Vertu Motors has now released its final results for the year ended 2016.

Revenues increased when compared to 2015 with a £121.3M growth in used car revenue, a £117.1M increase in new car revenue, an £89.1M growth in new fleet and commercial revenue, and a £20.9M increase in after sales revenue. Cost of sales also grew to give a gross profit £35.2M above that of last year. Wages & Salaries were up £17.3M, depreciation increased by £888K, operating leases were up £2M and other operating expenses grew by £9.4M which all meant that the operating profit grew by £5.5M. Vehicle stocking interest costs were up £735K and tax increased by £823K to give a profit for the year of £20.7M, a growth of £4.1M year on year.

When compared to the end point of last year, total assets increased by £205.8M, driven by a £121.7M growth in new vehicle inventory, a £24.7M increase in cash, an £11.8M growth in used vehicle inventory, a £14.3M increase in goodwill, a £6.6M growth in trade receivables and a £12.9M increase in the value of land and buildings. Total liabilities also increased during the year due to a £157.9M growth in trade payables, a £13.9M increase in long term borrowings, a £6M growth in advance payments from finance partners and a £5.6M increase in accruals, mainly relating to an increase in outstanding service plans. The end result is a net tangible asset level of £127M, broadly flat year on year.

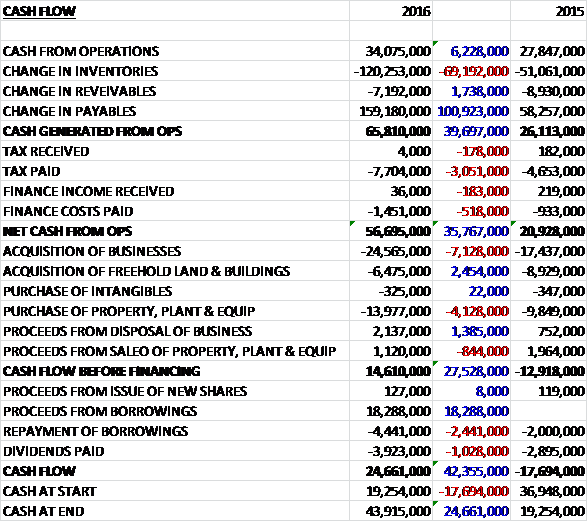

Before movements in working capital, cash profits increased by £6.2M to £34.1M. There was a cash inflow from working capital, with a very large growth in payables and after the group paid out £3.1M more in cash and £518K more in finance costs, the net cash from operations came in at £56.7M, a growth of £35.8M. The group spent £14M on fixed tangible assets, £24.6M on new businesses and £6.5M on freehold land and buildings and even after this there was £14.6M of free cash flow. Some £3.9M was spent on dividends but a net £13.8M of new borrowings was taken out to give a cash flow for the year of £24.7M and a cash level of £43.9M at the year-end.

The gross profit in the aftersales business was £102.9M, a growth of £13.5M year on year. The group now has over 89,000 customers paying monthly for service via the three year service plan product compared to 71,031 last year. In addition, significant numbers of service plans operated by manufacturers are also in place. The total of these plans are helping the group to take market share from the independent aftersales market in the service area and drive consistent servicing growth. Furthermore the group has sold over 30,000 Motability vehicles in the last three years, each of which is on a three year service arrangement, adding a further resilient income stream.

Service revenues rose 6.5% on a like for like basis and aftersales margins strengthened from 43.5% to 44.8%. The improvement in aftersales margins has been achieved in each of the service, parts and accident repair centre activities as a result of a focus on the detailed operational performance in each department. The accident repair centre sector delivered another year of improved revenue and margins as demand has started to outstrip supply in the channel. Accident repair centre revenues grew 8% on a like for like basis and margins improved to 66.2% with eleven accident repair centres now being operated. Supply of manufacturer parts continues to be a vital part of the franchised dealer model. Parts revenues rose 5.5% of a like for like basis and margins improved to 23.3%.

The gross profit in the new car retail business was £59.3M, an increase of £8.4M when compared to last year. New retail car volumes sold rose by 4% on a like for like basis compared to an increase of 3.9% in UK private car registrations. The outperformance was weighted to the second half of the year when the group’s new car registrations grew by 7.3% against the market which grew 4.7%. Volumes of sales on the Motability scheme rose by 1.6% on a like for like basis against a 2.9% decline in the UK market as a whole, helping to earn the group the title of Motability Dealer of the Year. Gross profit per unit rose to its highest ever level in the second half of the year due to the growing mix of premium sales and retail sales growing faster than the lower-margin Motability sales.

