Newmark Security has now released its interim results for the year ending 2017.

Revenues declined when compared to the first half of last year as a £3M fall in asset protection revenue was only partially offset by a £187K growth in electronics revenue, Cost of sales declined by £1.3M to give a gross profit £1.5M below that of last time. Admin expenses increased by £70K but tax charges declined by £82K to give a loss for the period of £816K, a detrimental movement of £1.5M year on year.

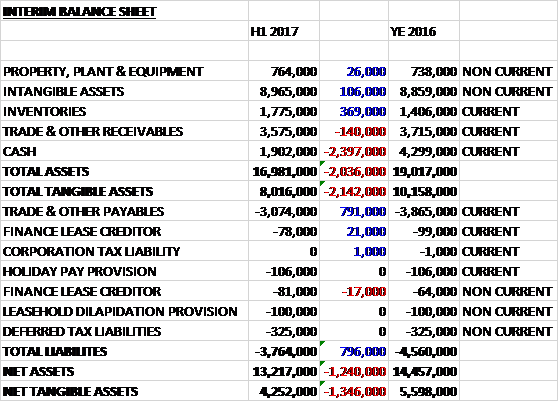

When compared to the end point of last year, total assets declined by £2M driven by a £2.4M reduction in cash, partially offset by a £369K growth in inventories. Total liabilities also declined due to a £791K fall in payables. The end result was a net tangible asset level of £4.3M, a decline of £1.3M over the past six months.

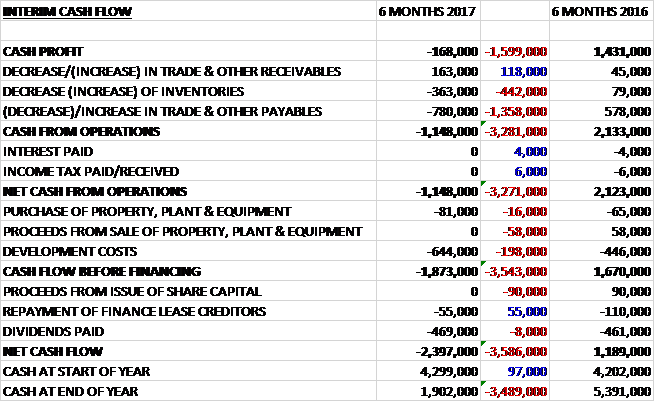

Before movements in working capital, cash losses saw a detrimental movement of £1.6M to -£168K. There was also a cash outflow from working capital compared to an inflow last time so the net cash outflow from operations came in at £1.1M, a detrimental movement of £3.3M year on year.

The group spent £644K on development costs and £81K on other capex so that before financing there was a cash outflow of £1.9M. After dividends were paid out too, there was a cash outflow of £2.4M and a cash level of £1.9M at the period-end.

Asset protection revenue was 39% lower, mainly as a result of the expected reduced contribution from sales of time-delay cash handling equipment to the Post Office which saw the sales of cash handling equipment fall 37%. Product division revenue was 31% lower. The lead up to the Brexit vote resulted in many customers putting plans on hold and afterwards there was the cancellation of planned work by several customers, including government departments, resulting in reduced orders. Sales were further reduced by the cancellation of a sales order for the supply of time delay cash handling equipment to a longstanding financial institution after they agreed to sell 300 of their high street branches.

Revenues from Eclipse Rising Screens were effected by reduced spending from two long standing financial institution customers. CounterShield revenue was lower as a result of a planned refurb programme for a large police force being delayed to the sale of their HQ. Sales of Fixed Glazing products were unchanged with increased competition from low cost counter suppliers.

Sales within the service division in the first six months have been challenging with the impact of branch closures that have occurred in the banking sector. Towards the end of the period, they embarked on the installation of their new TC105 rising screen activation system which the board expect to provide good revenue streams over the next few years, replacing the now obsolete TC104. Pneumatic upgrades continue as budgeted. Action to readdress resources within the division have been taken and overhead were reduced by 7%. The new field management software has now been bedded in and provides invoice capture and cash flow advantages. They continue to explore and develop their other product offerings and to reduce their reliance on rising screen revenue streams in the future.

In Access Control, revenues from SATEON continued the strong growth trend shown in previous periods, increasing 80% compared to the corresponding period last year. Much of this growth came through the upgrade of existing JANUS sites with many end users keen to continue long standing relationships with the group. Notable projects included Greater Manchester Fire Service and a major defence contractor.

JANUS revenues continued to decline in line with expectations as less new projects were completed. The product remains the platform of choice, however, for many end users and a major rollout continued for one of the world’s largest data centres. Significant investment was made developing SATEON version 3.0 software and SATEON Advanced Hardware, both of which were released at the begging of H2, later than originally anticipated. SATEON Advanced Hardware in particular is expected to become the majority Access Control revenue generator through the second half of the year and into next.

In workforce management development resources were focussed on the GT-10 employee terminal, released towards the end of the first half. GT-10 has an Android based operating platform, allowing current and potential software partners to integrate their web-based offerings seamlessly, where they have existing Android based apps. First launched at a US trade show, negotiations have started with several potential major workforce management software providers in the US, UK, Europe and Middle East. In addition to existing markets, GT-10 provides an opportunity to generate revenue in new markets and the group has begun research into several vertical sectors to investigate the potential return on investment available.

Sales of existing RS and IT series of WFM terminals continued in line with management expectations. The group has recently secured a new £350K contract with a steel producer for the supply of its IT31 WFM terminals. This order will be shipped in two tranches with £200K realised in the current year and £150K next year.

In North America, business development activities increased to leverage the potential that exists for growing WFM revenues. The directors consider that the US market remains the region with the fastest growing growth opportunities. For the first half WFM revenues grew 11% and a number of marketing initiatives are planned for the second half to increase brand awareness through the sales channel and into end-user markets.

The Hong Kong business saw revenues fall well short of expectations. As revenues were not forecast to significantly improve over the short to medium term a decision was taken to withdraw from the country during the period.

The shares are trading on a historic PE rating of 5.1 but this is likely to be much higher this year – I cannot find a forecast but the management state that they expect to make a loss this year. There is no interim dividend proposed, which is usually the case.

Overall then this has been a pretty terrible period for the group. They made a loss, net assets reduced and there was on operating cash outflow. The Asset protection division has a disastrous year as the wind down of the Post Office contract was not counteracted. The group are also blaming Brexit and the closure of bank branches. The latter is also affecting the Access Control division and shows no sign of getting any better as banking moves more and more online. This looks dangerous, I am not investing here for now.

On the 10th May the group announced that they had acquired an office in Poole. They have had a presence in Poole for over ten years but their current rented premises will not be available from this summer. They have therefore taken the decision to purchase a property in the area. The property will be acquired from LINSAR for a consideration of £1.2M which will be funded 30% from existing cash reserves and 70% from a bank loan.

On the 23rd May the group announced that it had entered into a development and commercial partnership with UniKey Technologies to develop its access control technology and provide new products.

On the 11th August the group announced that they have exchange contracts for the sale and leaseback of their new premises in Poole. The property was sold for £1.5M and will result in the group realising £360K after costs, refurbishment and repayment of the bank loan used to purchase the property. The lease arrangement is for 15 years with stipulated increases to the annual rental rate at the five and ten year anniversaries of the start of the contract.