Serabi Gold has now released its Q1 results for the year ending 2016.

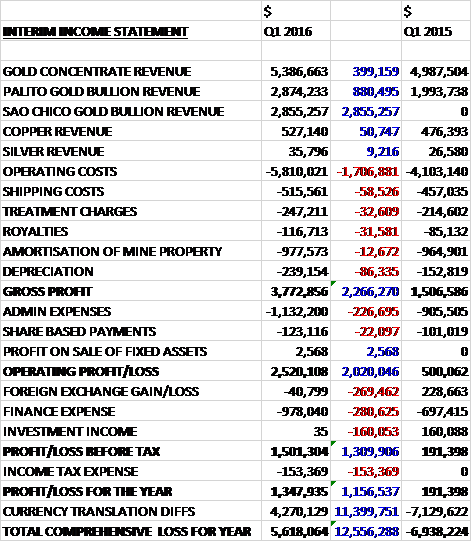

Revenues increased when compared to Q1 last year with a $399K increase in gold concentrate sales, an $880K growth in bullion sales from Palito and a maiden $2.9M contribution from Sao Chico. Operating costs increased by $1.7M, with the bulk of the increase coming from mining consumables and maintenance, and there were modest increases in other costs, with the biggest change being an $86K growth in depreciation due to an increase in mobile fleet acquired for both mines to give a gross profit some $2.3M ahead of last time. Admin expenses increased by $227K due to due diligence charges and an increase in director pension contributions with share based payments up $22K to give an operating profit $2M above that of last time. There was then a $269K detrimental forex movement relating to non-dollar denominated cash holdings and a $281K increase in finance expenses due to finance costs on gold trading and after tax was up $153K the profit for the quarter was $1.3M, a growth of $1.3M year on year.

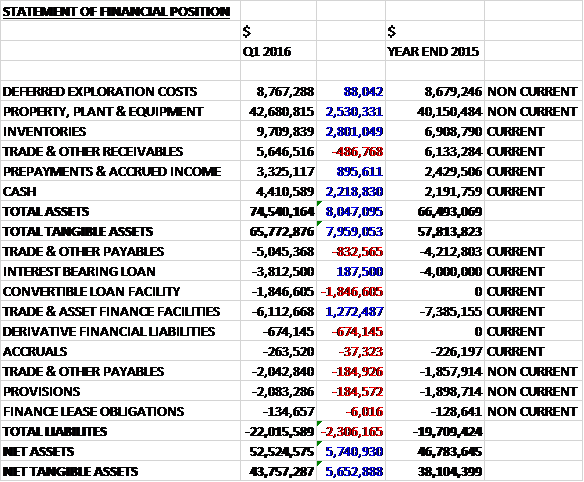

When compared to the end point of last year, total assets increased by $8M driven by a $2.8M growth in inventories manly due to a growth in finished goods, a $2.5M increase in property, plant and equipment relating mainly to forex movements, a $2.2M increase in cash and an $896K growth in prepayments and accrued income, partially offset by a $487K decline in receivables. Total liabilities also increased during the period as a $1.9M growth in the convertible loan facility, a $1M increase in payables and a $674K growth in derivative financial liabilities relating to warrants was partially offset by a $1.3M decrease in trade and asset finance facilities. The end result is a net tangible asset level of $43.8M, a growth of $5.7M over the quarter.

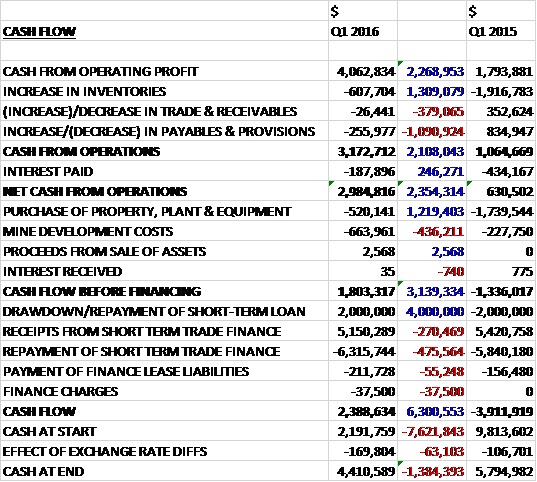

Before movements in working capital, cash profits increased by $2.3M to $4.1M. There was a cash outflow from working capital which was broadly in line with Q1 last year and after interest payments showed a modest fall, the net cash from operations came in at $3M, a growth of $2.4M year on year. The group spent $520K on property, plant and equipment along with $664K on mine development costs to give a free cash flow of $1.8M. A draw down on the short term loan meant that there was a quarterly cash flow of $2.4M and a cash level of $4.4M at the period-end.