The gross profit in the new fleet and commercial business was £17.6M, a growth of £5.3M when compared to 2015. The group has significant fleet operations and a shift in sales mix away from supply to lower margin daily rental channels resulted in continued improved margins and slightly lower volumes. Consequently their like for like car fleet volumes fell by 4.2% while margins improved. In the light commercial vehicles sales channel, the group’s like for like volumes of commercial vehicles increased by 22% during the year reflecting continued market share gains against UK registrations up 13.2%. Margins in fleet and commercial sales improved from 2.5% to 3% and are now at record levels.

The gross profit in the used car business was £83.5M, an increase of £8M year on year. The strong like for like growth in used vehicle volumes of 8% was significantly ahead of the market. This strong growth in like for like volumes accelerated in the second half of the year, up 12.2%, reflecting both the inherent strength of the group in used cars through sales and stock management processes and the impact of more effective marketing, both on line and offline from October onwards. During the year the group adopted a more centralised approach to used car marketing and increased TV advertising and more nationally co-ordinated campaigns. The impact of this approach has been to improve sales volumes and profitability.

The group’s used car gross margin was 9.8% compared to 10.4% last year and gross profit per unit was down from £1,190 to £1,165. The slightly lower margin effect was more than offset by higher volumes and related to the increased premium content within the group.

The group increased its investment in like for like advertising expenditure during the year by £2M which saw a shift towards TV and online and away from press reflecting shifts in consumer behaviour.

As can be seen, there was a significant cash inflow through working capital during the year. The major components of this movement were lower VAT payments due to the increase in new vehicle consignment inventory levels leading to more input VAT being reclaimed (£14.4M), accelerated receipts from customer finance partners (£6M), reductions in fully paid vehicle inventories as manufacturers reconfigured their supply chains (£4.4M), and increase in service plan receipts from customers as the number of service plans increased (£2.2M). The board does not expect this to be the normalised position for cash generation and it is possible that some of these amounts may reverse in future periods as vehicle flows from manufacturers evolve.

Several of the group’s manufacturer partners are currently increasing their dealership size and facility requirements and are therefore encouraging retailers to redevelop dealership premises. Consequently the group anticipates that expenditure on current dealership redevelopment projects will be about £11M in 2017. In addition, planned new dealership developments including freehold purchases totalling £16.5M are also anticipated which will add further capacity to the group’s operations.

The company is currently rolling out a group-wide, in-house developed showroom system built around the use of computer tablet technology by sales teams. This will be rolled out by the end of September and has contributed to increased levels of IT expenditure in the year. The system is anticipated to increase the efficiency of the sales process and deliver enhanced customer service.

As usual there have been a number of acquisitions during the year. In May the group acquired the Bury Land Rover outlet from Pendragon for a total cash consideration of £7M, generating goodwill of £4.4M. Also in May they acquired Bradford Jaguar from Lancaster for a cash consideration of £825K, generating goodwill of £750K. In June they acquired Blacks Autos, who operated a Skoda dealership in Darlington, for a cash consideration of £1.8M, generating goodwill of £765K. Had this acquisition occurred in March, profits would have been £88K higher. In October they acquired SHG Holdings, who operate various VW outlets in Herefordshire and Gloucestershire.

There was a cash consideration paid of £12.9M with a further deferred consideration of £1.5M payable two years after the acquisition date. This acquisition generated goodwill of £7.8M and had the acquisition occurred at the start of the year, profits would have been £1.3M higher.

In December the group acquired Who’s Ace Holdings, an online vehicle parts business. There was no consideration paid but the business did have net borrowings so goodwill of £314K was generated. The business is still loss making so had the acquisition occurred at the start of the year, group profit would have been £154K lower. In January 2016 the group acquired three Honda dealerships in Stockton, Nottingham and Derby from Lookers for a total cash consideration of £2.1M, generating goodwill of £170K. Many of the acquisitions undertaken in recent periods are still to become fully established in margin terms which provides the group an opportunity to deliver improved margins and grow organic profit.

In April the group disposed of its petrol forecourt at Walkden and in September they disposed of a service station in Horwich. Both included freehold properties and were acquired with the Bolton and Wigan Ford businesses in November 2014. In July the group disposed of its Peugeot operation in Dunfermline. In all, these disposals brought in a consideration of £2.1M, broadly similar to the carrying value of their assets.

After the year-end the group acquired Sigma Holdings which operates three Mercedes dealerships in Reading, Ascot and Slough. The total consideration paid was £21.9M, consisting of about £18.4M settled in cash and £3.5M of deferred consideration due over the next year. In addition, vendor shareholder loans of £9M were settled in cash on completion with £13M of goodwill being generated. In March the group announced that they were raising £35M through a placing of 56M new shares at a price of 62.5p per share. Finally, in May 2016 the group acquired Leeds Jaguar from Inchcape for a consideration of £650K, including goodwill of £500K.

