Serabi Gold has now released its interim results for the year ending 2015.

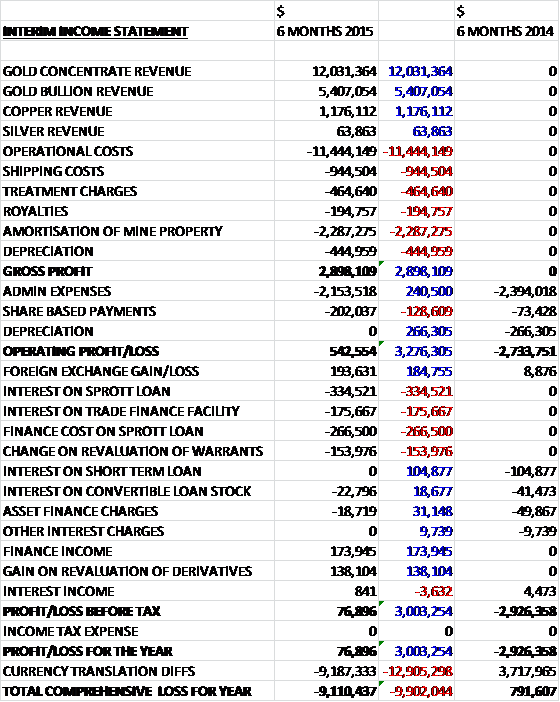

There was no commercial production in the first half of last year so there are no comparatives. We can see that gold concentrate makes up the bulk of the revenue and operational costs are the largest cost of sales item. The gross profit for the half year stood at $2.9M. Admin expenses fell by $240.5K, principally due to the devaluation of the Brazilian real and the lack of legal fees associated with last year’s placing, but share based payments did increase somewhat to give an operating profit of $543K compared to an operating loss this time last year. Finance costs increased during the year as a the interest on the Sprott loan increased by $335K, the finance cost on the same loan increased by $266.5K and related to the call option granted over 4,812 ounces of gold, the interest on the finance facility increased by $176K. The change on the revaluation of warrants came in at $154K compared to a maiden finance income relating to income due arising from short term movements in the gold price between contractual pricing arrangements with the designated refinery and the price ruling when the group draws down on the trade finance arrangement, and a $138K gain on the revaluation of derivatives. The overall profit for the half year stood at $77K compared to a loss of $2.9M in the first half of last year. There were currency translation losses of $9.2M, however, due to the collapse in the Brazilian Real.

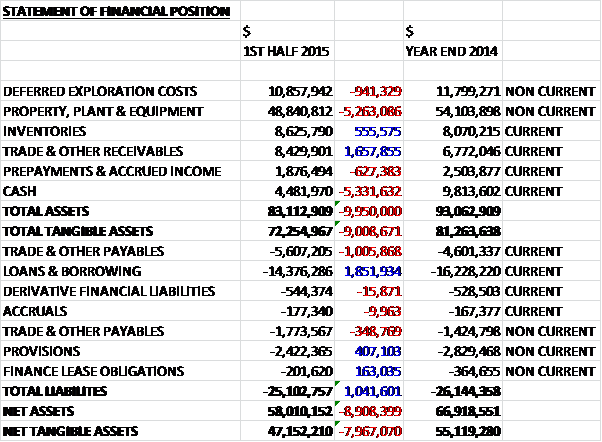

When compared to the end point of last year, total assets fell by $10M driven by a $5.3M decline in cash, a $5.3M fall in property, plant and equipment due to currency differences and a $941K decrease in deferred exploration costs, also due to the depreciation of the Brazilian Real. Total liabilities declined during the period as a $1.9M fall in loans and a $407K decline in provisions, again due to the depreciation of the Real, was partially offset by a $1M increase in current payables and a $349K increase in long term payables. The end result is a net tangible asset level of $47.2M, a decline of $8M over the half year period.