During the quarter the group achieved an average gold price of $1,165 per ounce compared to $1,212 in Q1 2015. The total AISC cost of production was $858 per ounce, an increase from the $759 achieved in the same period last year with the increase attributable to Sao Chico entering commercial production. The current gold price is $1,256 so the company should be making some money at these levels.

The group mined 37,546 tonnes of ore at a grade of 11.02g/t compared to 32,204 tonnes at 10.51g/t last time. This represented 26,752 tonnes at 11.84g/t from Palito and 10,794 tonnes at 9g/t from Sao Chico. They milled 36,615 tonnes at a grade of 8.58g/t, an increase from the 36,6,15 tonnes at 8.52g/t in Q1 last year which just represented Pallito production. The lower production from Palito was expected, reflecting the limitations of the level of ore that can be processed and the availability of ore from the Sao Chico mine. The mine production for the quarter is consistent with the production levels reported for H2 2015.

They produced 9,771 ounces of gold in all, up from 7,389. The forecast gold production for the year as a whole is 37,000 ounces at an all in sustaining cost of between $840 and $870 per ounce. At the end of the period, the combined surface coarse ore stockpiles totalled 17,000 tonnes at a grade of 5.3g/t. In addition there are about 32,800 tonnes of flotation tails with an average grade of 2.5g/t waiting to be processed.

At Palito, management anticipate that mine output for 2016 will be between 105,000 and 110,000 tonnes at an average grade of between 8.5g/t and 8.9g/t. The gold production will be supplemented by the processing of the surface stockpiles of ROM ore and the flotation tailings that were generated in 2014. About 1,900 metres of horizontal development work has been completed at the mine during the quarter, of which 1,064 metres was ore development. This rate is consistent with the levels required to maintain an adequate level of production stoping blocks and reflects the rate at which they are depleted.

The installation of the third ball mill is almost complete, along with the second flotation line and enhancements to the carbon in pulp plant. The works are on schedule to be completed this month at a cost of $1.2M. Following their completion it is anticipated that plant processing capacity could be increased from the current levels of around 400 tonnes per day to over 500 tonnes per day. This will be in excess of mine production levels, allowing the stockpiles to be depleted and creating surplus capacity to catch up any lost production caused by unplanned stoppages. The plant expansion is expected to provide sufficient incremental capacity to process most of the stockpiled material of both coarse ore and flotation tails during the remainder of 2016. A carbon regeneration kiln is also being acquired which will assist in enhancing gold recoveries once it is operational in H2.

At Sao Chico, the development of the main ramp is continuing. The immediate priority is to evaluate and define stoping blocks on the first four levels to secure mine production for the next 12 to 18 months. Further ramp development will therefore be progressed to pursue the down-dip extension of the current areas that are in development. The rates of lateral development on existing levels will be increased when the group, through a combination of its current drilling programmes and on-lode development, has greater confidence in the distribution of the high grade mineralisation within the lateral strike extension.

At this time no surface drilling or exploration activities are panned on the group’s properties. Once adequate cash flow is being generated, however, they will step up their exploration activity and will be looking to add to their resource base and production potential by establishing additional satellite high-grade gold mines in relatively close proximity to the current Palito operation which would be a centralised processing facility. Management will continue to evaluate other opportunities in Brazil that it considers could increase the resource base.

The underground development of the Palito mine is being driven towards the Palito South area. In the second half of the year, the group intends to use down-hole geophysics in existing drill holes in the Curretela and Piaui prospects in particular. It is hoped that the results will better define a subsequent evaluation drill programme over these prospects. At Sao Chico, once adequate cash flow is being generated, the group intends to use some of it to advance the exploration opportunities. This is forecast to start early in Q3 when they plan to conduct a ground geophysical survey to the east and west of the Sao Chico deposit with a view to defining the projected strike extension of the main vein.

It is worth noting that after depreciating heavily last year, the Brazilian Real has shown some strength so far this year with the rate increasing by 9% from R3.9042 per dollar to R3.5583 as of the end of Q1.

The group has a $5M loan facility from its main shareholder, Fratelli, of which $2M has been drawn down to date with the rest available to be drawn down before the end of June. There is an additional secured loan facility which is repayable before the end of 2016 which has $4M outstanding against it with the group paying the first instalment at the end of April. The directors anticipate that the group has access to sufficient funding for its immediate needs.