The group is somewhat susceptible to uncertainty surrounding the Brexit vote and is maintaining contact with its manufacture partners in Europe so this is something that should be considered.

The group have announced that Pauline Best is joining as a non-executive director. She is an HR professional who is currently the global people and organisation director of Specsavers.

The group has traded ahead of the current year financial plan, and last year, in March and April. Increasing sales and a strong aftersales performance, together with an increased contribution from recently acquired dealerships are enabling the group to drive profits. In the period since the year-end, aftersales margins rose to 46.7% with like for like revenue increases. Service like for like revenues rose 7% and continued to benefit from the successful customer retention initiatives being executed by the group and overall aftersales profitability increased on a like for like basis.

After the year-end there was a continuation of growth in the UK private new car market. In the period the group has seen stable new retail volumes and a slight decline in gross margin. They have seen strong growth in fleet and commercial volume margins, however, and overall the profit contribution from new vehicle sales in retail and business channels is flat on a like for like basis.

The group’s like for like used vehicle retail volumes were up 5.9% in the post year-end period. The impact of the changes made to the group’s marketing in the second half of last year along with a continued focus on the management of used vehicle inventory have contributed to this performance. Used vehicle margins were stronger during the post year-end period which has led to a significant increase in year on year profitability. Given trading in March and April and the improvements seen in the acquired businesses, the board remains confident about the group’s prospects for the current year.

If we add on the new shares placed after the year-end, at the current share price the shares trade on a PE ratio of 11.1 which falls to 9.7 on next year’s consensus forecast. After a 23.8% increase in the total dividend, the shares are yielding 2.3% which increases to 2.6% on next year’s forecast. At the year-end, the group had a net cash position of £23.1M compared to £15.7M at the end of last year, although given the timing of sales I suspect this figure is a rather flattering view of group cash.

Overall then this has been a good year for the group. Profits increased, net tangible assets were flat and the operating cash flow grew, and aided by favourable working capital movements that will likely reverse at some point in the future, there was plenty of free cash generated. All parts of the business performed well, particularly in the second half of the year as improved marketing drove a great performance in the used car business.

Going forward, there is a lot of manufacturer-driven capex requirements that need to be paid for and it is a bit disappointing to see the group having to resort to placings for their acquisitive needs – I would much rather see a company grow its business out of operating cash flow. In the start of this year, performance has been ahead of plan but this seems to be acquisition-led and new car sales were only flat which is a bit of a concern. Still, with a forward PE of just 9.7 and a fairly respectable dividend yield of 2.6%, these shares look decent value to me and I am tempted to get back in here.

On the 1st June the group announced the acquisition of Gordon Lamb for a total cash consideration of £18.7M which has been settled from existing cash resources. The business operates a Toyota, Land Rover, Skoda and Nissan outlets in Chesterfield along with a Skoda dealership in Derby. The transaction generated goodwill of £8.3M and last year the business generated pre-tax profits of £2.7M with the board expecting the deal to be earnings enhancing in its first full year of ownership. This looks to be a good acquisition to me.

On the same date the group announced that Pauline Best joined the board as a non-executive director. She has over thirty years of HR experience and is currently global people and organisation director at Specsavers.

On the 15th May the group announced that CEO Robert Forrester purchased 54,700 shares at a value of £29K which gives him a total of 6,767,673, so just a token buy it looks like then.

On the 29th June it was announced that Chairman Peter Jones purchased 117,000 shares at a value of about £50K. He now owns a total of 1,522,000.

On the 20th July the group released a trading update covering the first four months of the year where the board reiterated that they expect the performance for the full year to be in line with current market expectations.

Profitability in the four month period was ahead of the prior year and in line with board expectations. Group revenues have increased by 21.5%, aided by higher revenues from acquired dealerships and continued organic growth with like for like revenues up 8.4%. Total gross profit increased by 23.6% with like for like gross profit increasing by 8.7%.

The aftersales operations continued to grow strongly with gross profits up 25% in the period, an increase of 7% on a like for like basis. The group’s retention initiatives such as service plan sales, the focus on customer service, and increases in the overall vehicle parc positively contributed to these profitability trends. In vehicle servicing, the group increased total service revenues by 25% and like for like service revenues by 6% whilst improving like for like service margins from 75.8% to 76.6%.

