Serabi Gold has now released its final results for the year ended 2016.

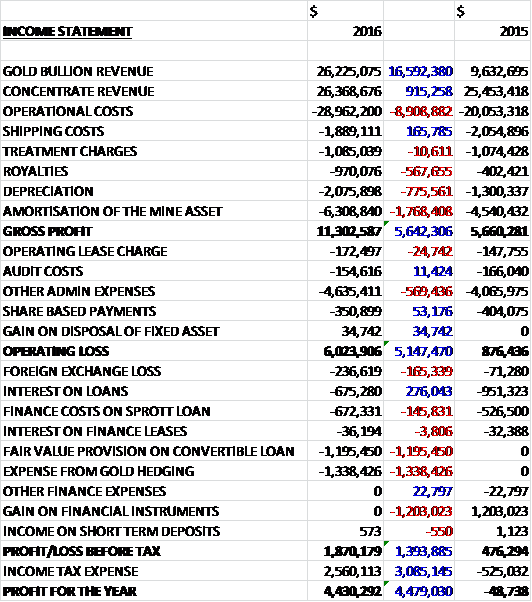

Revenues increased when compared to last year with a $16.6M growth in gold bullion revenue and a $915K increase in concentrate revenue. Operational costs increased by $8.9M due to growing labour costs and the fact that Sao Chico only entered commercial production at the start of 2016, royalties were up $568K, depreciation increased by $776K and amortisation grew by $1.8M to give a gross profit $5.6M above that of last year. Admin expenses increased by $570K reflecting expenses for old tax settlements which meant that the operating profit was up $6M. We then see a $1.2M fair value provision on the convertible loan as the group’s share price increased, a $1.3M expense from gold hedging and the lack of a $1.2M gain on financial instruments which occurred last year, offset by a $3.1M positive swing to a tax income as tax losses were recognised. The end result was a net tangible asset level of $4.4M, an improvement of $4.5M year on year.

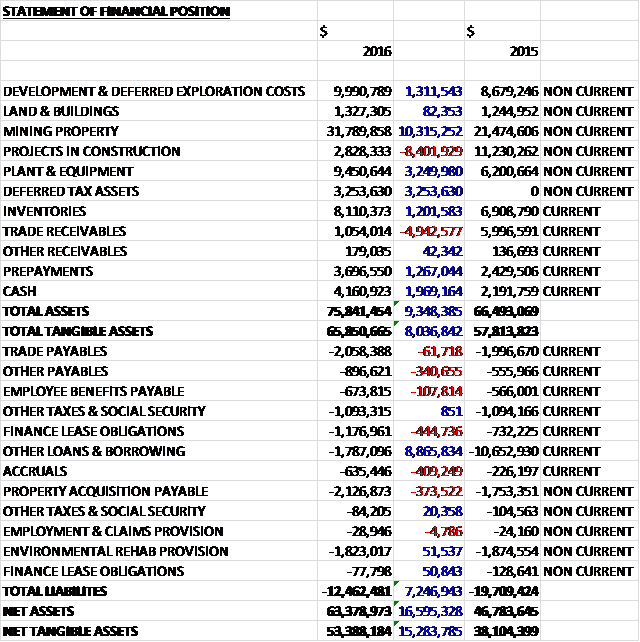

When compared to the end point of last year, total assets increased by $9.3M driven by a $10.3M growth in the value of mining properties, a $3.2M increase in plant and equipment, a $3.3M growth in deferred tax assets and a $2M increase in cash, partially offset by an $8.4M decline in projects in construction and a $4.9M fall in trade receivables relating to the new contract with a new customer for concentrate sales. Total liabilities declined during the year, mainly due to an $8.9M decrease in other loans and borrowings. The end result was a net tangible asset level of $53.4M, a growth of $15.3M year on year.

