QinetiQ has now released their final results for the year ended 2017.

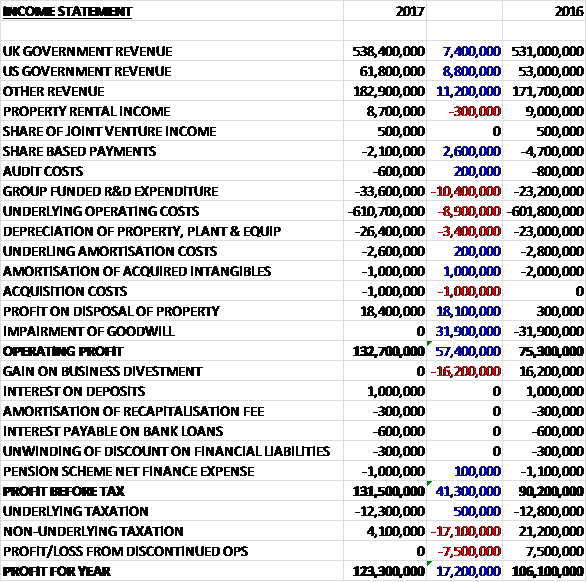

Revenues increased when compared to last year as a £300K decline in property rentals was more than offset by an £8.8M growth in US government revenue, a £7.4M increase in UK government revenue and an £11.2M increase in other revenues. Share based payments fell by £2.6M but group funded R&D exposure increased by £10.4M and other underlying operating expenses grew by £8.9M. Depreciation was also up £3.4M and there was £1M of acquisition expenses but the amortisation of acquired intangibles declined by £1M, there was an £18.1M increase in the profit on property disposals and there was no goodwill impairments which accounted for £31.9M last year. All of this meant that the operating profit grew by £57.4M. Conversely there was no gain on business divestments which brought in £16.2M in 2016, non-underlying tax income declined by £17.1M and there was no profit from the discontinued operations, which was £7.5M last time. Profits overall increased by £17.2M.

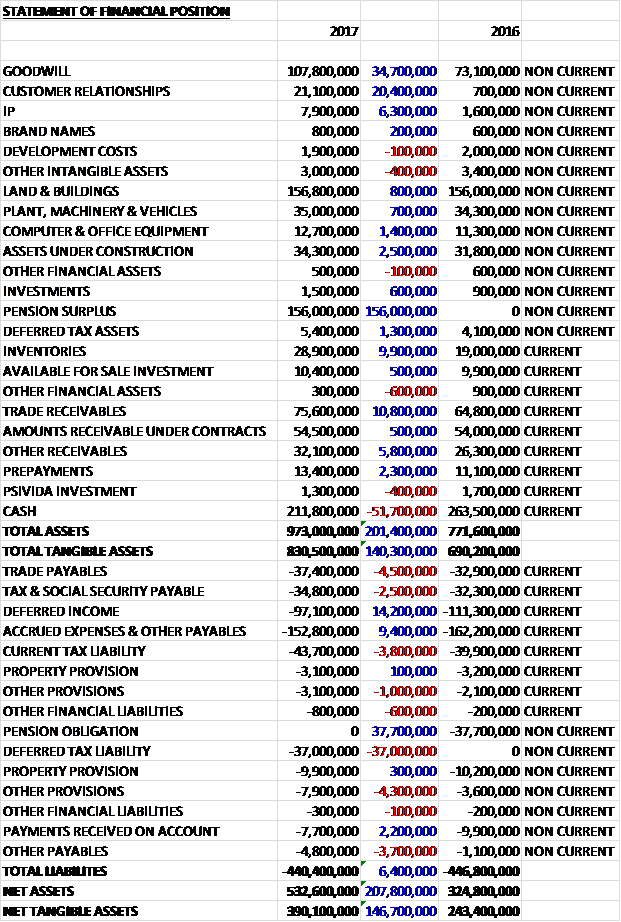

When compared to the end point of last year total assets increased by £201.4M, driven by a £156M pension surplus due to the performance of interest rate hedges, a £34.7M growth in goodwill, a £20.4M increase in customer relationships, a £10.8M growth in trade receivables, a £9.9M increase in inventories, a £6.3M increase in the value of IP, and a £5.8M growth in other receivables, partially offset by a £51.7M decline in cash. Total liabilities declined during the year as the £37.7M decline in the pension surplus, a £14.2M fall in deferred income and a £9.4M fall in accrued expenses and other payables was partially offset by a £37M increase in deferred tax liabilities, a £4.5M growth in trade payables and a £4.3M increase in other provisions. The end result was a net tangible asset level of £390.1M, a growth of £146.7M year on year.

