Sainsbury has now released its full year results for the year ending 2014.

Revenues from the retail stores were up £618M on last year and the newly acquired bank made revenues of £28M. Cost of sales were also up, including employee costs that increased by £115M and the gross profit was some £110M higher than in 2013. A number of one-off items were present, including £148M of past service credit related to the closure of the pension scheme to future accrual, a £76M payment with regards to VAT refunds on nectar points and a £92M impairment of land and buildings where the group no longer intends to build supermarkets, which were counteracted by an increase in other admin costs to give an operating profit £127M higher. Finance costs were broadly unchanged and taxation just a little bit higher so the profit for the year was £716M, a hike of £114M over last year which seems to be a decent outcome.

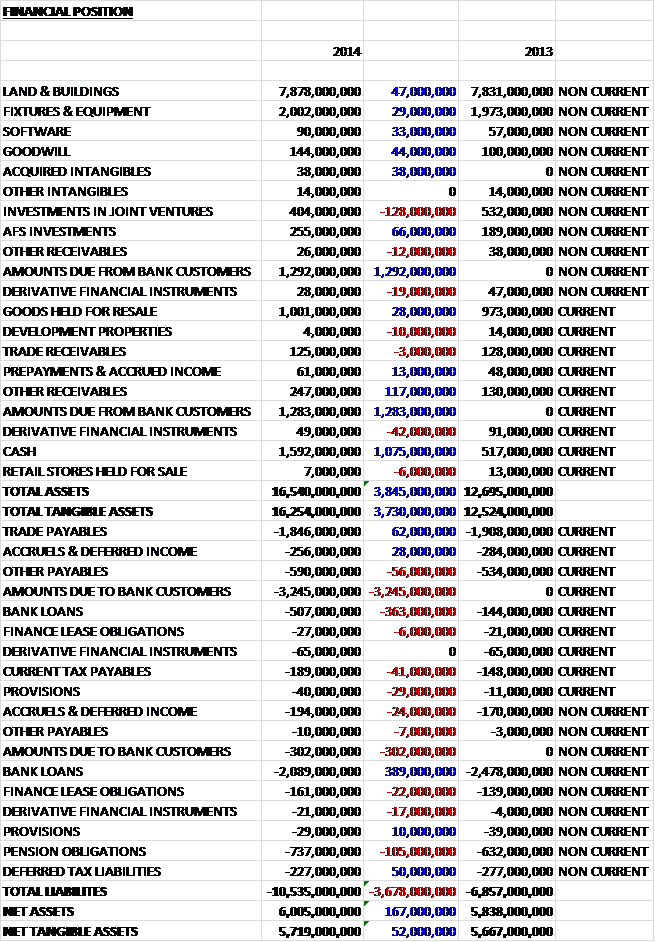

Assets were up by some £3.845BN over the end of last year. These increases were predominantly relating to the acquisition of the bank with loans to customers totalling £2.575BN, a £1.075BN increase in cash levels and a £117M increase in other receivables which are bank funds in the course of settlement, only partially mitigated by a £128M reduction in investments in joint ventures. As would be expected, liabilities also increased due to the £3.547BN in customer bank deposits acquired with the bank. The only other increase of note was a £105M hike in pension obligations. All of this meant that the increases in liabilities and assets broadly cancelled each other out and net tangible assets only increased by £52M year on year to £5.719BN. Still, this is better than a fall and is a substantial amount of equity.

Before movements in working capital, cash profits were some £72M higher than last year at £1.366BN. Due mainly to a decrease in payables (partly driven by Easter phasing), however, this became £1.227BN after working capital movements, £41M lower than last year. After interest and tax, this became £939M in net cash from operations. This cash was almost entirely swallowed up by £916M in capital expenditure. The bank acquisition came with £1.016BN of cash when the acquisition costs are taken off, which accounts for the positive cash flow of £1.075BN at the end of the year. The group also gained £335M from the sale of property, plant and equipment which paid for the dividends. There was a small net increase in borrowings but this was not particularly material. Overall then, the £1.075BN of cash the group made is clearly good but when it is realised this is entirely due to the cash received with the bank, this does not look so spectacular. It is also apparent that the dividends are not being paid out of operating cash flows, which entirely go on capital expenditure but from sale and leaseback proceeds.

