TT Electronics has now released its final results for the year ended 2016.

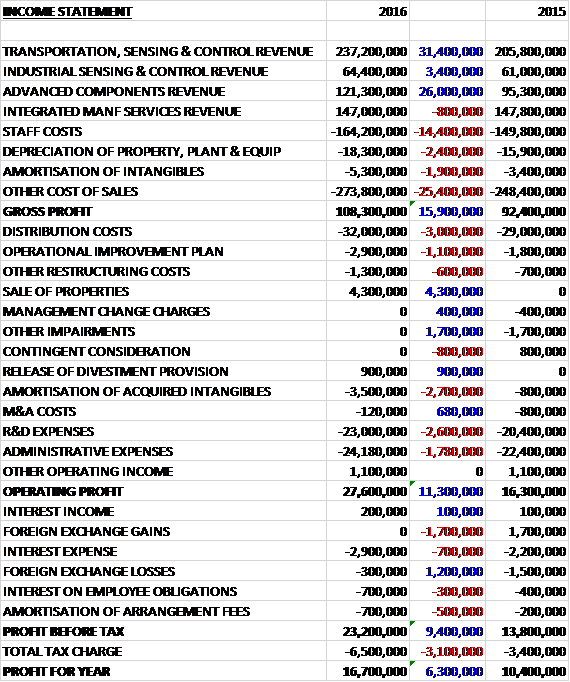

Revenues increased when compared to last year, entirely due to forex movements and the acquisition (they were otherwise flat) as an £800K decline in IMS revenue was more than offset by a £31.4M growth in transportation, sensing & control revenue; a £26M increase in advanced components revenue and a £3.4M growth in industrial sensing & control revenue. Staff costs increased by £14.4M, depreciation was up £2.4M, amortisation increased by £1.9M and other cost of sales grew by £25.4M to give a gross profit £15.9M above that of last time. We then see distribution costs up £3.3M, R&D expenses increasing by £2.6M and other underlying admin expenses up £1.8M. In addition there was a £1.1M growth in costs associated with the operational improvement plan, a £600K increase in other restructuring costs and a £2.7M increase in the amortisation of acquired intangibles offset by a £4.3M profit on the sale of a property and a £1.7M reduction in impairments. All of which meant that the operating profit grew by £11.3M. Interest expenses increased by £700k due to the higher level of debt and tax charges were up £3.1M to give a profit for the year of £16.7M, a growth of £6.3M year on year.

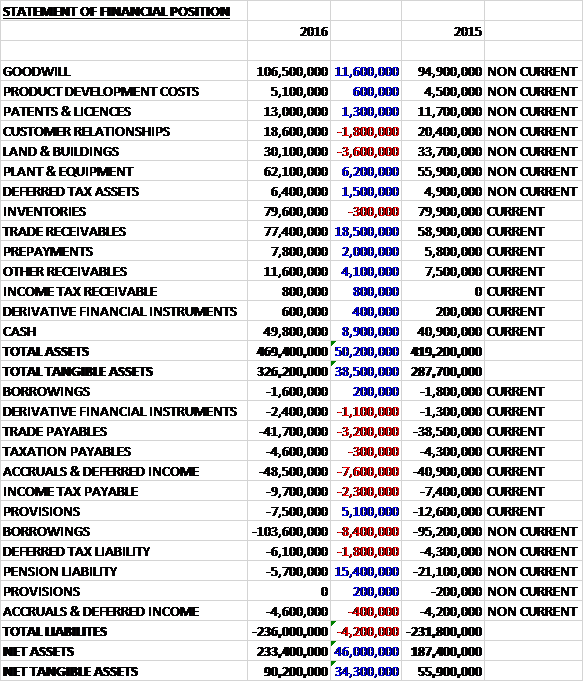

When compared to the end point of last year, total assets increased by £50.2M driven by an £11.6M growth in goodwill, an £18.5M increase in trade receivables, an £8.9M growth in cash, a £6.2M increase in plant & equipment and a £4.1M growth in other receivables. Total liabilities also increased during the year as a £15.4M decline in pension liabilities and a £5.1M decrease in provisions was more than offset by a £7.6M growth in accruals and deferred income, an £8.2M increase in borrowings and a £3.2M increase in trade payables. The end result was a net tangible asset level of £90.2M, a growth of £34.3M year on year.