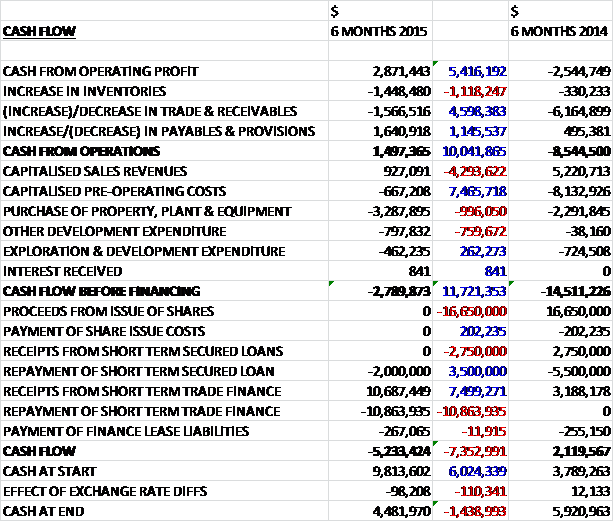

Before movements in working capital cash profits came in at $2.9M, a positive swing of $5.4M year on year. We then see an outflow of working capital due to a modest increase in inventories and receivables as a higher amount of concentrate was awaiting settlement from the smelter as per the contractual arrangements. This gave a cash from operations figure of $1.5M. As the Sao Chico mine is not yet in full production, the revenue and costs from this mine were capitalised as can be seen here but the operating cash flow is not year enough to cover capital expenditure with a $3.3M purchase of property, plant and equipment giving rise to a $2.8M cash outflow before financing. The group then repaid $2M of the short term loan and a small amount of finance leases to give a cash outflow of $5.2M for the half year and a cash level of $4.5M at the six month period.

Overall some 14,843 ounces of gold was produced from Palito and 783 ounces from Sao Chico with the all-in sustaining cost of production coming in at $967 per ounce and an average realised price of $1,186. The group is currently forecasting gold production for 2015 of approximately 35,000 ounces with an all-in sustaining cost of between $900 and $950 per ounce.

The Palito mine has now reached a relatively steady operational state with mining activities expected to generate some 90,000 tonnes of ore at around 8.5g/t during 2015. The gold generated from this mined ore will be supplemented during 2015 by running down surface stockpiles of ore that have been established over the first year of operations, and by the reprocessing, through Carbon in Pulp recovery circuit, of the stockpiled tailings accumulated from the initial floatation recovery process during the first three quarters of 2014. The group plans to undertake further ramp development during the year to access the next level at -19 metre relative level, significant focus will be given to accessing and developing drilled parallel vein structures on production levels above the 24mrl. These include the Chico de Santa zone which lies to the north of the primary G1, G2 and G3 veins and the Senna zone which is located to the south of the Palito West vein complex and which during 2008 and 2009 produced oxide material in excess of 3g/t.

The two mines together resulted in over 57,300 tonnes of ore being extracted during the first half of the year and the gold grade of the ore being mined has averaged 9.95g/t. The group has adopted selective mining in some of the development drives which has reduced dilution and resulted in higher grades of development ore being extracted from development mining activities. A total of 3,569 metres of horizontal development was completed during the period and management remains focused on ensuring that development mining rates are maintained to ensure that adequate stopes are generated to maintain ore production rates. The better than forecast performance at Palito has resulted in the surface ore stockpiles not being run down as quickly as forecast and by the end of June the surface stockpile was 7,744 tonnes with an estimated average grade of 3.41g/t.

Total volumes processed during the period were 64,691 tonnes. Milling performance at the start of the first quarter was affected by power stoppages resulting from an inconsistent electricity supply by CELPA, the regional power supply company. During Q2, the group has, in the short term during the rainy season when grid power is particularly subject to interruption, taken the decision to commit to the use of diesel generated power for the operation of the plant. Management expects that the benefits of increased plant availability will significantly outweigh the increased operational costs.

During the period the group also commenced processing of the flotation tailings that were produced during the first three quarters of 2014 through the CIP plant. The material is being used as top-up feed for the CIP plant as and when the opportunity arises. The process plant is however often close to capacity and this restricts the rate at which this material can be added into the CIP plant and thus the rate at which this material can be run down. At the start of the period a stockpile of more than 50,000 tonnes of material which management anticipates has an average grade of 2.5g/t had been established. Priority will always be given to higher grade material and in particular the treatment through the CIP plant of Sao Chico ore, so processing of these flotation tailings remains very much a secondary priority.

At Sao Chico, by the end of June about 9,100 tonnes of ore had been extracted and over 4,100 tonnes processed through the gold recovery plant at Palito. During 2015, the main vein will continue to be developed and evaluated with the continuation of on-lode development, surface and underground drilling. The vein is sampled with each advance in the gallery. The mine, whilst contributing to the group’s gold production during the year, will be primarily in development and is not expected to achieve its full production potential until 2016. A 5,000 metre diamond drilling campaign commenced in March the results of which, in conjunction with the on-lode development mining that will take place in 2015, will help the understanding of the ore body and facilitate the mine planning for 2016.

In January the ramp development intersected the main vein, the principal currently identified structure at Sao Chico, approximately 30 vertical metres below the portal entrance, in a four metre high and four metre wide gallery, crossing the ore perpendicular to its strike. The initial sampling confirmed a payable intersection with a true width of 3.6 metres and a gold grade of 42g/t. The group has now deepened the ramp down to the next level at 182m, where the main vein has been intersected. Development of the main vein itself on the initial level at 216m has been ongoing since the initial intersection in January. A total of over 600 metres of development following the main vein to the east and west of the initial intersection had been completed by the end of the period.

