President Energy have now released their interim results for the year ending 2019.

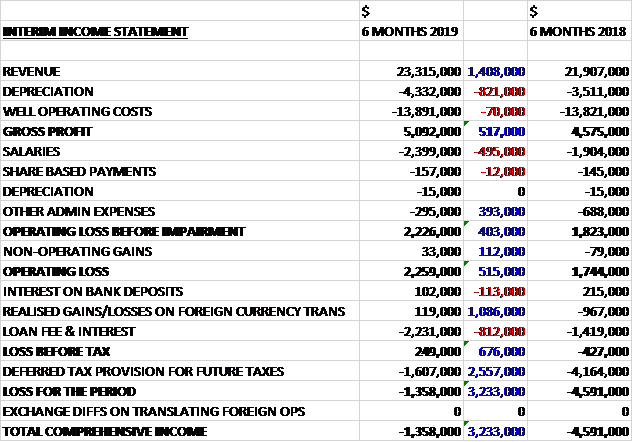

Revenues increased by $1.4M when compared to the first half of last year, depreciation was up $821K and other well operating costs increased by $70K to give a gross profit $517K higher. Salaries were up $495K but other admin expenses fell by $393K and non-operating gains increased by $112K which meant the operating profit increased by $515K. There was a $113K decline in bank interest received and interest paid increased by $812K, although there was a $1.1M positive swing to a gain on forex translation. Taking into account the $2.6M improvement in deferred tax provisions, the loss for the period came in at $1.4M, an improvement of $3.2M year on year.

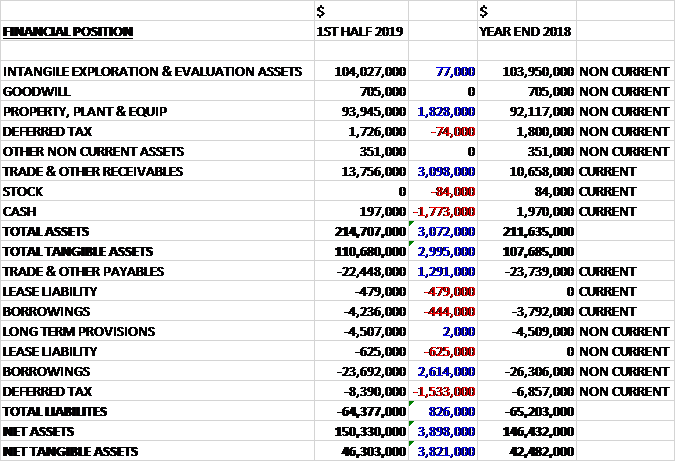

When compared to the end point of last year, total assets increased by $3.1M driven by a $3.1M growth in receivables and a $1.8M increase in property, plant and equipment, partially offset by a $1.8M decline in cash. Total liabilities declined during the period as a $1.5M increase in deferred tax liabilities was more than offset by a $2.2M decline in borrowings and a $1.3M fall in payables. The end result was a net tangible asset level of $46.3M, a growth of $3.8M over the past six months.

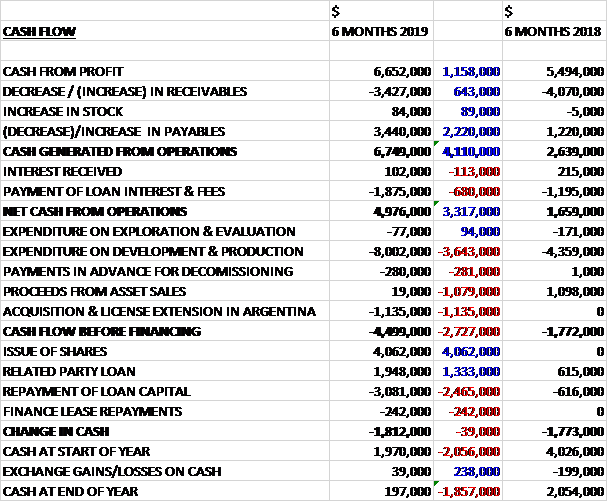

Before movements in working capital, cash profits increased by $1.2M to $6.7M. There was a small cash inflow from working capital but interest payments increased by $680K to give a net cash from operations of $5M, a growth of $3.3M year on year. The group spent $8M on development and production and $1.1M on licences in Argentina so that before financing there was a cash outflow of $4.5M. The group issued $4.1M of new shares, paid $242K in finance leases and paid back a net $1.1M of loans so there was a cash outflow of $1.8M and a cash level of $197K at the period-end.