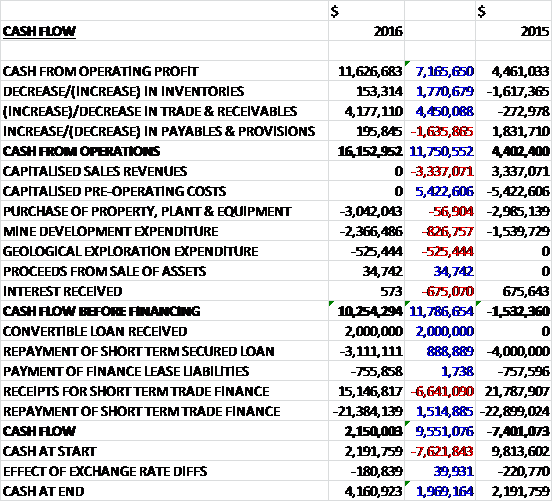

Before movements in working capital, cash profits increased by $7.2M to $11.6M. There was a cash inflow from working capital and the cash from operations came in at $16.2M, a growth of $11.8M year on year. The group spent $3M on property, plant and equipment, $2.4M on mine development expenditure and £525K on geological exploration which meant that the free cash flow was $10.3M. Of this, $3.1M was used to pay back the short term secured loan, $756K went on finance lease payments and a net $6.2M went on the repayment of short term trade finance. After a $2M convertible loan was received, the cash flow for the year was $2.2M and the cash level at the year-end was $4.2M.

With the Palito and Sao Chico mines now operating at planned levels and 40,000 ounces of gold production forecast for 2017, the focus is now on evaluation of the existing discoveries and other exploration opportunities that exist around both mines and successful development of these will bring a further opportunity to increase production.

Total gold production for Q4 was 9,413 ounces, making the total gold production for the year 39,390 ounces, representing a 21% increase over 2015 with Sao Chico not yet in production in Q1 2015 and commercial production starting at the start of 2016. The ore generated from Sao Chico in 2016 has continued to be derived principally from development operations rather than stoping, although this is now changing.

About 158,900 tonnes of ore was extracted in 2016 compared to 135,800 in 2015. The introduction in Q2 2016 of increased processing capacity eliminated limitations in the amount of ore that can be processed and allowed the increased levels of ore from Sao Chico to be accommodated. The mine production for Q4 2016 from Palito was some 28% higher than Q4 2015.

Average mined grades in Q4 at Palito were lower than in preceding quarters as a result of ore being cemented in two stopes. The production shortfall was partially compensated by increased production of development ore at a lower grade. Overall the mined grade at Palito averaged 9.62g/t for 2016, a reduction of 4% year on year.

At Sao Chico mined grade in Q4 2016 was 14.38g/t which is 48% higher than Q4 2015. This ore grade is considered to be a one-off event reflecting particularly high-grade areas that were being mined in the quarter and management consider that the normal mined grade at the mine will be between 9 and 10g/t over the life of the mine. The average grade in 2016 as a whole was 10.12g/t, an improvement of 17% over 2015. The improvement reflects the fact that during 2015 Sao Chico was primarily in development and higher grade ore from stoping operations only started to be produced in Q2 2016.

At Palito the group focused on opening up new sectors in the mine as well as continuing to develop the existing sectors. With four sectors now being developed underground at the mine, during 2016 the group has completed about 7,350m of horizontal development, representing an increase of 8% over the prior year.

The Senna zone is now in underground development and to date has been very successful. Mine development is ongoing and all ore being mined from the sector is currently from development activity with stoping yet to start. Based on the ore grades recovered from the earlier open pit operation and deeper exploration drill holes, management is hopeful of the long term potential within the zone which has the benefit of an independent access from the surface.

In the Chico da Santa sector, the 114mRL has been developed on the Ipe, Jatoba and Mogno veins. Good grades have been encountered in all three veins, although they tend to be slightly narrower than the veins being mined elsewhere at Palito. The development towards Palito South has not been advanced significantly during the year as it is awaiting underground diamond drilling to test the down-dip continuity of the G3 vein at depth. Management hopes that subject to available cash resources, a drilling programme can be undertaken in 2017 to evaluate the area further.

Underground drilling is being used to evaluate numerous known but underexplored veins and together with these two sectors, the group hopes to open up numerous new mining faces in the upper levels. These have the advantage of being in close proximity to existing mine infrastructure and will not require any new ramp development.