They expect to have sufficient cash flow from their forecast production to finance ongoing operational requirements to repay its loan facilities and in part, to fund exploration and development activity on the other gold properties. The forecasted cash flow projections over the coming year include a significant increase from Sao Chico, however, and the group is of course exposed to changes in the gold price and forex rates. The $2M drawn down under the Fratelli facility is convertible at the election of Fratelli into new shares at an exercise price of 3.6p at any time (the share price is now 4.6p).

There are some 26M options vested but the exercise price is well above the current share price so they are probably not that dilutive. It is worth noting that 12,600,000 have an exercise price of 5p and 18,200,000 have an exercise price of 5.5p, however.

On the 17th May the group announced that it had awarded 15,650,000 new options to employees which represents over 2% of the entire share capital. I am fairly relaxed about this actually as the exercise price is 5p which is above the 4.6p the shares currently stand at.

Overall then this has been a pretty decent quarter for the group. They are now profitable, net assets increased and the operating cash flow grew with some free cash being generated. With costs per ounce of $858 and a sales price achieved of $1,165, the group seems to be decently profitable at these gold prices. The processing plant upgrade is nearing completion which will mean processing capacity is over mining capacity which is a good place to be.

It should be noted that the local currency is recovering which means that costs will be up somewhat but borrowings are not a worry here and as long as the gold price holds up, I think this company could be a good investment, although the potential dilution should they go ahead with a large acquisition should be kept in mind.

On the 16th June the group released an update covering Q2. Gold production from both Palito and Sao Chico followed the trend set by Q1 with gold production expected to be around 9,750 ounces which puts them well on target to achieve the full year guidance of 37,000 ounces.

At Palito, as well as expanding the mine horizontally, they have also had success with some smaller zones within the deposit that can be accessed from existing ramp development. These are adding further improvement to the levels of gold production that can be achieved from each vertical metre. This, in turn, allows them to slow down the rate at which further deepening of the mine is required, meaning that they can replace vertical development with horizontal development generating cost and efficiency benefits as well has helping to increase the life of the mine.

At Sao Chico the group have found a good solution to the geological complexity of the deposit that hindered the extraction rates last year. Mine production continues to focus on the central portion of the Main Vein where they have the greatest confidence in the down-dip extension and they are continuing to push the ramp down towards 84mRL, some 150m below the surface. From there they will establish underground drill locations to assess the further extension at depth as well as the potential strike extensions to the east and west of the Central Zone.

The short term plan at the mine has been to secure production for up to 18 months in advance which establishes an adequate cushion to alloy time for them to concentrate on assessing the potential strike extensions and parallel structures which ensure that they can maximise the benefit of existing development in the longer term. The group has purchased an underground exploration drill rig which has now arrived on site and following commissioning will start on this work.

A Similar programme will also be undertaken at Palito once the initial phase of work is completed at Sao Chico. Initially work will focus on the extension at depth of the main zone but will also look for parallel structures which lie between the main zone and Palito West and Chico da Santa with the expectation that a number of small but viable veins will be identified that can be easily accessed from the existing mine development.

During Q2 the board had anticipated to have a third ball mill commissioned and operating but the failure of a key component in one of the other mills has delayed this start up because they borrowed the bearing from the third mill. A new bearing has now been delivered and the commissioning of the third mill will start in the coming week. This was a lucky coincidence and illustrates the requirement for building contingency and flexibility when operating in remote locations.

Whilst the focus for 2016 is to use cash flow to retire the borrowings that the company has with Sprott, they have been able to set aside some funding for the start of the next stages of wider exploration activity at the two mines. This will involve a down the hole electromagnetic survey at Palito using the past drilling undertaken at the Curretela and Piaui prospects. The contractor is due to arrive on site in July and they anticipate that the programme and subsequent evaluation of results will take around three to four months to complete. It is intended that this work will allow the group to better plan the next stage of exploration drilling that is expected to be undertaken in 2017.

At Sao Chico a surface induced Polarisation programme will be undertaken over an area to the west of the original exploration tenement. Results are expected to be available towards the end of 2016. Borth geophysical programmes are using well established techniques to identify conductive bodies and sulphide mineralisation as pathfinders to locating gold occurrences which are associated with these features.

