Swallowfield has now released their interim results for the year ending 2018.

Revenue increased by £254K when compared to the first half of last year as a £2.2M decline in manufacturing revenue was more than offset by a £2.5M growth in brand revenue. Cost of sales declined by £252K to give a gross profit £506K higher. Admin costs were up £49K but acquisition costs were down £343K to give an operating profit £776K higher. There was a modest increase in finance costs and tax charges increased by £134K to give a profit for the period of £2.2M, a growth of £569K year on year.

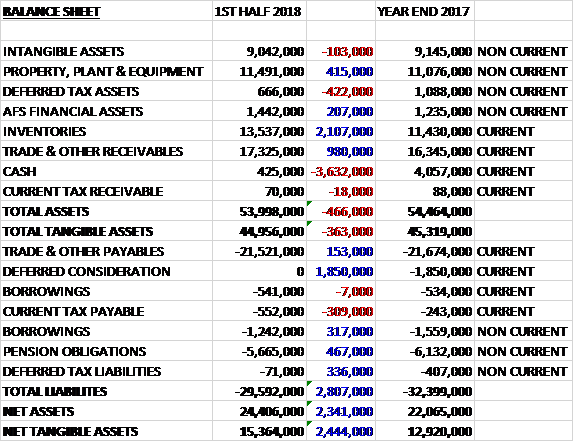

When compared to the end point of last year, total assets declined by £466K driven by a £3.6M reduction in cash and a £422K fall in deferred tax assets, partially offset by a £2.1M growth in inventories, a £980K increase in receivables and a £415K growth in property, plant and equipment. Total liabilities also decreased during the period as a £309K increase in current tax payables was more than offset by a £1.9M fall in deferred consideration, a £467K reduction in pension obligations, a £336K decline in deferred tax liabilities and a £310K fall in borrowings. The end result was a net tangible asset level of £15.4M, a growth of £2.4M over the past six months.

Before movements in working capital, cash profits increased by £471K to £3.6M. There was a cash outflow from working capital and after tax payments fell by £403K then net cash from operations came in at £268K, a decline of £610K year on year. The group spent £1.1M on capex and £1.9M on acquisitions which gave a cash outflow of £2.7M before financing. The group also repaid £300K of loans and paid out £590K in dividends to give a cash flow for the period of £3.6M and a cash level of £425K at the period-end.

The underlying operating profit in the brands division was £2.6M, a growth of £730K year on year. Branded sales growth was driven in particular by UK growth of key brands Dirty Works, Dr. Salts and Super Facialist along with a successful Christmas gifting period. Internationally, good growth in Western Europe was offset by softer sales in North America. Increased focus on supply chain efficiency and an improved mix resulting from a clearer brand portfolio prioritisation strategy, supported an increase in margins.

The performance of the Brand Architekts portfolio acquired in June continues to be very positive and this momentum is continuing with all key brands in growth. The sell through of Christmas gift ranges was particularly strong. The original Swallowfield brands have also prospered with strong combined revenue growth of 50%. 47 new products were launched across nine different brands. Particular successes include Super Facialist Hyluronic and Retinol ranges, Dirty Works Foaming Sugar Scrub and Quick Fix Facials Black Peel Mask.

Further products in the Brand Architekts range have been produced at Swallowfield sites in the period. An initiative to take further products into in-house manufacture is already underway and will follow in the second half. On an annualised basis they expect to be producing over 1.5m units of the brands in the next year. Further investment and improvements in relation to the e-commerce capability for key brands is in place with a team based in a new Exeter office driving strong sales growth and developing digital marketing activities.

Internationally, highlights included the launch of Dirty Works in France and Belgium and the extension of the Bagsy brand in France. This growth has been more than offset by some trading challenges in North America. Going forward there are a number of new opportunities being progressed that the board expect will bring new customers and geographies in the months ahead.

The underlying operating profit in the manufacturing division was £1.9M, a decline of £186K when compared to the first half of 2017. Sales reflected the normalisation of volumes on a number of major new product launches for global brand owners that peaked in the first half of the prior year. Outside of this effect, there was solid growth across the remainder of the customer base and a good performance at the margin level being maintained as continued focus on their drive product categories and a series of cost optimisation projects were able to offset broader inflationary pressures on materials.

