Red24 has now released its final results for the year ending 2015.

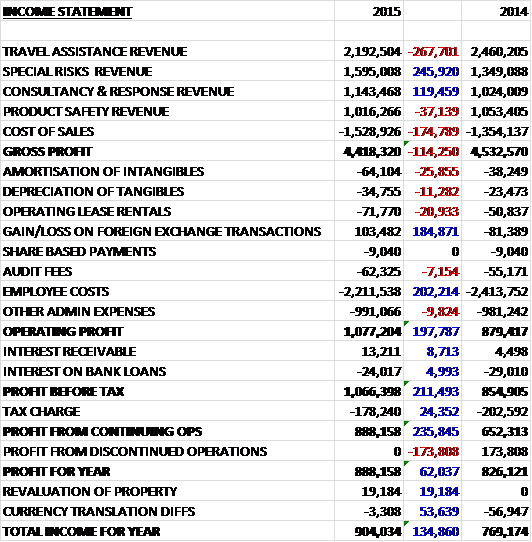

Overall, revenues increases somewhat year on year as declines in travel assistance and product safety were offset by increases in special risks and consultancy & response. Falls in revenues from the UK and Europe were offset by an increase in ROW sales. Cost of sales also increased, however, to give a gross profit some £114K lower than last year. We then see a fall in employee costs, partially offset by small increases in depreciation, amortising and operating lease rentals before a £185K positive swing in foreign exchange transactions sent the operating profit £198K higher than in 2014. There were then small improvements in interest costs and a smaller tax bill (due to the fact that R&D investment in the travel tracker product attracted a tax credit in the UK) offset by the lack of a £174K profit from the discontinued operation to give a profit for the year of £888K, an increase of £62K year on year.

When compared to the end point last year, total assets increased by £808K driven by a £1.1M increase in cash and a £152K growth in the value of intellectual property, partially offset by a £204K fall in trade receivables and a £118K decline in prepayments and accrued income. Total liabilities also increased during the year, mainly as a result of the £219K growth in accruals and deferred income relating to obligations for future services that have already been invoiced. The end result is a £569K growth in net assets to £4.1M (excluding goodwill). Operating leases were negligible and declining so this balance sheet looks rather solid.

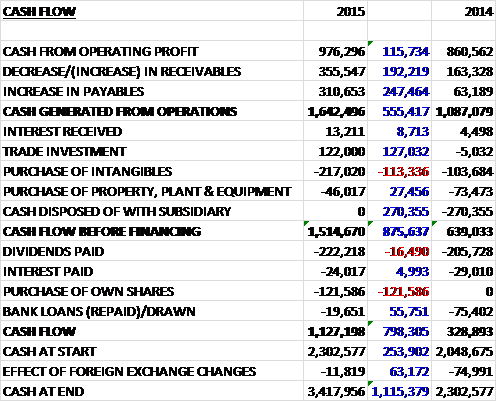

Before movements in working capital, cash profits increased by £116K to £976K which became an improvement of £555K to £1.6M after the group increased the number of days it takes to pay its creditors from 19 days to 26. Capital expenditure was minimal, with a £217K purchase of intangible assets and £46K going on property, plant and equipment and the free cash flow was further flattered by the £122K received from the sale of a portion of the Linx investment. Indeed, before financing, the cash flow stood at an impressive £1.5M. Of this, some £222K was spent on dividends and £122K on the purchase of shares to use for employee schemes so that for the year as a whole there was an impressive £1.1M of cash coming into the business, some £798K better than last year.

Gross profit at the Travel Assistance division fell by £111K to £2.2M. The service was significantly enhanced the investment in the travel tracker product which has placed it onto a new technical platform that will make it easier to interface with new clients. The product was launched in February 2015 and the initial response has been encouraging. The previously announced loss of the HSBC Premier and Advance books in the UK impacted revenues in the current year and although significant progress was made in diversifying revenue streams, regulatory changes in the UK make it unlikely that the lost revenues will be replaced by like for like income so the cost base was reduced.

Gross profit at the Special Risks division grew by £153K to £1.2M. The business had a busy year and dealt with a record number of kidnappings and other attempts at extortion with Mexico and Indonesia proving particular trouble spots. The prolonged incident that occurred last year in the Middle East was not repeated but the group has added new books of business over the year. The new Munich office is meeting expectations and has created a number of promising opportunities.