Whilst many economic commentators expected to see the Brazilian currency continue to decline during 2016, in the face of an uncertain political climate and a weakening economy, it has confounded expectation and strengthened. It appears that there remain strong inflows of currency into the country and while these may include investment from multinational companies to support their local businesses, this will place pressure on the group’s reported dollar costs should the situation continue. At this time it remains unclear how the political situation will resolve itself and how this will impact on the perceptions of Brazil but neither this, or the concerns over Zika are currently having an impact on group operations.

The board will continue to look at the opportunity for potential acquisitions of other projects. The recent surge in gold prices has started to change seller expectations. The board are keen to grow the company but will only consider acquisitions that they feel will genuinely increase value for shareholders. While a strong market is good for the group, they are concerned that some valuations and expectations may become unrealistic.

Overall then, it seems decent progress is being made. I am still a little concerned about an equity raise in the event of an acquisition and the situation in Brazil, in particular the strength of the Real need to be taken in to consideration but I have decided to take a position here.

On the 18th July the group released an operating update covering Q2. Total production was 9,896 ounces of gold, compared to 9,771 ounces in Q1, generated from the processing of the ROM ore from Palito and Sao Chico combined with the Palito surface coarse ore and stockpiled flotation tailings. The production came from the processing of 39,402 tonnes of hard rock ROM with an average grade of 8.17g/t which is a bit lower than the 8.58g/t in Q1 and the 8.36g/t in H1 last year. The total mined ore for the same period was 33,606 tonnes at 9.56g/t, lower than the 11.02g/t in Q1 and 9.85g/t in H1 2015, and this is split with 25,198 tonnes at 10.48g/t from Palito (10.17g/t in H1 2015) and 8,408 tonnes at 6.81g/t from Sao Chico (significantly lower than the 9g/t in Q1 and 8.47g/t in H1 last year). Additionally, 6,354 tonnes of flotation tailings with a grade of 2.7g/t was processed through the cyanidation plant.

At the period-end there were coarse ore stocks of about 12,000 tonnes with an average grade of 5g/t and about 25,000 flotation tails at 2.5g/t. The plant expansion, with mill number three now operational, is virtually complete and will provide sufficient incremental capacity to process most of this stockpiled material during the rest of the year. A second flotation line and enhancements in the CIP plant are also close to completion and the carbon generation kiln acquired earlier in the year is now being installed and will be commissioned in Q3. This kiln will regenerate fouled carbon and enhance gold recoveries.

There was a short delay in the commissioning of the third ball mill following the failure of a main bearing in mill number two, but they were fortunate to be able to use the identical bearing from the third mill to keep the plant at full operational capacity which delayed its commission by about a month. It is now operational – the group have been rather lucky here!

About 1,900 metres of horizontal development has been completed during the quarter at Palito, of which 943m is represented by ore development with the balance being on the development of ramps, cross cuts and stope preparation.

At Sao Chico, a total of 1,031 metres of horizontal development was completed, of which 598m represented ore development, with much of the balance being ramp development and cross cuts reflecting the ongoing deepening of the mine. Most of the 8,408 tonnes produced from the mine has been generated from development mining but there will be a greater contribution of ore coming from production areas during H2. They have now secured the source of production up to the end of 2017.

Additionally underground exploration drilling at Sao Chico has started. The purpose is to test the down dip continuation of the central ore shoot below the 100mRL as well as to the east and west along strike, areas which remain quite open. The first drill hole completed in the past week recorded an intersection of 46.2g/t over a drilled width of 2.32m, located about 240m from the surface and 100m down-dip from the current lowest developed level – this seems impressive.

The company expects to produce 28,000 ounces of gold during the year with the processing of Palito ROM and stockpiles. With the Sao Chico mine now under development, they also anticipate production of 9,000 ounces of gold from ore mined at Sao Chico so as a result, with nearly 20,000 ounces produced in the first half, the board remain confident of achieving its production forecast of 37,000 ounces.

Whilst they have forecast an all-in sustaining cost of between $840 and $870 per ounce, this guidance was predicted on a significantly weaker Brazilian Real at the beginning of the year. The currency has strengthened against the US dollar by about 20% since then, much of which occurred in Q2, and this will impact on reported costs. Apparently there is a prediction of a weaker Real in the second half of the year but this is something that needs to be kept an eye on.

Overall then things seem to be ticking a long OK, certainly as far as quantities are concerned. The fall in Sao Chico grades is a bit of a concern but more of a worry I think is the appreciation of the Brazilian Real which will likely increase costs. Thankfully the price of gold has also increased so if this can be sustained the group is set quite well. I now hold the stock.