Portmeirion has now released their interim results for the year ending 2018.

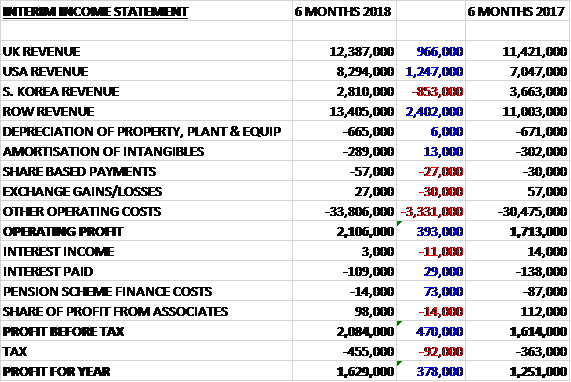

Revenues grew when compared to the first half of last year as an £853K decline in South Korean revenue was more than offset by a £1.3M increase in US revenue, a £966K growth in UK revenue and a £2.4M increase in ROW revenue. Operating costs also increased to give an operating profit £393K above last time. There was a modest decline in finance costs, mainly due to lower pension scheme costs but tax charges were up £92K which meant that the profit for the period was £1.6M, a growth of £378K year on year.

When compared to the end point of last year, total assets declined by £4.7M driven by a £3.8M fall in cash and a £3.4M decrease in receivables partially offset by a £2.9M growth in inventories. Total liabilities also declined due to a £991K decrease in borrowings, a £760K decline in payables and a £586K fall in the pension deficit. The end result was a net tangible asset level of £29.5M, a decline of £2M over the past six months.

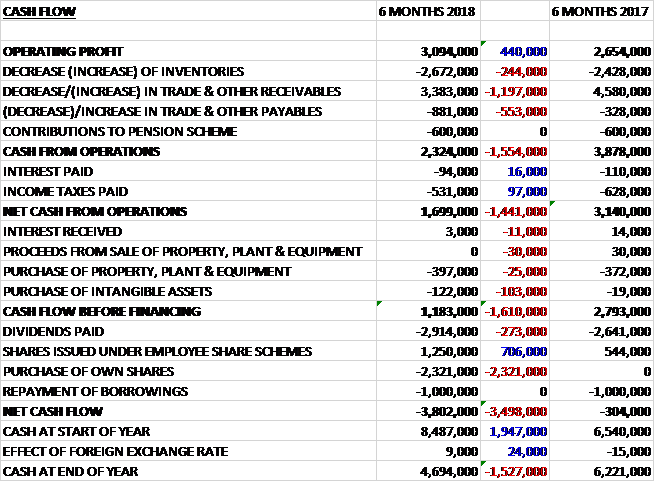

Before movements in working capital, cash profits increased by £440K to £3.1M. There was a cash outflow from working capital and even after tax payments reduced by £97K the net cash from operations was £1.7M, a decline of £1.4M year on year. The group spent £397K on tangible assets and £122K on intangibles to give a free cash flow of £1.2M. This did not cover the £2.9M paid out in dividends and the group also purchased a net £1.1M of their own shares, presumably to satisfy share schemes, and repaid £1M of loans to give a cash outflow of £3.8M and a cash level of £4.7M at the period-end.

The UK retail sector remains uncertain due to the ongoing Brexit negotiations and challenges in the high street. Despite this the group’s retail channel and e-commerce sales continue to grow driven by new product launches.

The US has seen a strong start to the year, delivering revenue growth of 29% at constant currency, although this reduced to 18% in Sterling terms. The retail environment in the US continues to change rapidly with sales moving from traditional channels to online. The board remain confident of prospects in the second half, driven by their ongoing development of the Spode Christmas tree range.

Sales in South Korea fell by 23%. This market remains under focus and the group are working closely with their distributor on expanding their product portfolio and targeting new customers. The board are confident of a recovery of a recovery in this market and expect second half sales to be in line with the prior year. Sales to the rest of the world showed the largest growth, increasing 22% to £13.4M. Sales into Europe continued to grow as well as their further penetration of Asian markets such as Taiwan and Hong Kong.

The UK business had a strong first half performance with a sales increase of nearly 9% driven by strong export sales to Asian markets and new product launches in the UK such as Sara Miller London and line extensions within Royal Worcester Wrendale Designs collection. Sales from the home fragrance division increased by 14% to £6.2M. The underlying performance of the Wax Lyrical business was pleasing with some new customer wins which was supplemented by further home fragrance sales penetration through the other distribution channels.

Going forward, the board remain confident in their ability to meet full year market expectations.

At the current share price the shares are trading on a PE ratio of 18.5 which falls to 16.6 on the full year consensus forecast. After an 8.1% increase in the interim dividend the shares are yielding 2.9% which increases to 3.1% on the full year forecast. At the period-end the group had a net debt position of £1.3M compared to net cash of £1.6M at the year-end due to the usual inventory build at this point.

Overall then this has been a solid period for the group. Profits increased and although the operating cash flow declined, this was due to working capital movements and cash profits were up. The free cash didn’t cover the dividend, however, and the net asset positon deteriorated slightly. The US and ROW markets are performing very well and the UK seems to be fairly decent. The problems lie in South Korea, which saw quite a drastic decline. This is apparently being addressed. With a forward PE of 16.6 and yield of 3.1% the shares are not cheap but this is a solid company and I am happy to hold.

On the 17th January the group released a trading update covering the year as a whole where they stated that they expect revenues to be at least £89.2M, ahead of market expectations driven by strong growth across the UK, US and South Korea. The home fragrance business continues to thrive, growing more than 11% and online sales growth was 20%. They also expect pre-tax profit to be ahead of market expectations.