During the period the group secured their first orders with a major US global consumer group and sales of plastic aerosol products continued to grow with the technology being extended to another brand in the second half of the year. Capital investment in increase wood pencil capacity and cost efficiency at the Bideford site has been completed. Further investment to deliver improvements in capacity and costs are scheduled with particular focus on personal care aerosols.

A number of new contracts and product launches have been confirmed and the group have either started production or received purchase orders in the weeks since the period-end.

The group has completed the acquisition of men’s grooming brand Fish which currently retails in Boots, Superdrug, Tesco and Waitrose. The consideration involves an upfront cash payment of £2.7M with a further £300K twelve month performance based earn out, financed via a new term loan. Last year the brand generated £400K of EBITDA. The board see many opportunities to accelerate the growth of the brand in the UK and beyond in terms of adding new products and broadening retail distribution. The founder, Paul Burfoot, will work with the group as a consultant and he continued to operate the Fish salon in Soho.

After five years as CEO, Chris How has informed the board of his intention to step down to pursue a non-executive portfolio career. He will be succeeded by Tim Perman who is currently Group Category and Brand Director and Divisional Director of Beauty at PZ Cussons.

Going forward, trading since the end of the period has been in line with expectations. The board expect the positive momentum seen in the owned brands business to continue, further new product launched and retail distribution gains have been secured in the UK and internationally which will contribute to growth in the second half and into the next year. The acquisition of the Fish brand should add further to this momentum.

In the manufacturing business, the second half will see the start-up of production on a number of significant new contract wins which will contribute positively to the second half of the year. They are seeing upward pressure on material and operational costs but have put in place a range of projects to mitigate. This combined with strong trading momentum leaves the group well place to achieve planned profits for the full year.

At the current share price the shares are trading on a PE ratio of 23.1 which falls to 14.3 on the full year forecast. After an 18% increase in the interim dividend the shares are yielding 1.6% which increases to 1.8% for the full year. At the period-end the group had a net debt position of £7M compared to £3.6M at the start of the period.

Overall then this has been a decent period for the group. Profits were up and net assets increased. The operating cash flow declined but this was due to working capital movements and cash profits increased. The group is not producing any free cash at the moment though so should arguably be conserving cash and not spending it on dividends. The brand business is doing well but the manufacturing business saw a decline in profits. This has been flagged up though and the second half looks more promising.

There is likely to be some disruption surrounding the change of CEO but with a forward PE of 14.3 and (uncovered) yield of 1.8% these shares are just about worth holding on to I think.

Swallowfield have now released a trading update covering the year as a whole. Overall they have traded broadly in line with expectations. The board expect revenues to be similar to last year, driven by double digit growth in the brands business and single digit decline in the contract manufacturing business. They expect pre-tax profit to be significantly ahead of last year, driven by the strong performance in the bands business and a reduction in LTIP charges.

The brands business has increased revenues by 16% and full year profitability will be significantly above both management’s expectations and the prior year as a result of improving margins. The recent acquisition of Fish has been integrated into the portfolio and is trading well.

Revenue in the contract manufacturing business has declined during the year. It has also been affected by material cost inflation and this, combined with a slower than expected start-up of the three major new contracts previously highlighted, has resulted in significantly reduced operating margins. Actions are underway to mitigate the material cost increases and the new contracts are now in full production and expected to contribute to future growth.

The acquisition of Fish, deferred consideration for Brand Architekts and the maturing of LTIP awards along with the movement of working capital have resulted in an increase in the net debt position to £11M. The board expect net debt to reduce significantly in the new financial year.

The board remain confident of the prospects for the New Year and they expect their brands business to continue to grow strongly. Whilst cost pressures are expected to continue, they expect their contract manufacturing business to return to stronger profitability as a result of current actions on costs and growth from the new contracts.

On the 30th July it was announced that non-executive director Roger McDowell purchased 36,250 shares at a value of just under £100K.