Sainsbury has now released their interim results for year ending 2015.

Although retail revenues fell by £187M, this was counteracted somewhat by a maiden revenue from the bank but a £310m charge for store impairments meant that gross profit was some £211M lower than last year. There were more one-off costs in admin expenses related to the write-downs in property values and admin expenses themselves also fell to drive the group to an operating loss of £234M, a £723M reversal from last year. Changes to finance costs and income broadly offset each other and due to lower profitability, lower tax was paid but the loss for the first six months of the year was £344M, a £684M fall when compared to the first half of 2014.

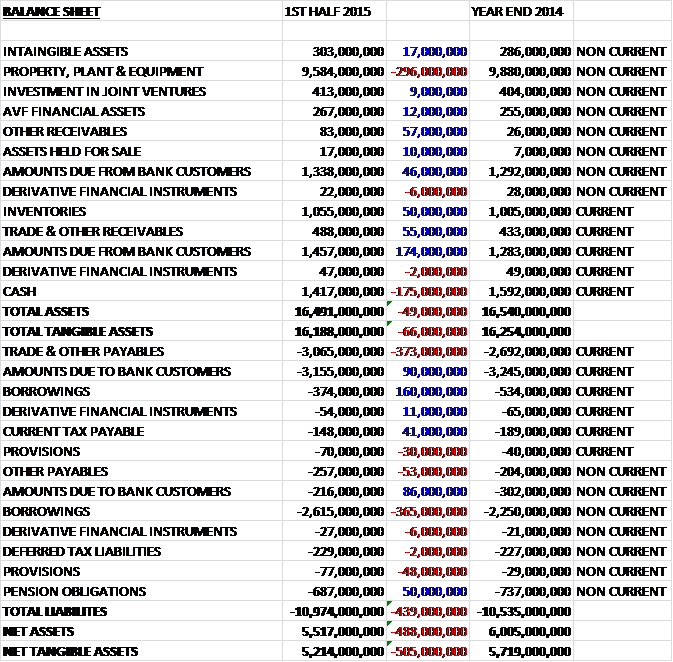

When compared to the end point of last year, total assets fell by £49M as a £296M fall in the value of property, relating to the previously mentioned impairments and a £175M decline in cash levels were somewhat offset by a £220M increase in amounts due from bank customers and a few other smaller increases. Liabilities increased considerably during the year as borrowings increased by £205M and trade & payables increased by a hefty £373M to give a net asset level down by nearly half a billion pounds at £5.517BN.

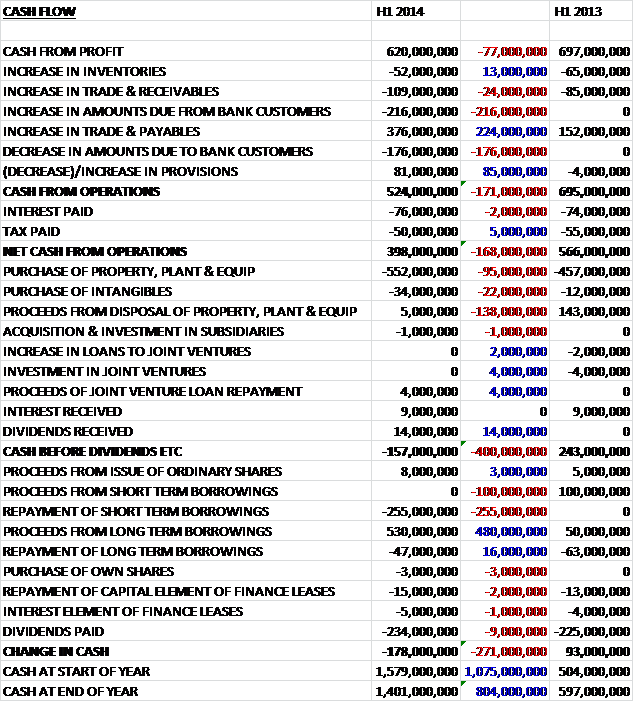

Before movements in working capital, the cash from profit was down £77M at £620M. Adverse changes in working capital, particularly in regards to the newly set up bank, meant that cash from operations before tax was £524M, a £171M reduction from the first half of 2013. This was eroded further by interest and tax so that net cash from operations was £398M, a fall of £168M. Sadly this cash was not enough to cover capital expenditure which was £552M on tangibles and £34M on intangibles. The only other major expense was the £234M spent on dividends (clearly not covered by cash) and a net £228M of new loans flattered the cash flow somewhat but the group still had a £178M outflow despite the new borrowings. At £1.4BN, the cash levels were healthy, however.

This was a period where there were a number of one-off items affecting results. Underlying profit before tax was actually £375M which was much better than the actual profit figures bit still some £25M behind the same period of last year. A £287M charge was recognised against property that will no longer be turned into stores after the group decided there wouldn’t be a decent return on the investments and £341M was recognised against currently unprofitable stores already built. The amount of new space being opened per year is going to decline from 500,000 sq feet this year and next to 350,000 in 2017/2018 with eight new supermarkets and over 100 new convenience stores per year. The three start-ups, including the mobile service, I2C and Netto are expected to make losses of about £10M this year.

Underlying retail profits before tax were £332M compared to £380M this time last year and it is disappointing to see that sales in Q2 fell by a sharper rate than in Q1. Clearly the food business performed poorly during the year but there were pockets of good performance as the premium own brand offering increased by 4% year on year. Non-food seems to be doing rather well with clothing and general merchandise both growing at over 5% per annum and the group sees these areas as significant drivers for growth going forward and it seems management are targeting a more department store look for some of the larger supermarkets. Another growth area is convenience stores and during the year convenience sales grew by 17%. Online orders increased by 9% during the period, held back somewhat by unprofitable customer activity.