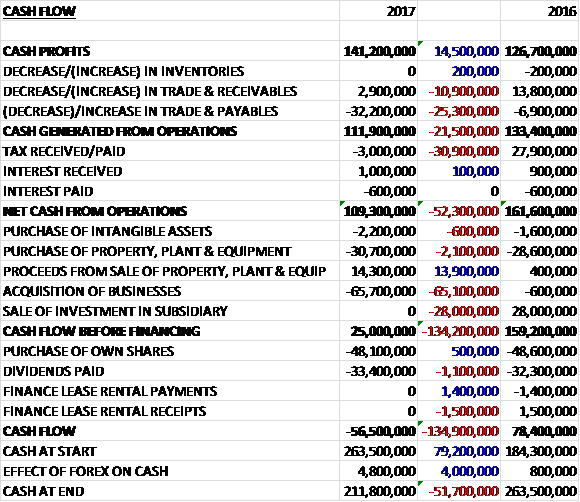

Before movements in working capital, cash profits increased by £14.5M to £141.2M. There was a cash outflow from working capital due to a decrease in payables and after tax swung to a charge, a detrimental movement of £30.9M, the net cash from operations came in at £109.3M, a decline of £52.3M year on year. The group spent £30.7M on property, plant and equipment, £2.2M on intangibles and £65.7M on acquisitions but received £14.3M on the sale of some property which gave a free cash flow of £25M. This did not cover the returns to shareholders, however, with a £33.4M dividend payment and £48.1M of share re-purchases meaning there was a cash outflow of £56.5M and a cash level of £211.8M at the year-end.

Excluding exchange rate changes, the £1.2M contribution from acquired businesses and last year’s profit from divested businesses, the organic constant currency operating profit increased by £3.4M to £112.6M.

The underlying operating profit in the EMEA Services division was £92.7M, a decline of £1.1M year on year despite being boosted by a £5.2M credit relating to the release of engine servicing obligations as they invest in new aircraft for test aircrew training (there was a £3M credit last year). Excluding those, and the effect of forex and acquisitions, underlying operating profit fell by £4.6M mainly due to the lower baseline profit rate for single source contracts. Revenues were flat as the impact of the RubiKon acquisition and favourable forex movements were largely offset by last year’s disposal.

Orders, excluding the £1BN LTPA amendment, grew 5% to £520.9M including the award of a £109M 11 year renewal from the MOD for the Naval Combat system Integration Support Services and an £80M of additional orders added to the Air Strategic Enterprise contract. The £1BN amendment to the LTPA signed during the year has significantly increased total EMEA services backlog. The remaining LTPA contract is due to be repriced in March.

As anticipated, the baseline profit rate for new and renewed single source contracts signed in 2018 will fall by 149 basis points from the 2017 baseline rate. Including the LTPA contract, 76% of the division’s revenue is derived from these contracts.

Within Air and Space, the Strategic Enterprise model for aircraft engineering services has now been in place for a year and £80M of additional contracts were added to the model during the year to provide in-service support for eight aircraft including the Apache, Puma and Merlin helicopters and Tornado fast jets, as well as test and evaluation services for the Wildcat Future Air to Surface Guided weapon programme.

The business is focused on the modernisation of test aircrew training provided by the Empire Test Pilots School which achieved approved training organisation status during the year allowing it to train civil test pilots. Investment in new aircraft and a revised syllabus will allow it to pursue opportunities for growth. During the year Boeing Defence UK identified MOD Boscombe Down which the group operate and manage on behalf of the MOD, as the preferred site for its future UK HQ and European hub for maintenance, repair and overhaul.