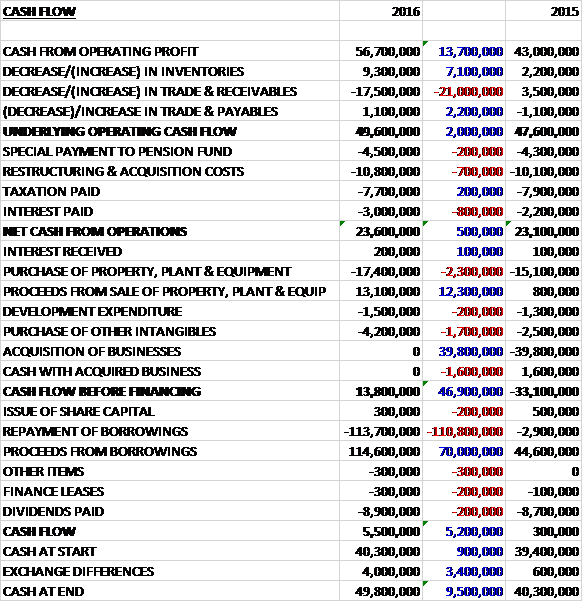

Before movements in working capital, cash profits increased by £13.7M to £56.7M. There was a cash outflow from working capital and after restructuring costs increased by £700K and interest payments grew by £800K, the net cash from operations came in at £23.6M, a growth of £500K year on year. The group spent £17.4M on property, plant and equipment but received £13.1M from the sale of fixed assets which included £12.3M from the sale of surplus sites in Weybridge, Fullerton and Werne. They also spent £1.5M on development expenditure and £4.2M on other intangibles to give a free cash flow of £13.8M. This was used to pay £8.9M of dividends so the cash flow for the year was £5.5M and the cash level at the year-end was £49.8M, boosted by £4M of positive forex movements.

Overall, underlying operating profit increased by £9.6M. Of this, £3.2M was due to favourable forex movements, £3.4M was the contribution from the acquired Aero Stanrew and £3M was from self-help actions and underlying business performance.

The underlying operating profit in the Transportation, Sensing and Control division was £3.2M, a positive swing of £4.6M year on year including a £600K forex benefit, with the division returning to profitable growth faster than expected. Revenues increased by 4% on an organic basis as a result of market demand in Europe and China together with new contract wins in China to service the growing domestic market. The business has maintained their strong position in Europe while driving growth in China and securing their first major win in the US where they see opportunity to grow market share over the medium term.

They have seen good growth in China with five new customers won during the year for position sensors in chassis applications in addition to further revenue growth with a number of existing customers. They have seen the ramp up of a new pedal platform and global crankshaft platform which has increased volumes sold in China. The European operations have also performed strongly with significant ramp up of new contracts during the year including for remote lights, LED lighting solutions and a chassis height sensor solution.

During the year they also launched a new automotive actuator to deliver significant improvements to their next generation haptic accelerator pedals offering power efficient transmission and a significant weight reduction from previous generation offerings, improving their customers’ fuel efficiency. New changes in emissions legislation have refocused industry efforts on turbo charged engines where the group has won a new contract for their high temperature sensors for a leading German OEM. They also have a wide range of products for exhaust after treatment including fluid quality sensors which they offer in Europe, India and Korea.

The underlying operating profit in the Industrial Sensing and Control division was £11.9M, an increase of £500K when compared to last year although it fell by 8% on a constant currency basis. Revenues also decreased with the fall in large part a result of challenging North American industrial markets, although the division returned to modest growth in the second half of the year. The optoelectronics offerings that combine the use of electronics and light have seen good growth through the year, improving the mix of business towards higher reliability and precision offerings which have a higher margin.

During the year the business launched a number of new products to support future growth including a component that transfers electrical signals between two isolated circuits using light, to support satellites, and spacecraft. We also launched a high-performance industrial pressure transmitter for a range of industrial applications including chemical plants, mining, power generation and plastics manufacturing.

During the year the business won a contract with an American computer hardware, software and electronics customer to design and deliver circuit board assemblies to be used in ATMs for detecting currency, cheques and deposit envelopes. They have a longstanding relationship with this customer for delivering individual IR emitting and detecting components as well as cable assemblies which are all core components in the new circuit board assembly contract.

The underlying operating profit in the Advanced Components business was £10.3M, a growth of £4.3M when compared to 2015 with £3.4M of that due to the Aero Stanrew acquisition, £200K from positive forex movements and £700K coming from organic improvements. The division released eleven new products during the year, further enhancing its position as global leader in circuit protection, detection and power management across aerospace and defence, transportation and industrial markets. The group continue to see strong demand for wire wound resistors targeted at the smart metering business, as a result of European legislation.

They are experiencing good growth in automotive electro-magnetics due increasing demand for high quality components for power management as their customers manage the increasing power requirement and increasing electronic content in cars. Their electromagnetic capabilities have been enhanced by the acquisition of Aero Stanrew and additional product launches including two power inductors and a transformer targeting demanding high temperatures in automotive and industrial applications.