Four distinct ore zones, totalling around 250 metres have been identified within this 600 metres of development. The largest of these has been developed and prepared for stoping with the first production stope at the 216m now underway. With the development having identified that scope exists at Sao Chico for mined widths of over 3 metres, it is becoming clear that the main vein exhibits mineralised widths that will require the use of both selective manual mining and mechanised mining methods. The group has adopted a mechanised mining method for this first production stope. These findings along with the mine development and ongoing drill programme which commenced in late March are enabling the group to better understand the geometry and continuity of the Sao Chico deposit.

The decline ramp is being driven initially to two development levels, at the 216m and the 182m levels, approximately 30 vertical metres and 60 vertical metres respectively below the surface. The development levels will follow the main vein to its strike extents to the east and west. This work will allow the group to better evaluate the continuity and payability of the mineralisation. The group plans to undertake over 900 metres of ramp development and 1,000 metres of ore development at Sao Chico during the course of the year. Ore transportation to Palito began in February and processing of Sao Chico ore through the Palito gold plant commenced in April.

To enable processing of the Sao Chico ore through the Palito gold recovery plant, a separate process line has been established with a dedicated feed hopper which can feed one of two mills with a dedicated feed of Sao Chico ore. The construction of the hopper was completed at the end of Q1 and after an initial commissioning period using ore from Palito, the processing of the Sao Chico ore started at the end of April. Over 8,300 tonnes mostly of development ore had been extracted by the end of June and included 702 tonnes extracted during June at a grade of 7.72g/t that was extracted primarily from the first production stope.

The group started a 5,000 metre drill programme in March and to date a total of 4,700 metres have been completed in 25 holes. The drilling campaign is a combination of in-fill and step-out drilling and the results from this, in conjunction with the on-lode development mining that will take place during the remainder of 2015 will help the understanding of the ore body and facilitate the mine planning for 2016. The group is still mining on a trial licence and continues to prepare the Plano de Approveimento Economico which is the next major requirement in the conversion process.

A resolution was approved that the issued share capital of the company should be reduced by cancelling and extinguishing all of the issued deferred shares of 4.5p and 9.5p. This is a good move, I don’t really know why they existed in the first place. There remains 100,000,000 warrants in the company at an exercise price of £0.06 that expire at the start of March 2016. There are also 51,146,285 options outstanding after the lucky management were awarded 15,000,000 more during the period at an exercise price of £0.055.

The group now expects to have sufficient cash flow from its forecast production to finance its ongoing operational requirements and to, at least in part, fund exploration and development activity on its other gold properties. It is worth noting though, that the forecasted cash flow projections for the next year include a significant contribution from Sao Chico where commercial production has yet to be declared. The group has payments of $6.3M in long term debt to pay over the next twelve months along with $556K of finance lease payments and $103K in operating leases.

After the period-end, the Brazilian Real has reduced further in value against the US dollar by approximately 8%. The value of the group’s net assets and liabilities were significantly impacted by the devaluation of the currency during Q1 and this will further exacerbate things – assets will reduce but so will locally derived costs. Last year the group made a loss but on the consensus forecast for profits this year, the shares trade on a very cheap PE of 4.5 so I suppose the market does not believe these figures.

Overall then, this has been another period of good progress for the group. They made their maiden first half profit which is a good achievement given there weren’t even aby revenues this time last year. Net assets did fall but this was broadly attributable to the collapse of the Brazilian Real, which has fallen further since the period-end. The group is still not making any free cash, however, as there was an outflow of $2.8M before financing, although once the Sao Chico mine is making a property contribution, this may change. In all the group expect to produce 35,000 ounces of gold at an all-in cost of $900 to $950 per ounce. During the first half of the year, they had an all-in cost of $967 per ounce and an averaged realised selling price of $1,186 per ounce.

So, things are looking rather good for the company going forward but the continued weakness of the gold price does put a spanner in the works. If it continued to fall, these mines may start to become less economically viable so I think this could be the most important thing to watch.

The share price seems to jump around all over the place but the general trend seems to be negative.

The price of gold does seem to be attempting a bit of a recovery but it is certainly too soon to call the end of the bearish sentiment. Tricky one this, I think the risk of the falling gold price just about outweighs the potential at this company but I will watch closely.