There were a number of unforeseen headwinds during the period. In Argentina, a series of down-hole issues affecting some of the high impact production wells and electrical outages impacting average field performances in the Puesto Flores field on top of natural declines and in Louisiana there was flooding which resulted in the shutting-in of the entire production from all three wells for three months which also included the first part of H2.

In total ten workovers at the main Puesto Flores field were completed with the objective of stemming both the expected and unexpected losses in production and to make production less reliant on the relatively few high impact wells in the core Rio Negro province. Whilst these met with mixed success the learnings were valuable and the work was beginning to show positive signs towards the end of the period. The frac conducted in well PF0-16 was successful with production at double the pre-frac level. Further fracs will be effected in the field in due course.

In other work, the Puesto Prado field and associated facilities were recommissioned and placed into operation and the Las Bases gas facilities were tested and further sub-surface studies conducted in relation to the Paraguay assets. After the period-end a further eight workovers have been completed in Rio Negro with work currently continuing at the Puesto Flores field. The Estancia Vieja field and necessary facilities have now also been brought back into production after some eight years lying idle. Gas sales from that field will commence shortly. Elsewhere in Argentina, the Puesto Guardian field production remains stable.

Work has now also started on a brand new 16km section of steel pipeline to be laid between Puesto Prado and Las Bases, replacing the limited capacity pipeline between those points. This will enable a significant increase in gas sales in the new year with a projected additional 1,850 boepd in spring.

The presidential elections are due to take place in Argentia in October. In August the prelim elections took place, the result of which saw the Peronist Frente de Todos party securing 78% of the vote, a 16% margin over the Macri administration. The result was not anticipated which resulted in a significant fall in the Merval Index and the Peso/Dollar exchange rate. The fall in the currency has to a certain extent been corrected.

After the year-end there has been increasing volatility and falls in the Merval Index and USD:Peso exchange rate. In an aim to reduce pressure on consumers in the short-term, the Argentinian government passed a decree in August which fixes the price of crude oil and gasoline for 90 days. This sets a reference price of $59 per barrel. Additionally they imposed a fixed exchange rate of 49.30 pesos to the dollar.

With the exchange rate fixed at lower than the current rate of exchange, the decree is having an impact on the group due to the fact that all domestic oil sales contracts are paid in pesos. Therefore realised sales revenues in H2 will be lower than expected. It remains difficult to forecast where the domestic oil price will land after the end of the restrictions as well as the future of the temporary forex controls.

In Louisiana the wells have now been placed back in production after an extensive workover of the highest producing Triche well due to lower oil and gas and higher water flow. This and the historic flooding led to production falling by 42%. After the workover the well is delivering reduced production compared to pre-flood levels. This is down from 260 bopd at the start of the year to just 55 bopd. Whilst remaining profitable at these levels, the group is monitoring progress and considering further action and strategy regarding these assets. They are due to start drilling in Q4 at Jefferson Island where they have a 20% interest.

Whilst the macro circumstances in Argentina have been volatile of late, there have been early signs that stability is returning. All the presidential candidates acknowledge that the domestic hydrocarbon industry needs continued investment with satisfactory returns for investors.

Current net group production is 2,422 boepd with a further 250 due to be brought online from Rio Negro in October. The Rio Negro assets are contributing the most at 79% followed by Salta at 18% and the balance representing reduced production from Louisiana. The group remains operationally profitable and cash generative at the field level with profits in Argentina expected to be $3.5M in the second half. The next four months will see more growth from the group and the board expect to deliver from their existing well stock and additional 1,850 boepd in Spring.

Group well operating costs fell by 15% to $20 per boe and admin expenses fell by 13% to $6.40 per boe. In the period the group raised $4.1M by way of a placing of shares at 8p per share. The results for the full year are not currently expected to materially improve on 2018

The net group production for 2019 is now projected to be 2,600 boepd, up 13.5% on last year with the benefits from increased gas production only being felt from the end of the year once the building of the enlarged pipeline is completed. Internal projections for 2020 show an average in the range of 4,000 to 5,000 boped with a significantly increased proportion of gas from the Rio Negro assets.

At the current share price the shares are trading on a 2019 predicted PE ratio of 31.8.

On the 21st October the group announced the acquisition of an exploration contract in Rio Negro and the subscription of $1.8M of new shares by CGC.