At Sao Chico the main ramp has now reached the 71mRL, about 170m below the surface, and will continue to be deepened during 2017. During the year the decision to implement sublevel open stoping as the main mining method was taken which resulted in the development of sublevels with 12m vertical spacings floor to floor.

The gold grades within this alteration zone are quite erratic and are hosted in three steeply plunging pay shoots. Outside the pay shoots the vein is continuous but with low gold grades and as a result it will be unavoidable that as the mine development passes between the pay shoots, lower grade ore has to be mined. The central pay shoot is the most established of the three high grade shoots and is some 100m long. The group has focused on developing this part of the main vein and some consistent higher grade development ore is being generated as a result.

During Q2 the group started underground exploration drilling of the central pay shoot targeting its down dip extension. The drilling has intersected the Main Vein in all holes and is confirming the belief that the Sao Chico main vein is a regional shear structure. This bodes well for the continuation and strike extension outside the immediate and current mine limits.

The gold production of 39,390 ounces this year came from the processing of 158,966 tonnes or ore with an average grade of 8.11g/t compared to 130,299 tonnes at 8.43g/t last year reflecting the increased levels of ore being produced at Sao Chico.

Further improvements undertaken within the process plant during 2016 have included the installation of additional flotation capacity and automation, along with new carbon screens within the CIP tanks to improve the inter-tank flow rates. A carbon regeneration kiln was installed, commissioned and became operational during Q4 which will regenerate fouled carbon, reducing the need to purchase fresh carbon and is also expected to enhance gold recoveries.

Milling rates for ROM ore have increased by 22% to 435tpd. The introduction of the third ball mill at the end of June has had a significant impact on throughput rates. The average daily rate was 460tod in H2. The increase in processing rates also reflects the improvements in the operational efficiency of the process plant which have been assisted by the introduction of the gravity circuit and ILR for treating Sao Chico ore, reducing the levels of gold that would otherwise have been treated in the CIP circuit. This improved efficiency has also allowed the rate of processing of the flotation tails to be maintained at similar levels to 2015. As of the year-end there were about 20,800 tonnes of flotation tails with an average grade of 2.5g/t waiting to be processed.

Much of the group’s expenditure is incurred in Brazilian Reais and they therefore have significant exposure to the changes in exchange rates. Whilst the 20% strengthening of the Real between the beginning and end of 2016 has negatively impacted on the performance, when looking at the unit costs of production compared with 2015, the underlying trend has been for an overall reduction in unit costs when look at in local currency terms. The total all in sustaining cost of production during the year was $965 per tonne compared to $892 per tonne in 2015.

At Sao Chico in the second half of 2016 the level of stoping activity began to increase and the long term balance between developing mining and stoping rates only started to be reached at the end of the year. During 2017 management expects that monthly development and production rates will continue to stabilise. The group is driving development galleries east and west towards additional ore shoots that have been identified by surface drilling.

Management is confident that these ore shoots will provide additional mineable ore at Sao Chico. Underground drilling is being undertaken for short term operational and mine planning purposes with a second parallel campaign being undertaken to test the deeper resource potential of the deposit.

Mine-site geophysical studies undertaken during Q3 over the Currutela and Piuai discoveries and other areas close to the current Palito mine have been designed to improve the drill targeting of a planned 2017 surface drilling campaign. Management feel that this drilling campaign could prevent sufficient confidence to justify commencement of new mine portals and underground exploration development drives to access and fully evaluate any new discoveries that are considered to be potentially commercially viable. In time these discoveries could become established as new near-mine satellite deposits adding incremental production.

The group started the first phase of an increased exploration effort during the second half of the year with some initial geophysics programmes around the two mines. The results at Palito from the down the hole electromagnetic programmes have helped them better understand the size and location of existing discoveries and will help them plan the next phase of evaluation those. At Sao Chico the work was suspended because of weather conditions but the initial signs have been encouraging and continue to support the belief that the current Sao Chico mine is just a small part of a larger regional structure. In this respect, the acquisition of the exploration rights during 2016 over exploration tenements surrounding the current Sao Chico operations was very important.