Underlying bank profit before tax was £35M, an increase of £23M on last year. The increase is due to a higher total income and favourable bad debt levels (an improvement from 1.3% to 0.8%). The bank is currently being transferred on to a new platform which is expected to be up and running by winter 2015 with cards and loans migrating across by summer 2016. New credit card accounts grew by 55% year on year and new loan accounts increased by 16%. Following the successful re-launch of pet insurance, sales of that product increased by 86% year on year. Travel Money also had a good half year with sales up 20% and 21 new bureaux were opened during the period.

These are undoubtedly difficult times for the UK supermarkets. The market is changing faster than at any time in the last three decades as customers are shopping more frequently and buying less each time, favouring a combination of online shopping and convenience stores. This means that some of the larger out of town stores are becoming less and less competitive. Sainsbury apparently has smaller stores located on more dense populations than some of the competition, but this change is still going to affect them and management see this trend increasing going forward. Sainsbury are not even holding up against the rest of the market, with their market share falling to 16.7%. It is also notable that there are no sale and leasebacks in the first half of this year.

So what are Sainsbury doing to halt the decline? They are continuing to improve the quality of their own-brand offering and simplifying prices, but perhaps most importantly targeted price investments are to begin immediately with approximately £75M being invested in the second half of this year and the same amount being spent in the first half of next year which will apparently be paid for through efficiencies in the value chain. The group have also identified 25% of the total store portfolio that due to declining volumes will have under-utilised space which is likely to be taken up by non-food offerings. The group are also going to trial smaller convenience stores with a range focused on food to go and are looking at larger convenience stores to improve their offering.

During the period the first Netto store was opened and the group are still on track to open 15 stores before the end of the year which should give them a way to tap into the discount market. The group have identified a number of areas where costs can be cut and hope to generate annual operating cost savings of more than £150M going forward. Additionally capital expenditure is going to be around £950M this year due to investments in convenience but by next year this is expected to fall to less than £550M per annum.

The interim dividend of 5p remains the same and represents a stonking 7.4% yield at current share prices. It is worth noting that going forward management are re-aligning the dividend to be covered two times by underlying earnings and based on forecasts the yield for the full year 2015 comes out at 5.8%, still a good return but lower profitability in the coming years will reduce this further. The current net debt stands at £2.382BN, which was very similar to the level recorded at the end point of last year and close to the expected £2.4BN at the end of this year. Sainsbury expects profitability to be lower still in the second half of the year.

Despite the declining share price it is difficult to recommend further investment in Sainsbury. They are in a rather difficult position as their brand relies on the perceived higher quality and provenance. In order to achieve this, however, margins are thinner than some of the rivals and the group are likely to lose out on a race to the bottom with the likes of Tesco and Asda. Despite the problems in the grocery sales, non-food seems to be a decent growth driver for the group and the bank seems to be off to a good start. Whether the mobile business will be a success going forward remains to be seen. Whilst I am not buying shares at this time, I am holding on to the ones I have (probably a mistake) but if the yield remains above 4% it seems to be a decent income play for the time being.

On the 7th January the group announced a trading update for Q3 which included Christmas trading. Total retail sales excluding fuel fell by 0.4% but like for like sales were down 1.7%. This was a better performance than in Q3 but worse than Q1. This is clearly not a good result, but there were some areas of growth. The premium own brand range grew by 5% and Christmas items seemed to do well with mince pies and turkeys up 8% year on year. The trend of more frequent and local shopping continued and there was a 16% growth in sales at the convenience offering with the biggest Christmas for online sales to date. General Merchandise traded well and clothing sales were up nearly 10% year on year. The outlook for the rest of the year remains challenging with food price deflation likely to continue and the board currently expect like for like trading in Q4 to be similar to that of the first half – about a 2.1% decline in other words. So, the update was not good but not unexpected so I am holding on to the shares for now.

On the 16th January Sainsbury announced that it had replaced PWC as auditor with Ernst and Young. No reason was given, but it seems to be the trend with Supermarkets at the moment after Tesco said goodbye to KPMG.

On the 17th March the group released a Q4 trading statement. The headline figure was that like for like retail sales were down 1.9% excluding fuel. During the quarter there was volume growth across the food business and an average uplift of over 3% on the products that have seen price reductions and like for like transactions grew. The group have implemented their value simplicity programme which replaces one-off promotions with continued lower prices. The general merchandise and clothing business performed well, up more than 6% on the same period of the previous year. There was a 14% growth in the convenience business with the opening of 23 new stores and the online business saw order numbers increase 14% as customers can now click and collect their online grocery orders from over 100 sites. The bank grew sales of its loans by 21% and Argos digital stores were opened in ten of the supermarkets.

It is expected that the market will remain challenging for the forseeable future with food deflation likely to continue for the rest of the calendar year and competitive pressures continuing. The board believe that the group should be able to outperform their supermarket peers. That will remain to be seen but it does sound as though progress is being made. In the near term, though, things look tough and after selling out earlier in the year, I will remain on the sidelines for now.

On the 27th April it was announced that David Keens will joint the board as non-executive director, replacing Gary Hughes who previously announced his retirement. David was the finance director at Next from 1991 to 2015 and seems an excellent appointment given his success there and Sainsbury’s desire to growth their non-food sales.

On the 29th April the group announced that CEO Mike Coupe was involved in a court case in Egypt. When Mr El. Nasharty bought the group’s interest in the ill fated Egyptian joint venture, he paid with cheques that bounced. He is now claiming that Mike was in Egypt in July last year and seized the cheques. Mike was convicted in his absence in a court case that he was apparently unaware of for an offence that took place while he was in the UK. This is a rather strange distraction but does rather re-iterate the potential danger of doing business in countries that do not have such an advanced justice system.