The business’ relationship with the ESA continues with their transceiver operating as part of the ExoMars mission to Mars, despite the lander on which it was mounted being lost. They are continuing to deploy significant resources to develop the gridded ion engine electric propulsion system for the flight module to be used on ESA’s mission to Mercury which is due to launch in October 2018.

They secured £2M of research funding to lead a team to upgrade the scale models used in the Farnborough wind tunnel using technology adapted from F1, leading to improved efficiency and increased capacity and they entered into a teaming agreement with Thales and Textron to provide an offer to the MOD for thee Air Support to Defence Operational Training programme.

In Maritime, Land and Weapons, the business delivered the trial of the new Spear 3 missile system planned for the UK’s F-35 Lightning II stealth fighter aircraft. They also secured an 11 year contract extension worth £109M for the Naval Combat Systems Integration and Support services. Later in the year the site hosted the Royal Navy’s Information Warrior exercise designed to develop and test new information warfare capabilities. The business is a member of a UK industrial consortium called Dragonfire which won a £30M contract for a Capability Demonstrator programme for laser technology. The demo is reliant on a QinetiQ-developed technology. They also won an £8M contract to implement and evaluate vehicle survivability for Sdtl, including installing a soft-kill defensive aids system on a Challenger 2 tank along with a £5M contract to deliver a real time simulation system for the Sentry E-3D aircraft to enable effective operations with NATO countries.

Within Cyber, Information and Training, the business won a £10M contract to link existing Typhoon synthetic training at RAF bases to the facility at RAF Waddington and delivered a cyber range for an army exercise as part of a growing capability to support customers in the test and evaluation of cyber operations. The business delivered their stand-off threat detection system to the US Transportation Security Administration for use at several high-profile events including the Presidential inauguration.

During the year the business secured contracts totalling £10M for secured navigation, working with European and UK government customers to enable the effective exploitation by users of the Galileo constellation of satellites which goes live in 2021. This included the first demonstration of accessing the encrypted Public Regulated Service in real-life applications. The business has built on this by agreeing a partnership to go to market with Rockwell Collins around the world.

Following the acquisition of RubiKon, the Australian business continued to develop its core capabilities, extending contracts for the provision of integrated engineering services at the Defence Science and Technology group’s Fisherman’s Bend workshop in Melbourne, and for aircraft structural integrity services. They also signed a new strategic support partnering contract for the replacement of the AP-3C Orion fleet with a combination of unmanned and manned aircraft. The Australian business also grew order intake, including contracts to support tanker aircraft, navy guided weapons systems, ground-based air defence and the Australian Artillery Regiment.

The Canadian business achieved its first home win with a contract to provide advice to the Royal Canadian Coast guard and a new office is being established in Malaysia to support sales and marketing in the region. Overall the revenue under contract for 2018 is in line with last year and the division is expected to deliver modest revenue growth this year but the lower baseline profit rate for single source contracts represents a headwind for operating margins.

The underlying operating profit in the Global Products division was £23.6M, a growth of £8.5M when compared to last year which included the impact of the acquisition of Meggitt Target Systems, favourable forex movements and £2.2M of credits relating to historical overseas contractual disputes. With these items removed, underlying operating profit increased by £3.6M driven by QNA and OptaSense. Organic constant currency revenues grew by 8% due to a strong performance in QNA, driven by product shipments relating to the new US aircraft carriers, together with growth in OptaSense. Orders reduced by £10M to £154.4M as a result of a strong comparative year which included a large pipeline contract in OptaSense and a five year £10M contract to provide materials research and advice to the MOD. Order flow in North America was strong including $41M of aircraft carrier orders during the year.

In North America, QNA delivered very good orders and revenue performance driven by the strength of their US military robot business, sales of aircraft armour and their continued role supporting the next generation of US aircraft carriers. In total the business was awarded more than $40M of orders for unmanned ground vehicles for the reset of robots previously used in operations for capability upgrades such as detection of CBRNE. The business is bidding for multi-year programmes of record that are under way now or will be under way this year. These will be funded out of the DOD’s base budget for TALON-class and Dragon Runner class systems.

