Ricardo has now released its interim results for the year ending 2017.

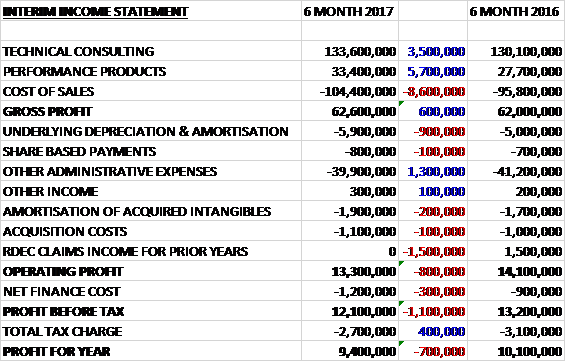

Revenues increased when compared to the first half of last year due to a £5.7M growth in performance products and a £3.5M increase in technical consulting. Cost of sales also increased to give a gross profit £600K higher than last time. Depreciation and amortisation was up £900K but other admin expenses declined by £1.2M. After the RDEC claims were not repeated this time, however, which brought in £1.5M in the first half of last year, the operating profit declined by £800K. Finance costs increased by £300K but the tax charge was down £400K to give a profit for the period of £9.4M, a decline of £700K year on year.

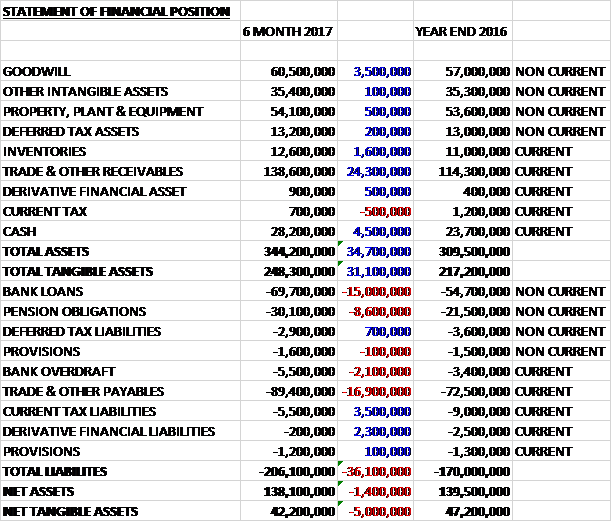

When compared to the end point of last year, total assets increased by £34.7M driven by a £24.3M growth in receivables, a £4.5M increase in cash, a £3.5M growth in goodwill and a £1.6M increase in inventories. Total liabilities also increased during the period was a £3.5M decline in current tax liabilities and a £2.3M fall in derivative financial liabilities were more than offset by a £15M increase in bank loans, a £16.9M growth in payables, an £8.6M increase in pension obligations and a £2.1M growth in bank overdrafts. The end result was a net tangible asset level of £42.2M, a decline of £5M over the past six months.

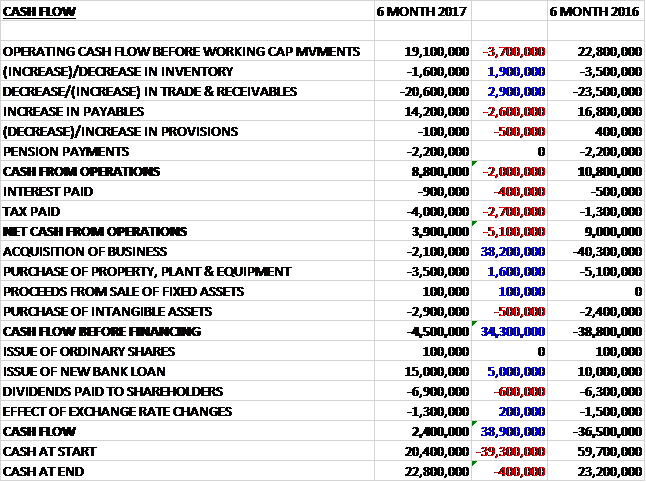

Before movements in working capital, cash profits fell by £3.7M to £19.1M. There was a cash outflow from working capital but this was less than last year but interest payments increased by £400K and tax payments were up £2.7M to give a net cash from operations of £3.9M, a decline of £5.1M year on year. The group spent £3.5M on property, plant and equipment; £2.9M on intangible assets and £2.1M on acquisitions to give a cash outflow of £4.5M before financing. They took out £15M on few loans which was used to pay the £6.9M of dividends and leave a cash flow of £2.4M for the half year and a cash level of £22.8M at the period-end.

On a like for like basis, pre-tax profits increased by £300K to £14.7M, taking into account constant currencies and contribution from Cascade.

The underlying operating profit in the Technical Consulting business is £12.9M, a growth of £600K year on year. The division experienced a low level of orders in Q1 but this recovered in Q2 and overall they were slightly ahead of the first half year which should put the business in a good position to grow in H2. The rail business is now completely integrated and has had a strong order intake in the period from a wide geographical spread of customers. Rail’s profit also benefited from favourable forex movements.

The US market remains challenging but the group’s focus continues to shift towards their operations in California where the market for new vehicle technologies provides greater opportunities. The energy and environment consulting business continued to broaden its customer base and reduce its reliance on the public sector. In November it was appointed as the UK’s National Atmospheric Emissions Inventory agency on behalf of the Department of BEI.

The performance of the business in Asia has been decent and they enter the second half of the year with a stronger order book than the prior period, particularly in the Rail business. The strategic consulting activities continue to make good progress.