Retail sales grew by 2.7% with like for like growth at 0.2% which was lower than Sainsbury’s own guidance due to the difficult market and it is a little worrying to see that decent increases were experienced in the first half of the year but like for like sales declined by 3.1% in the final quarter. The convenience business grew sales by 19% to £1.8BN and online groceries increased by 12% to over £1BN. Retail underlying operating profit increased by 5.1% to £873M, reflecting cost savings of £120M during the year with a similar level of cost savings expected next year. Bank income fell by 4.2% to £229M mainly due to a reduction in the earned interest rates on the loan book due to strong competition, and also a decline in commission due to price deflation in car insurance. The Bank delivered an underlying operation profit of £53M, 10.2% less than last year due to the above reduction in income and a provision relating to potential customer redress payable in respect of Card Protection Plan insurance. The bank is expected to make a similar level of profit next year.

The group have invested in own brand products and they are growing at over twice the rate of branded lines and account for about half of food sales. The Premium Taste the Difference range achieved double digit growth and a new factory has been opened to create desserts for the range using British ingredients. The Basics range is doing less well and sales declined during the year, the response has been to rebrand with new packaging so hopefully the decline can be reversed. A big part of Sainsbury’s success in recent times has been down to trust, as demonstrated during the horsemeat scandal where no products were found to be contaminated. Indeed, the group have been DNA testing their food for 10 years to guarantee provenance and this has been expanded during the year. Also, there is a strong commitment to source locally with pork and chicken now 100% British.

The group have made a big investment in the TU clothing line this year and it generated annual sales of about £750M. A two year deal has been signed with designer Gok Wan whose designs prove popular with customers. The back to school range this year was the most successful such event in the group’s history. General Merchandise sales are now over £1BN and Sainsbury is the 6th largest homeware retailer by value. Cookware and Kitchen appliances have enjoyed double digit growth and the group have outperformed the market in all their entertainment categories. Some of the stores have been converted to “department store” layouts and they have progressed well so the concept is being rolled out in more than 150 stores in the coming year. The Digital entertainment offering has been slower to gain traction than expected but progress is being made. Meanwhile the pharmacy business is continuing to develop through in-store and hospital out-patient pharmacies.

Convenience store sales have increased by 19% year on year but securing appropriate sites have become increasingly competitive. The website has been enhanced during the year to give a more intuitive search and the new mobile website will be a boon going forward. Overall, online grocery sales increased by 12% year on year although a decline in marketing spend whilst the website was upgraded did impact sales growth in the short term. There are plans to open a dedicated online fulfilment centre within the next few years in Bromley-By-Bow to help meet the growing demand in the South East.

Clearly one of the major events of the past year was the purchase of Lloyds Bank’s 50% share in Sainsbury Bank. The group spent £199M in cash and £5M in deferred consideration. With this acquisition came net assets of £352M with a goodwill payment of £45M. The bank also came more than £1BN of cash balances included in the above net asset figure. As the group build the new systems for the bank, profit growth will be constrained by double running costs and a total of £260M in transition costs and capital expenditure will be incurred in moving to the new platform (£45M next year). The bank currently has 1.6M customer accounts and the products are designed for customers of the supermarkets, for example the Nectar Credit card that gives extra points on Sainsbury purchases. The insurance market has become increasingly price driven which has reduced retention and profitability, despite this Home Insurance has performed quite well. The Travel Money bureau performed well with sales increasing by 23% year on year and 107 new ATMs have been opened.

The mobile phone network is still in its first year of business and progress has not been as quick as expected. The network is a joint venture with Vodafone and it includes Nectar incentives. In order to support this, the group have opened phone shops in some of the larger stores. In its first year the joint venture suffered losses of £4M due to start-up costs and is expected to make a similar loss next year. The ebook business is still very small and in its first year of trading and is being offered on the website. The Energy business offers gas and electricity and again, uses Nectar points as incentives. The group have gained 60% more customers than last year as the business makes progress.

There have been a number of investments in land and infrastructure. This includes a £500M project with Barratt at Nine Elms with 737 new homes, a new supermarket and local shops, restaurants and office space. The group have also opened a new £30M convenience depot in Thameside to support the growth of the convenience network in the South East and work has begun on a new distribution facility in Daventry to support the general merchandise business.