Whilst currently the immediate focus of management is to evaluate the near-mine potential within two to three km of its existing operations, on a wider regional basis the group is developing plans to progress the evaluation of its whole tenement package. They have flown about 14,650 hectares of airborne VTEM surveys but has had limited funds to follow up on many of the areas of interest that were highlighted. Conscious that the exploration tenements it holds are only granted for limited terms, the group is keen to implement, as and when funding is available, a regional exploration programme to highlight the tenement areas that have the highest potential.

As consideration for an extension of the repayment terms agreed with Sprott in January the group granted to Sprott call options to acquire 2,500 ounces of gold from the company at a price of $1,125 per ounce, exercisable at any time up to June 2017. The grant of the call options and its settlement occurred within the financial period and the group has recorded for the value of the cash settlement due as a finance expense in the income statement.

During the year the group repaid $3.1M in capital repayments as well as $150K of a total amount of $433K relating to a cash settlement liability for call options over 2,500 ounces of gold which were granted to and exercised by Sprott during the year.

In August the group issued 42.3M new shares following the decision of Frateli to convert its $2M convertible loan into shares. Under the terms of the loan they had the right to convert the shares at 3.6p per share. The group anticipates that while it may seek to raise further finance in the future it now has access to sufficient funding for its immediate needs.

Going forward the group is currently forecasting gold production for 2017 to be approximately 40,000 ounces with all in sustaining costs expected to be between $950 to $975 per ounce. The group’s cost profile is subject to change as a result of exchange rate variations. At the current share price the shares trade on a PE ratio of 9.6 which falls to 4.5 on next year’s consensus forecast.

Overall then this has been a year of consolidation as the Sao Chico mine finds its feet and starts contributing to the group result. Due to this, profits were up, net assets increased, aided by the strengthening of the Real and the operating cash flow improved with decent levels of free cash being generated. This year the group produced just under 40K ounces of gold at a cost of $965 per ounce, and this is broadly what they expect to do again in 2017.

The Q4 grades are a bit of a red herring with the Palito grade temporarily lower and the Sao Chico grade temporarily higher. A lot depends obviously on the price of gold but also on the strength of the Real with further appreciation making costs rise to uncomfortable levels. Overall though, I like the calm exploration strategy here and with a forward PE of 4.5 this looks pretty good value to me.

On the 12th April the group released details of progress in Q1. It was a strong quarter with production of 9,861 ounces of gold, in line with guidance. Mine production totalled 36,918 tonnes at 10.12g/t and 46,663 tonnes of ore was processed through the plant at a combined grade of 7.09g/t. As of the period-end there were coarse ore stocks of about 13,000 tonnes with an average grade of 4g/t and about 17,000 tonnes of flotation tails with an average grade of 2.5g/t. This stock is not being consumed as quickly as forecast and for now the operation remains plant constrained.

The grade of 12.64g/t achieved at Sao Chico was well above the 10.12g/t average achieved last year but was below the 14.38g/t achieved in Q4, perhaps suggesting it is moving away from the high-yield area. At Palito the grade was 9.07g/t which was above the 7.38g/t achieved in Q4 last year but below the 9.62g/t average.

Ore development and production from Sao Chico continued in line with schedule and good mined grades, at an average of over 12g/t, was achieved for the quarter. The main ramp has now reached the 56mRL with the main vein being intersected early in April. Stope ore production is currently focused on the 140mRL whilst development is progressing on five levels below and is ahead of stoping activity.

Due to the wet season arriving early, the exploration programme at Sao Chico had to be suspended but initial results that have become available are promising. The survey was designed to traverse the known orebody to provide focus to the east and west of the current strike.

The results to date show two good anomalies 600m to the north and 300m to the south of the current workings which look even stronger than the orebody being mined. These anomalies appear to suggest a geometry consistent with the known orebody and could suggest parallel mineralisation. They are set to recommence the programme this coming quarter.

Exploration and evaluation drilling underground continued with about 1,950 metres of diamond drilling completed. This is focusing on deeper drilling into inferred resources in the Senna, Pipocas and G3 veins in the Palito orebody, and similarly the down dip extension of the main vein in the Sao Chico orebody with a view to converting substantial inferred resource to indicated status.

Overall things seem to be ticking along fairly well and I now hold the shares.