In October they announced a partnership with Estonian company Milrem for Titan, a modular, hybrid military unmanned ground vehicle for dismounted troop support. QNA also confirmed a $41M contract with General Atomics which follows the initial $16M announced in 2015. The business will deliver control hardware and software for the Electromagnetic Aircraft Launch System to be installed on the next aircraft carrier.

In September the business launched a new meteorological sensing product that provides real-time atmospheric data in support of military requirements such as artillery fire support, tactical weather modelling and air drop. The Line Watch product which measures the current and voltage of power distribution lines is being piloted by ten utility companies following the delivery of the first production unit.

In international markets, robots, vehicle protection, and soldier protection systems remain relevant as security challenges and instability persists in the Middle East and elsewhere. In addition to product sales the business is building its base of contract R&D projects to drive technology development, explore new customer problems and expand its competitive offerings. Progress continues with awards for an airborne wind profiling radar, robotic enhancement projects, a turbine-based power and thermal management system and a number of other commercial research and development projects.

The OptaSense business grew last year, driven principally by strength in its pipeline sensing business and some recovery in the North American oil and gas market. They are delivering the system for the world’s largest distributed fibre sensing project for the 1,850km Trans-Anatolian Natural Gas Pipeline that runs from Azerbaijan to Europe. The business has also signed an agreement to work with Siemens to pursue new opportunities in the rail sector.

Additionally, the business is undertaking collaborative research with Stanford School of Earth, Energy and Environmental Sciences in California that includes the installation of a fibre-optic seismic array on the Stanford campus to better understand the complex geology of the Bay Area.

Within Space Products the business secured a €2M contract with the ESA to develop the next generation computer and power management system for their PROBA family of satellites in addition to other developing funding. Their P200 satellite was also listed in the NASA catalogue which will help facilitate the procurement of spacecraft by US federal agencies and their affiliates. Under contracts awarded during the year the business supported the development of a spacecraft for the Argentinian space programme and a satellite for a joint European and Chinese solar wind programme. They also secured funding to continue the development of their International Berthing and Docking mechanism for spacecraft.

Within EMEA products, the group acquired target systems business secured an early contract win in the UAE and completed their first commercial flight of the Banshee Jet 110 aerial target. During the year DARPA invested a further $3M in the group’s electric hub drive technology that will improve mobility and survivability of future military ground vehicles. The new agreement builds on previous contract awards and will take the technology from concept design to the building and testing phase including the production of two fully working units. Boldon James further expanded their product portfolio with the introduction of several new enhancements to their data classification offering.

Going forward, as a result of their contracted orders and pipeline of opportunities, as well as the expected full year contribution from the Target Systems acquisition, the division is expected to continue to grow in 2018.

One major development in the year was the signing of an 11 year £1BN amendment to the LTPA. The focus in 2018 is to re-price the remaining LTPA contract which is due in March and to work with the MOD to develop a long-term vision for the UK’s testing capabilities. This will provide a platform for growth in the UK T&E market which the group estimate to be double that which they currently access, and improve their ability to win work with customers outside the UK.

In December the group acquired Meggitt Target Systems for £60.3M. The business is a provider of unmanned aerial, naval and land-based target systems and services for test and evaluation and operational training and rehearsal. They provide systems to about 40 countries with operations in Canada and the UK. The acquisition generated £24.5M in goodwill and operating profit of £1M since acquisition. In January the group acquired RubiKon for £7.4M. The business provides solutions to complex logistics, supply chain management and procurement projects in defence, aerospace, mining and government markets in Australia. The acquisition generated goodwill of £3.9M and operating profit of £200K since acquisition.

Going forward, in EMEA services, revenue under contract is in line with the prior year and the division is expected to deliver modest revenue growth this year but the lower baseline profit rate for single source contracts represents a continued headwind for operating margins. The group’s global products division has shorter order cycles and is dependent on the timing of shipments of key orders but as a result of their contracted orders and pipeline of opportunities, as well as a full year contribution from the Target Systems acquisition, the division is expected to continue to grow in 2018.

Cash flow will reflect increasing investment with capex of £80M to £100M to support the amendment to the LTPA agreement compared to £33M this year but overall for 2018 the board are maintaining expectations for steady progress excluding the non-recurring benefits of 2017.

