Redrow has now released their interim results for the year ending 2018.

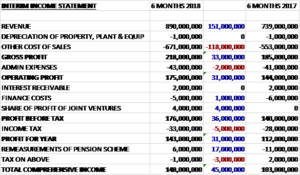

Revenues increased by £151M when compared to the first half of last year and with cost of sales up £118M the gross profit increased by £33M. Admin expenses were up £31M to give an operating profit £31M higher. Finance costs fell by £1M and there was a £4M profit from joint ventures but this was offset by a £5M growth in tax charges to give a profit for the year of £143M, a growth of £31M year on year.

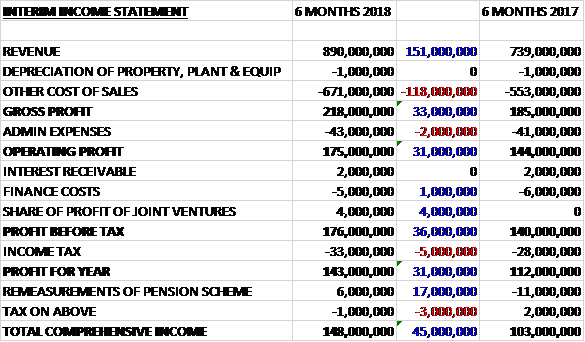

When compared to the end point of last year, total assets increased by £89M, driven by a £64M growth in land for development, a £41M increase in work in progress and a £6M growth in show home stocks, partially offset by a £13M decrease in cash and an £8M fall in joint venture investments. Total liabilities declined during the period as a £31M increase in land creditors was more than offset by a £51M fall in bank loans. The end result was a net tangible asset level of £1.341BN, a growth of £108M over the past six months.

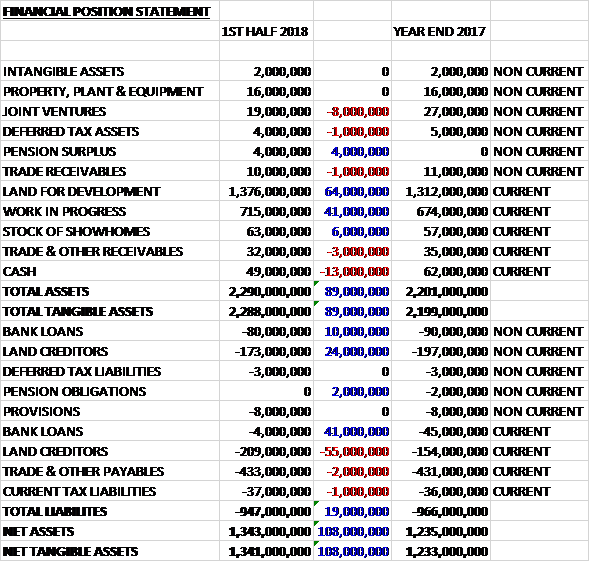

Before movements in working capital, cash profits increased by £31M to £174M. There was a cash outflow from working capital and after tax payments fell by £6M the net cash from operations was £64M, a decline of £41M year on year. The group received £13M from joint ventures and £3M from interest and only spent £1M on capex to give a free cash flow of £79M. Of this, £10M was used to repay loans and £41M on dividends to give a cash flow of £28M and a cash level of £45M at the period-end.

During the period legal completions increased by 14% to 2,811. Group revenue rose by 20% due to the increase in completions, including the first 82 apartments at Colindale Gardens. There was also a 9% rise in the average selling price to £330K, mainly due to the growth in the Southern business. Demand for new homes remained robust with good availability of mortgages at competitive rates. The value of private reservations in the period grew by 10% on a like for like basis and the total order book at the end of December was 5% ahead of the prior year at £1.05BN.

During the period the group added 4,315 plots to their current land holdings, 583 of which were transferred from forward land. There was a net increase of 1,500 plots in the current land holdings and the forward land bank increased by 5,400 plots to 31,800.

Going forward, the group are entering the second half of the year with an order book comfortably in excess of £1BN. Reservations in the first five weeks have been in line with the strong comparable last year and given the strength of the order book and land holdings, together with the robust sales market, the growth strategy remains on track.

At the current share price the shares are trading on a PE ratio of 8.3 which falls to 7.1 on the full year forecast. After a 50% increase in the interim dividend the shares are yielding 3.5% which increases to 4.3% on the full year forecast. At the period-end the group had a net debt position of £35M compared to £73M at the end of last year.

On the 20th February the group announced that director Matthew Pratt sold 9,000 shares at a value of £54K.

Overall then the group has made further progress in the period. Profits were up, net assets increased and although the operating cash flow declined this was due to an increase in inventories and cash profits increased with a good amount of free cash being generated. The improved performance is mainly down to an increase in completions with a small increase in average price of home sold due to differing mix, so it seems that the prices have stagnated somewhat. Still, with a forward PE of 7.1 and yield of 4.3% these shares still look decent value to me.