This year they launched mag-Net, a new connector which forms part of a soldier system for the digital battlefield and enables communications for soldiers. It is currently being used in equipment trials with a large customer in the defence industry.

The underlying operating profit in the IMS business was £5.9M, a growth of £200K year on year but the constant currency profit declined by 11%. Revenues also decrease on a constant currency basis. Revenues in China were strong with new customers won in transportation and medical markets but the division was faced with challenging industrial markets in the US which resulted in a volume reduction as project revenues ended as expected.

In China good progress with operational efficiency measures supported a strong contribution to the divisional performance. The impact of the reduction in volume in the US was mitigated in large part through a 22% headcount reduction and other cost reduction actions. In the medical market they have seen strong growth in life sciences, ophthalmology and direct patient care, including winning a new contract with an Australian optometry equipment provider. The UK site in Rogerstone and the Chinese site in Suzhou collaborated on a cabin lighting project for a customer. In addition, the business has been supporting good growth in Advanced Components by providing specialist manufacturing capabilities for engine test equipment.

During the year they won a number of new customers in Asia in addition to expanding existing customer relationships. Sales in Asia increased by 17% at constant currency. In particular they have seen strong growth in the Chinese rail market where new business included a three year contract to provide design and manufacturing services for the Chinese metro lines. They have also started to win new customers across Asia Pacific as a result of focused sales efforts to meet growing regional demand which includes a Korean semiconductor customer won during the year.

Aero Stranrew was acquired in December 2015. In its full year of ownership, the business has been integrated, has performed well, achieved strong order growth and is on track to deliver return on invested capital in excess of the cost of capital this year. The group continue to look for new acquisition opportunities to accelerate growth due to organic top line growth being flat.

As usual there was a plethora of non-underlying costs. Restructuring costs related to further costs incurred on the operational improvement plan initiated last year, costs associated with other site restructuring and a credit of £4.3M arising on the sale of properties. Acquisition costs amounted to £3.8M which included a credit of £900K relating to the release of a provision established for warranty liabilities arising from a divestment that is no longer required, £3.5M amortisation of acquired intangibles and £1.2M of other costs, relating primarily to the integration of Aero Stanrew.

The triennial valuation of the UK pension scheme in 2016 showed a deficit of £46M compared with £19.1M and the group agreed additional fixed contributions extending to 2020. These amount to £4.7M, £4.9M, £5.1M and £3.9M. In addition they have set aside £3M over the last three years to be used in agreement with the trustees for reducing the long term liabilities of the scheme.

Going forward, despite uncertain end markets, the group enter the year with good momentum in operational efficiency improvement and a robust order book, giving them confidence of making further progress in 2017.

At the current share price the shares are trading on a PE ratio of 19.2 which falls to 14.5 on next year’s consensus forecast. At the year-end the group had a net debt position of £55.4M compared to £56.1M at the start of the year. After an increase in the final dividend the shares are yielding 2.8% which increases to 3% on next year’s forecast.

Overall then this has been a decent year for the group. Profits were up, net assets increased and the operating cash flow recovered, although the only reason free cash was generated was due to the property sales. Transportation sensing and advanced components both performed well with the former doing well in China and the latter benefiting from the Aero Stranrew acquisition. Industrial Sensing and IMS both struggled, however, due to a challenging North American industrial market. The pension scheme seems to be causing some problems too, and is looking rather expensive over the next few years.

There is no doubt that performance seems to be improving but the group has benefited from favourable exchange rates and last year’s acquisition. Organic growth seems much harder to come by and I feel that a forward PE of 14.5 and yield of 3% is a little expensive.

On the 12th May the group released a trading update covering the first four months of the year. Trading has been in line with expectations overall with revenues 10% higher than last year but just 1% up on an organic basis. The order book is strongly ahead of the prior year, giving them a better visibility in the outturn for 2017. During the period they acquired the assets of Cletronics, a small US-based manufacturer of electromagnetic components for the aerospace industry, for $1.2M.

On the 19th July the group announced that it had entered into a conditional agreement for the sale of its Transportation Sensing and Control division to AVX for a cash consideration of £118.8M, a value of about 11x the underlying EBIT. The proceeds will be used to pay down the existing debt and fund further investment to accelerate growth through capex and acquisitions. The pattern of trade across the remaining business has been good and the order book remains strongly ahead.

This disposal really repairs the balance sheet and leaves the shares looking decent value. It would be nice to get hold of an updated forecast but of course being a private investor I can’t do that! Shame.