over this but it would be nice if she owned some shares in the company that were not gifted to her.