On the 21st October the group released the first results from its surface drilling exploration campaign at the Sao Chico gold mine. A drilling programme of 5,000 metres, totalling some 35 holes, has been ongoing since April targeting the strike and depth extension of the known Sao Chico Main Vein as well as some infill drill holes. There were some excellent high grade intersections with hole 15-SC-093 intersecting three times at a grades of 155.37g/t, 242.68g/t and 105.18g/t.

The high grade gold mineralisation is dominantly hosted in a consistent two to eight metre wide alteration zone which itself is visually easily identifiable. The high grade gold zones within this alteration zone are much less so, however, and as a result the mining operations will require on-lode development at regular vertical intervals, with regular channel sampling and in-fill drilling between these levels to best define the high grade gold mineralisation.

Considering the need to drill a tighter drill pattern at Sao Chico, at least in the short-term, the drilling campaign has had to change focus from step out exploration drilling to more in-fill drilling. The company has therefore taken the view that with this change in priority, the planned resource update will be deferred until 2016. This will allow them time to complete the surface drilling campaign with underground lode-development. They also feel with gold prices being volatile and many miners facing considerable economic headwinds, that the company should be minimising discretionary costs and an independent technical report falls into that category.

I have to say, I didn’t realise conditions were so bad for Serabi that they are needing to conserve cash. Nonetheless, the drill results seem to be pretty decent.

The group have now released an update covering trading in Q3. They continued to average 3,000 ounces a month during the period, they have produced 25,000 ounces so far to date and remain on track to produce 35,000 ounces in the year as a whole, which will be double that of last year. The Palito mine continued to perform well with both mined tonnage and grade exceeding the planned targets. Mined grades for the year remain over 10g/t. During the last quarter, the company began driving long cross-cuts to the Chico da Santa and Senna sectors to the North and South of the Palito Main Zone, two areas which have previously been drilled and have potential. These two new sectors will open up more ore faces.

At Sao Chico, ore development is now on three levels with over 2,000 metres of development mining now completed. This initial development, along with surface and underground drilling is providing the board with a good understanding of the mineralisation. The grades at Sao Chico are, at times, over 100g/t though the high grade ore zones at the mine are not easily visible. As a result, in the mining of Sao Chico they are more reliant on assay control, requiring close spaced sampling. Nevertheless, each month sees an improved level of contribution from Sao Chico to the company’s gold production.

It has become clear that the operation will require increased milling capacity. Since the start of production, the company have never been able to run down their ROM stockpiles, albeit that they are of relatively low grade. The generation of low grade ore in narrow vein mining is part and parcel of the business, as lode development is an unavoidable part of the exploration and evaluation process. As a result there is approximately 14,800 tonnes of ROM stock which they cannot process without increased throughput capacity. A third ball mill identical to the two already operating has been purchased and will be operational in early Q2 2016. This, along with some improvements in the flotation and cyanidation plant, will see the daily throughput increase from the current levels of about 400 tonnes per day to about 500 tonnes per day once the improvements are complete and will also create excess capacity to catch up any lost production caused by unplanned stoppages.

The surface diamond drilling programme has now exceeded 6,000 metres and whilst they have had to tighten up the drill spacing due to the complexity of Sao Chico, some of the results have been good with the two deepest holes both showing grades in excess of 40g/t over mineable widths. They have been complementing this programme with additional underground drilling from within the development galleries. It is anticipated that Sao Chico will enter commercial production late in the year with the forecast of 35,000 ounces at an all-in sustaining cost of $900 to $950 per ounce is still in place.

In all, total production in Q3 was 9,078 ounces of gold. During the period, gold production was derived from the processing of ROM ore from the Palito mine combines with the Palito surface coarse ore stockpiles, the stockpiled tailings established during Palito mine production last year and processing of Sao Chico ROM ore. With a total stockpile of over 42,000 tonnes of flotation tails recovered from last year’s production, the company will continue processing this material when possible but with excellent levels of ROM feed available from both mines, combined with the surface coarse ore stockpiles, available plant capacity of processing the flotation tailings is limited.

At the Sao Chico mine over 840 metres if horizontal development was achieved during the quarter, of which 250 metres involved deepening of the ramp. Over 950 metres of lode development has now been completed on the levels 216mR, 199mRL and 186mRL. Production is now underway, albeit limited as the focus remains on lode development and evaluation. During the quarter, about 6,200 tonnes of development and stope ore were processed through the plant. Whilst the majority of the ore is being derived from the development drives, the Sao Chico ore processed this quarter showed an improved average grade of 7.4g/t of gold.

The company expects to produce 28,000 to 29,000 ounces of gold during 2015 form the processing of Palito ROM and Palito stockpiles. With the Sao Chico mine now under development, the company also expects production of 6,000 to 7,000 ounces of gold from ore mines there.