As mentioned previously, this is a bit of a milestone for Sainsbury. CEO Justin King steps down at the AGM to be replaced by Commercial Director Mike Coupe and Mike has had quite a while to learn the ropes.

Going forward, despite some signs of economic recovery, the food retail sector is likely to remain challenging. Customers continue to focus on value and as such the discounters have continued to gain market share, although Sainsbury seems to be less affected by this trend than some other supermarkets, indeed they are the only “big 4” supermarket to maintain market share this year. However, the group are still planning on opening 13 new supermarkets and 91 convenience stores during the upcoming year.

Net debt is currently running at £2.384BN, an increase of £222M over the end of last year. This was driven by the additional funding used to acquire the bank and an increase in working capital. The shares look undervalued on a P/E level as the underlying ration is 9.9, although this is expected to increase to 10.8 next year this is still on the value end of the spectrum. Likewise, after a 3.6% increase in the final dividend, dividend yields are strong, being at 5.5% this year at the current share price and predicted to rise to 5.6% next year.

Overall then, this has been an interesting year for Sainsbury. As many of its rivals struggle, the group has been able to cling on to increasing retail revenues and profits. Worryingly this trend may be reversing, however, as was seen in Q4. The purchase of the 50% of the bank they did not already own is also clearly a big step forward. Profitability will be constrained in the short term but medium term, this should be a decent source of income albeit with the regulatory risks attached. The other businesses are also still in their infancy but it is good to see some diversification taking place. The core issue, however, is the changing way that customers shop for groceries. They are more driven to discounters, convenience stores and online groceries and while Sainsbury has made good progress on its convenience and online offering, the large superstores are becoming more and more redundant, although the department store idea might have some legs. The migration of customers to the discounters is a little harder to address. The group have been less affected than Morisson and Tesco but this is still something that needs to be addressed. The share price certainly prices in these concerns as evidenced from the yield and P/E ratio and at these prices I am happy to hold.

On the 11th June the group released a trading statement covering the first quarter of the year. Total sales increased by 1% but this was due to new store openings as like for like sales declined by 1.1%. This reflects that growth within the industry is at its lowest level for a decade. Own banded products continued to perform well, however, with Taste the Difference sales up 10%. General merchandise also showed decent strength, with clothing delivering double digit growth and the group are trialling an online clothing offer which should further drive sales. Entertainment showed good growth and convenience sales grew by 18% year on year as the 200th store was opened in London. Online grocery sales increased by 10% following the roll out of the improved website and Sainsbury Bank’s transition remained on track. Although the like for like sales decline is a disappointment, it was not altogether unexpected and I remain happy to hold.

On the 20th June the group announced that they are entering into a joint venture with Dansk Supermarkets to resurrect Netto in the UK. The initial trial will consist of 15 stores to be opened before the end of 2015, with the first in the North of England. If the trial is successful the new format stores will be rolled out across the country. Sainsbury will provide an initial £12.5M to the joint venture and will probably incur a loss in the region of £5M to £10M up to mid 2015. The new stores will be in a completely different format to that of the Netto stores that left the UK market in 2010 and will offer discounted wares a long with an in-house bakery offering fresh Danish breads and pastries. This is an interesting move by Sainsbury. It is clearly an attempt to grab some of the increasing discount market. I believe this is an excellent idea and am quite excited to see how it pans out.

On the 1st October the group released a statement covering Q2 trading. Like for like retail sales were down 2.8% and total retail sales fell by 0.8% (all excluding fuel). The market remained very competitive and customers continued to buy more in convenience stores, reducing the average basket size. Sainsbury now matches prices to Asda, even when they are on promotion, and have stopped matching with Tesco. General merchandise performed well with a double digit growth in sales and convenience sales increased by 17%. Online grocery sales increased by 7%, impacted by a high level of competitor customer acquisition. During the quarter the group opened 23 new convenience stores and two new supermarkets and they remain on track to deliver five new Netto stores by the end of the year. Going forward, it is believed that the significant pricing activity and food price deflation seen this quarter will continue for the foreseeable future and management now expect like for like sales in the second half to be similar to the first half of the year. So, this update is clearly not that good but was known well in advance and there are no surprises here.