At the current share price the shares are trading on a PE ratio of 15.7 which increases to 16.1 on next year’s consensus forecast. After a 5% increase in the dividends, the shares are yielding 2.2% which increases to 2.4% on next year’s forecast. At the year-end the group had a net cash position of £221.9M compared to £274.5M at the end of last year.

Overall then this was a solid performance. Profits increased, net assets were up due to the good performance of the pension scheme, but the operating cash flow fell. This was due to working capital movements, however, and the cash profits increased. The free cash flow was not enough to cover the dividends and the increased capex next year suggests this is something that will continue. The EMEA Services division saw profits decline due to the lower baseline profit rate for the single source contracts. Orders were good but there will be a further headwind with more reductions in the baseline profit rate for single source contracts so it seems unlikely the division will grow profits in 2018. Global products performed well due to orders relating to the new US aircraft carriers for QNA and continued pipeline sensing business for OptaSence following a modest pick-up in the oil and gas market.

Going forward EMEA Services look as though they might drag on results but despite lower orders, the Global Products division is expected to grow, aided by the Meggitt acquisition. The shares are not particularly cheap with a forward PE of 16.1 and yield of 2.4% but there is plenty of net cash here and this is a strong, steady company. I am inclined to continue to hold.

On the 21st June the group announced that CFO David Smith purchased 17,416 shares at a value of just under £50K.

On the 13th July the group announced that CEO Steve Wadey purchased 15,000 shares at a value of £39K. This is nice to see, but not a huge buy.

On the 19th July the group released a trading update covering Q1. In the EMEA Services division, Q1 revenue under contract is similar to the position a year ago but orders have been slower than expected with some customer contract award decisions being deferred or delayed. Despite the somewhat slower start to the year for orders, the board continue to expect the division to deliver modest revenue growth this year. The lower baseline profit rate for single source contracts continues to represent a headwind for operating margins.

Revenue performance in Global Products during the quarter was similar to last year but the board expect the division to grow in 2018 as a result of their contracted orders and pipeline of opportunities, as well as the anticipated full year contribution from the recent acquisition. Overall they are reaffirming the previous outlook and expect steady progress in 2018, supported by revenue growth.

All this is OK but it seems to me that a lot more of the growth is being pushed back and there must be a risk that it doesn’t come. Growth here is sluggish at best and despite the solid, high quality nature of the company I remain on the side lines. The valuation is starting to look rather interesting, however, so I am keeping a keen eye on this company.

There have been a number of recent director share purchases. On the 21st July non-executive director Michael Harper purchased 5,000 shares at a value of £12K; Chairman Mark Elliott purchased 20,000 shares at $62K; and CEO Steve Wadey purchased 15,000 shares at £36K.

On the 8th September it was announced that CFO David Smith purchased 8,936 shares at a value of just under £20K.

On the 21st September it was announced that non-executive director Susan Searle purchased 7,500 shares at a value of £17K.

On the 29th September the group released a trading update covering the first half of the year where hey stated that trading had been in line with expectations and the outlook for overall group performance this year is unchanged.

The EMEA services division started the year in a strong position. Following stronger order intake in Q2, the revenue for the year under contract is as expected and the board reiterate their guidance for modest growth in revenue in 2018. The Global products division has been trading in line with expectations during the first half. As a result of its contracted orders and pipeline of opportunities, as well as the expected full year contribution from Target Systems, the division is expected to grow this year.

In the UK home market, they secured an £8M order from the MOD to provide naval combat systems expertise for Type 26 Global Combat Ship added to the £110M eleven year Naval Combat System Integration Support Services contract agreed last year; and an order from Boeing, worth approximately £25M, to continue to deliver wind tunnel testing for their commercial aircraft development until 2024.

In their US and Australian home markets, they were awarded a significant order for aircraft launch and recovery equipment for the new class of US Navy aircraft carriers; and an A$8M order to manage mine warfare maintenance facilities at HMAS Waterhen for the Australian DoD.

Overall this seems like a steady update and I am tempted to jump back in there at the lower share price.