Gross profit at the Consultancy & Response division fell by £94K to £363K. The business has been busy with requests for close protection work and for evacuation planning services. In August a Far Eastern client requested a large evacuation from Libya involving several hundred members of staff which was successfully completed and represented the largest operation to date. Gross profit at the Product Safety division fell by £62K to £682K. The division did show an increase in revenue during the second half of the year following the launch of a new analytical tool and new training modules which kept the group’s offering ahead of the competition and helped ensure that contracts are renewed and new business won.

Given the loss of the largest customer these results are actually very good. The group seems to have responded swiftly to the news by reducing their fixed cost base and winning new contracts. Two clients still account for more than 10% of revenues, however with both account for about 14% compared to 23% and 10% last year. This is to be expected for a company of this size but it is still a considerable risk and one that the group is trying hard to resolve. The group does also seem to be suffering from a high level of receivable impairments. Of the total amount of £717K some £44K was impaired during the year, which is more than 6%. After this impairment, the amount of receivables overdue has fallen significantly however, so hopefully this is a one-off occurrence.

Another potentially serious risk is that of currency differences. A 10% appreciation of the South African Rand against Sterling would increase the cost of its operations in the country by £148K, although this would be mitigated somewhat by a corresponding £116K rise in the value of their Rand assets. Were the US dollar to appreciate by 10% against Sterling, profits would be reduced by £84K. These may not sound like huge amounts but they are fairly material to a company of this size. In order to try and counteract some of this risk, the group has forward purchased 80% of their forecasted Rand requirements.

During the year the group received £122K from the sale of a portion of their Linx investment. They have agreed to sell their entire holding which will bring in £125K in 2015 and the same amount in 2016. The KPIs of the group are all financial in nature and include revenue, gross profit, profit before tax, EPS and available cash. All of them except gross profit improved year on year. This year the group appointed Lorraine Adlam as non-executive director. She was previously CEO of a Lloyd’s Underwriting business and Chairman of Howden Insurance Brokers so she sounds like she might be a useful person to have on the board given that insurance companies must make up a decent portion of the client base.

Going forward, although there are risks to the business mainly relating to their continued (but improving) over-reliance on some large customers, foreign exchange risks and the general global economic outlook, the board are encouraged by the progress over the last year and are confident of further progress to come. The acquisition made after the balance sheet date added a number of blue chip clients to the group’s books and strengthened their presence in Asia along with broadening the product offering in the UK. There is apparently a good pipeline of new business and significant opportunities are seen in Europe and Asia.

At the current share price the shares trade on a P/E ratio of 11.4 which falls to 9.4 on next year’s consensus forecast which looks pretty decent value to me. After a 17% increase in the final dividend, the dividend yield currently stands at 2.4% increasing to 2.9% next year which again seems pretty good. At the end point of the year, the group enjoyed a net cash position of £3.2M compared to £2M at the end of last year so they clearly had enough to pay for the acquisition announced recently.

Overall then, this is a very encouraging updates. Profits improved slightly, net assets increased in what was already a solid balance sheet and operational cash flow improved, albeit slightly flattered by good working capital movements, to give a very strong free cash flow. Operationally, the travel assist business did remarkably well considering the loss of the HSBC contract and the special risks division had a strong year due to record numbers of kidnappings! The consultancy & response, along with the product safety divisions both saw profits fall although revenues picked up for the latter business in the second half of the year.

As with any business there are risks, though, and especially so in one as small as this. The group still relies on a number of large customers, although this is an area that is much improved year on year. The large amount of impaired receivables will hopefully be an area of focus and the currency issues, at least as far as the more volatile Rand is concerned, seem to be being addressed but strong shifts in the USD and GBP exchange rates could still cause problems. The forward P/E is under 10 though, there is a near 3% dividend yield expected for next year and the group has a strong net cash position. This is the kind of business I like – they make enough free cash to be able to fund their own expansion both organically and through acquisitions. I am currently comfortable with my investment here.

As you can see the shares have pretty much entirely recovered from their shock after the loss of the HSBC contract.

On the 6th July the group announced that a company indirectly owned by Chairman Simon Richards sold 240,000 shares at a total value of £63.6K. Mr. Richards still owns some 14,219,250 shares representing over 29% of the total equity but this is likely to put a bit of a halt on the share price appreciation in the short term.

On the 20th July the group announced that the same company as above, indirectly owned by the Chairman sold its remaining 200,000 shares at a value of £58.5K. Mr. Richards still owns 14,019,250 shares representing 28.62% of the total issued share capital so he is still heavily invested.

On the 28th August the group released a statement that non-executive director Lorraine Adlam had purchased 25,000 shares at a value of £6,575 which gives her a total of 75,000 shares. This is not exactly a huge vote of confidence but nicer than nothing!