Used vehicle performance also continued to be very strong in the period with the group delivering total volume growth of 19% and like for like growth of 10%. Performance was aided by continued investment in marketing and by the timing of sales events compared to the prior year. The gross profit generated from used vehicle sales rose 27% with a growth of nearly 18% on a like for like basis reflecting strong price discipline and the underlying strength of residual values in the UK used car wholesale markets. The increase in new car PCP business, where the manufacturer guarantees the residual value of the car has provided stability in prices.

During the period the UK new retail market has been stable after a period of sustained growth. Whilst private registrations saw growth in March, the market has softened with small declines seen in April, May and June. The group’s total new retail sales volumes grew by 9% but like for like sales reduced by nearly 4% with volume franchises seeing declines in volumes whilst premium franchises saw growth. The UK remained an attractive market for the manufacturers and supply push of product into the market continued, although whether this will be the case following the weakening Sterling remains to be seen.

The group has seen growth in its car fleet operations during the period, with total volumes higher by 7.5% and like for like volumes increasing by 3%, compared to an increase in UK fleet registrations of 6%. Group sales of new commercial vehicle sales volumes grew by 27.5% and like for like new commercial sales grew by 25%. UK commercial vehicle registrations grew by 4.3%, showing that the group continued to take market share in this market. They grew like for like gross profit from their fleet and commercial operations by nearly 18% with overall profitability in the channel up significantly.

In March the group purchased Greenoaks, which operates three Mercedes dealerships, for £21.9M alongside the settlement of £9M of shareholder loans. These dealerships in Ascot, Reading and Slough have historically underperformed but the board are pleased with the progress made to date to integrate and improve the performance of the businesses and they have traded in line with the performance targets put in place at the time of the acquisition.

In the period the group has undertaken three further transactions which represent a deployment of a substantial proportion of the raised capital. In May they acquired Leeds Jaguar for £700K, generating goodwill of £500K – this business broke even last year. In early June the group acquired Gordon Lamb, a group which operates five sales outlets in Derbyshire. This acquisition introduced the Toyota franchise to the group and added a sixth Land Rover dealership together with two Skoda and a Nissan outlet. Total consideration amounted to £18.7M including an £8.3M payment for goodwill. For 2015, the business showed adjusted pre-tax profit of £2.7M. In Late June the group acquired the freehold and long leasehold interests in two Honda dealerships they operate in Nottingham and Derby for a consideration of £3.2M.

Obviously the Brexit vote has led to some uncertainty for the economy and the motor retail industry in a number of areas. Regulations surrounding manufacturer franchise contracts are currently determined on an EU basis and reflect EU competition policy. The board doesn’t anticipate any major changes to this contract position resulting from the vote, however.

The UK represents the second largest market for new vehicles in the EU so the board believe that manufacturers are likely to be keen to support UK retailers through any period of uncertainty. The majority of the group’s new vehicle sales are imported from the EU. The manufacturing partners clearly have a vital interest in ensuring continued free trade access to the key UK market and negotiations will be monitored closely. The Euro/Sterling exchange rate is important to manufacturer profitability on the UK sales and is a factor in determining the level of supply push of vehicles to the UK market. Whilst sterling has declined against the Euro, it remains at levels above the lows seen in 2009 and throughout much of 2013, at levels which the board believes remain attractive for EU manufacturers.

It is likely that business and consumer confidence in the UK may also come under pressure. In line with trends in recent months, since the referendum new vehicles sales volumes have been behind last year but used cars and aftersales have mitigated any negative impact to date.

Overall then, this is an interesting situation. The performance of the group has clearly been very strong with growth almost everywhere – except new car sales which are suffering following the Brexit vote. Whether this will continue and filter down eventually to the other businesses at the group really define whether this is viewed as a good investment at the moment. I am starting to think the share price decline has been rather over-done and I am tempted to take a nibble here.

On the 1st September the group released a trading update where they stated that full year results are expected to be in line with market expectations. Aftersales and used cars have continued to grow but SMMT data has shown UK private new retail vehicle registrations softening since April and the board expects this trend to continue. September order intake levels on new vehicles reflect continued growth in the fleet and commercial sector and a continuation of the softening in the private retail new car channel.

The macroeconomic environment of low interest rates and high levels of employment provide a favourite backdrop for the sector but weaker exchange rate levels for Sterling create uncertainty around future manufacturer strategies towards new car pricing. The Brexit result has to date not impacted consumer confidence as adversely as some were predicting and the group has not experienced any significant change in customer behaviour. The board is pleased with the performance of the recently acquired dealership and with the integration of them into the group.

Overall, this is a fairly decent update although the slow-down in new car sales is a potential concern, along with whether European manufacturers will continue to target the UK now that Sterling has depreciated.