The underlying operating profit in the Performance Products business was £3.4M, a growth of £400K year on year driven principally by increased volumes of engines in respect of the contract for McLaren, offset by lower one-off software license sales than the prior period.

Despite a slow start in Q1 the automotive business in the US and in Europe, order intake improved in Q2. The group have seen good levels of activity in Asia, particularly in China. They have secured a range of large programmes in the core powertrain areas of their business, especially in the engines sector across both light and heavy duty applications and are also seeing significant opportunities in the hybrid and electric systems sector. They continue to invest in advanced combustion and other key technologies in areas relating to improving overall vehicle efficiency such as intelligent driveline and electrification. The future of mobility solutions, including connected and autonomous vehicle technology in particular, is now attracting significant interest across all geographies.

The rail business continues to perform well, all the post-acquisition integration activities have been completed and the business has won significant levels of new orders in the UK, Europe and Asia. They are pursuing a range of large, long-term rail contracts, particularly in Asia and the Middle East, whilst also investing in the development of their portfolio of niche rail products such as PanMon and SmartFleet.

In Energy and Environment, they have secured a number of significant, multi-year contracts in the period through the provision of consultancy services to governments, their agencies and private sector clients. Growth in the environmental consulting business is focused on private sector and international expansion. Recently they have seen good growth in private sector and international projects and are well placed to support clients with the implementation of commitments agreed at COP21 and COP22.

Within the power generation business, the focus remains on growing the large-scale generator sales, together with consultancy on smart grids, energy economics and technologies. Across the renewables business, they continue to pursue a range of opportunities in off-shore win and energy storage applications.

Production of engines for the McLaren 650S, 675LT and 570S continue to meet the needs of the customer. The production of Bugatti transmissions also continues to meet the terms of the supply agreement. The group remains a key supplier to the motorsport sector and continues to manufacture for Formula 1 and the Porsche Cup whilst providing design and development services, including manufactured products, to GT3, LMP1, WRC, R5 Rally and also specification formula series such as Japanese Formula 14, Indy Lights and the Formula V8 3.5.

The total RDEC credit for the current period is £3M compared to £2M last time. This comprised of an estimated RDEC credit in respect of the current period of £2M, together with £1M arising from the routine amendment of open application in respect of previous accounting periods, as a result of further analysis of the qualifying expenditure incurred.

The automotive businesses in the US, the UK and the rest of Europe experienced a weaker than expected Q1 but performance improved in Q2. Going forward, overall they continue to trade in line with their expectations and have a record order book of £244M.

During the period, following formal accreditation by the UKAS to provide certified assurance services for the global rail sector, the group launched Ricardo Certification. The accreditation means that the business can perform notified body, assessment body and designated body roles on any rail project that is required to comply with relevant national and international technical rules. The accreditation also covers railway product certification services.

In July the group acquired Motorcycle Engineering Italia for an initial cash consideration of £2.1M, generating goodwill of £2.4M. The business was formed from the operating assets and employees of Exnovo, a vehicle design house, which creates aesthetics for global motorcycle and scooter brands. During the period the business made no profit but had it been purchased at the period-end, it would have contributed a £100K loss at the operating level.

At the current share price the shares are trading on a PE ratio of 18.8 which falls to 15.2 on the full year consensus forecast. After a 7% increase in the interim dividend the shares are yielding 2.2% which increases to 2.3% on the full year forecast. At the period-end the group had a net debt position of £47M compared to £32.2M at the same point of last year.

Overall then this has been a bit of a subdued period for the group. Profits declined, although excluding last year’s one-off RDEC claim it increased but having said that underlying RDEC was higher this time so perhaps without this profit would have fallen – all very confusing. Net assets also declined and the operating cash flow fell with no free cash being generated. It seems that Q1 was poor but Q2 better so perhaps performance will improve in H2. The performance products business is ticking along nicely due to higher volumes of McLaren engines and the rail business seems to be performing well with automotive a little more subdued.

With a forward PE of 15.2 and yield of 2.3% these shares aren’t that cheap and although it should improve in the second half, the performance hasn’t been that good here. Having said that, this remains a quality company and I am still invested for now.

On the 9th May it was announced that non-executive director William Spencer purchased 8,000 shares at a value of £73,200.

On the 6th July the group released a trading update for the year as a whole. Order intake was slightly ahead of the prior year at £360M but was significantly higher excluding the large multi-year transmission supply contract awarded in June 2016. The closing order book at the end of June is over £240M, an increase of £9M. At the end of the year net debt was £38M.

The rail and energy and environment business continue to perform strongly but the automotive business has had a disruptive year given the wider macro-economic factors, although it enters the new year with good momentum in Q4 and a good order book and pipeline. The performance products business continues to perform well with continued growth in McLaren volumes and a recent contract to supply transmissions to Aston Martin.

Overall this is not a bad update but the group seems to have lost a bit of momentum with the poorly performing automotive division. On the other hand the group has lost quite a lot of value recently and is starting to look a bit better on a value front. Tricky one this.

On the 2nd August the group announced that it had signed an agreement to acquire the US-based engineering firm Control Point which will become part of the group’s US subsidiary Ricardo Defence Systems and expand the range of opportunities that can be pursued within the US defence sector. New capabilities acquired include expanded vehicle engineering capabilities. Expertise in distributed software based systems and fleet management. The total cash consideration is $10.2M. It is hard to ascertain whether this is a good deal or not but the fall in the share price recently is starting to make these shares look interesting again.