Angostura is situated to the west of the group’s Las Bases concession and their pipeline passes through the SW corner of the area. It currently produces 50 bopd and 2.8MMscf of gas per day, representing in total around 500 boepd so will increase the group’s daily production by 10%. All the gas is currently compressed within Angosturam sent by pipeline to the group’s Las Bases facility and conveyed by their pipeline to offtakers. The oil will be taken by truck to Las Bases and added to their existing production.

The first period of the exploration contract extends until November but they are entitled to request access to a second exploration period, with a royalty of 15% over volumes produced during this phase. In the event that the exploration contract is converted into an exploitation concession of 25 years, the royalty is reduced to 12% and the province’s energy company will take a 20% interest.

CGC has agreed on completion of the acquisition to invest $1.8M in the group by way of a subscription.

On the 1st November the group released an update. They announced that they are now ready to flow gas through their own 60km pipeline from their Estancia Vieja and Las Bases fields. From the start of November, 30,000m3 per day of their own gas will be piped by this route to market with the volume currently restricted by a bottleneck in a 16km stretch of pipeline due to it being a 3” flexible temporary plastic pipe.

Next week they will commence to build a 6” steel pipeline to replace this section. The work is due to be completed in January. When finished, gas deliveries will be ramped up as more wells will be opened up on a stage by stage basis.

Since the last announcement the 75 boepd production from Louisiana has increased to 275 boped as the Triche well has staged a recovery with currently a gross 220 bopd being sold. In Argentina it was announced that oil prices payable to producers will increase by 5% with effect from now. Which is a start.

Overall then this has been a bit of a difficult period for the group. Losses did improve, the net asset level increased and the operating cash flow improved but the group still produced no free cash and I am starting to wonder whether they will ever actually be cash generative. The issues are the poor performance of the workovers, the floods in Louisiana and the political situation in Argentina. Given the issues in Argentina it is especially disappointing to see the US assets performing badly. There is still potential here but the group seems unable to realise it and the forward PE of 31.8 looks expensive.

On the 14th November the group announced that the decree limiting prices for oil producers in Argentina has now expired and prices have returned to normal. It has not yet been replaced which means an immediate increase of around $9 per barrel to around $53 per barrel. It is unclear as to how long this will last.

On the 20th November the group announced the acquisition of the Angostura exploration contract has been completed along with the subscription for $1.8M of new shares.

On the 3rd February the group released a full year trading update. The group had turnover of $41M, $6M lower than last year with average realisation price in Argentina 19% down. Average production of 2,414 was 6% up on 2018 and the group made an adjusted EBITDA of $12M, $5M lower.

First oil was produced from the Estancia Vieja field with the field facilities in Puesto Prado and the gas plant in Las Bases re-commissioned. First gas was transported from the Estancia Vieja field to market through the group’s pipelines. At the end of the year the producing Angostura field was purchased but this came too late to have a material impact on results, although it is now contributing profitably.

The challenges encountered included unplanned downtime in key producing wells and electricity supply outages in Rio Negro, a three month shutdown in Louisiana and the effects of the temporary Decree 566 in Argentina which reduced oil prices by almost 25% for three months. Consequently margins were squeezed. The results were further impacted by lower oil prices which was reflected in average group sales prices declining to $49.6, down nearly 17% with Argentina down 19% to $49.90.

As a result of the above factors the group suspended drilling activity in Argentina.

The current year has got off to a good and profitable start with January showing a material improvement over H2 2019. Trafigura has consolidated its position as an active partner by coming on board as a significant shareholder with group debt reduced by $69M to $15M. The temporary Decree 566 lapsed in December and therefore the group is preparing to drill three new wells in Rio Negro with the first expected to be spudded by the end of the first half. Additionally with Louisiana production largely restored they expect to drill in Jefferson Island during H1. A further six wells are targeted to be drilled across their assets later in the year, of which two are exploratory.

The construction of the new gas pipeline between Estancia Vieja and Las Bases in Rio Negro has now been completed on time and budget and should be commissioned by the end of the month. Group production will be supplemented by gas flowing through that enlarged pipeline where they expect by the end of February, gas deliveries to market of around 1,000 boepd with a target of 1,500 boepd by the end of the first half of the year. The acquired Angostura exploration block is expected to make a contribution of some 600 boepd by mid-February.

The group is cautiously optimistic that the macro environment in Argentina has calmed and that they may see beneficial developments during the year. The group repeats their guidance for 2020 of average production in excess of 4,000 boepd.