The Property Franchise Group have now released their interim results for the year ending 2019.

Management service fees increased by £235K but franchise sales were down £132K and other revenue declined by £148K. Assisted acquisitions support increased by £29K but other cost of sales fell slightly to give a gross profit £59K lower. Depreciation increased by £29K but other admin expenses fell by £183K which meant the operating profit was £95K higher. Bank interest was slightly lower, as were tax charges so the profit for the period was £1.6M, a growth of £120K year on year.

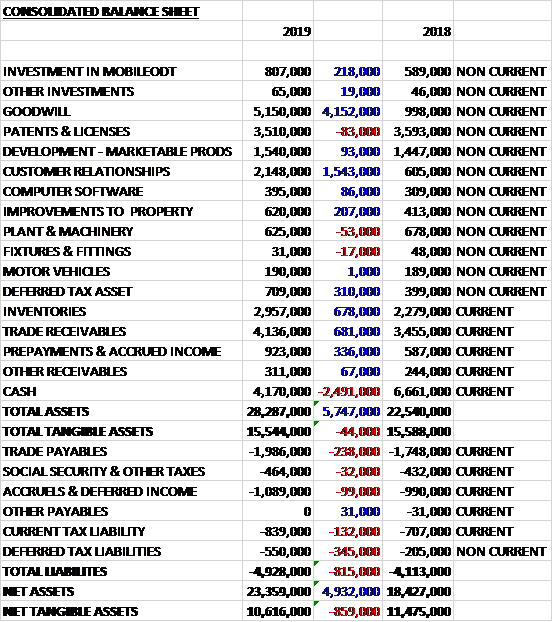

Total assets declined somewhat over the past six months, driven by a £207K decrease in the master franchise agreement, partially offset by a £124K growth in trade receivables. Total liabilities also declined during the period as a £228K increase in current tax payables and a £91K growth in other payables was more than offset by a £450K reduction in the bank loan. The end result was a net asset base (minus goodwill) of £8.6M, a growth of £84K over the past six months.

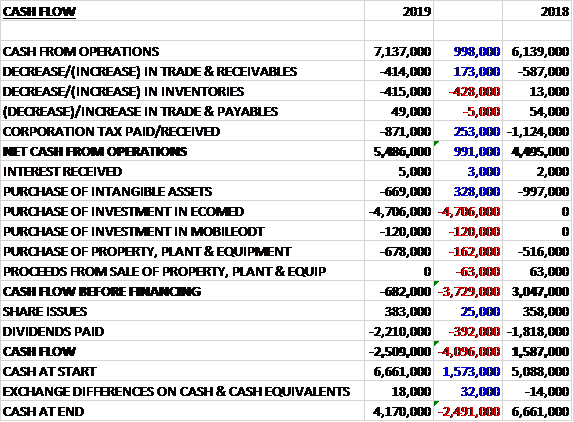

Before movements in working capital, cash profits increased by £122K to £2.4M. There was a small cash outflow from working capital but tax payments fell by £200K and interest payments were down £13K to give a net cash from operations of £2.2M, a growth of £209K year on year. The group spent £205K on assisted acquisitions support but there was negligible other capex so the free cash flow was £2.1M. Of this, £450K was used to repay loans and £1.5M was paid out in dividends to give a cash flow of £59K and a cash level of £3.9M at the period-end.

All six brands’ franchising networks experienced revenue growth over the period despite challenging market conditions. Their franchisees added 1,175 tenanted managed properties in the period through their assisted acquisitions programme which, alongside the continued organic growth of the portfolio, leaves the group managing 56,000 properties at the period-end.

For the traditional brands, growth was driven largely by a robust increase in lettings management service fees which outweighed the market weakness faced in sales. Ewemove has 115 franchise territories at the end of the period, which was broadly flat on last year but property listings have increased to 3,173 in the first half despite a falling market. The business has improved its cash generation and tight cost control has delivered a corresponding improvement in profitability. They are on track to materially improve on the 2018 result for the full year.

The government’s tenant fee ban took effect at the start of June with these results reflecting just one month’s impact of the ban. After the period end, July letting results exceeded board expectations with evidence of pent up demand feeding through.

Going forward, the group traditionally experiences stronger trading in the second half of the year and at this stage the board believe this pattern will be maintained. While the board are cognisant of the UK market conditions, they remain confident of delivering on market expectations for the full year.

At the current share price the shares are trading on a PE ratio of 16.7 which reduces to 14 on the full year consensus forecast. After an 8% increase in the interim dividend, the shares are yielding 4.2% which remains the same for the full year forecast. At the period-end the group had a net cash position of £2.8M compared to £500K at the same point of last year.

On the 20th November the group released a trading update. Trading during the second half of the year to date has remained strong and management are confident that the group remains in line to achieve market expectations for the full year. In October, they set a new record for lettings revenue at a franchise level who reported income of £6M. This was achieved despite the loss of tenant fee income following the ban in June, which had previously represented 16% of their franchisees lettings revenue.

Growth in management commission has increased 10% to £4.3M. The group believes that it is the high level of satisfaction of its landlord clients that lies behind the better than expected progress in shifting the burden of cost from tenants to landlords. Management are now confident that the objective of full mitigation of these costs will be attained by June 2020, six months earlier than originally thought.

The sales market has softened further in the second half of the year but the lettings business is outperforming expectations.

Overall then this has been a decent period for the group in a difficult market. Profits were up due to tighter controls over admin costs, net assets were flat and the operating cash flow improved with a good amount of free cash being generated. The lettings business is doing well, having mitigated the loss of tenant fees. Ewemove also seems to be making progress. The sales business is faring less well in this market, however. With a forward PE of 14 and yield of 4.2% this is not a bargain given the market conditions but it is a quality, cash generative company so I’m tempted to buy here at the right price.

On the 14th January the group announced that it intends to develop a new division, targeting the acquisition of financial services businesses which are relevant to the core business. The division will operate as a subsidiary and service the existing franchisees. It is the intention to make financial services available as a new franchise opportunity with the group holding the master franchise rights and delivering to its franchisees a mortgage products and compliance function.

As part of this strategy they have acquired a 72% stake in Auxilium Partnership a protection advisory business, for a non-material sum. The business was launched in March 2019, has no debt and is cash generative.

On the 28th January the group released a trading update covering the whole year ending 2019. Overall they performed in line with expectations, delivering growth in both revenues and management service fees. Their franchisees mitigated much of the impact of the tenant fee ban and achieved a record performance for lettings revenue. EweMove is also expected to show a significant improvement in profit over last year.

Despite the wider market being adversely impacted by the tenant fee ban, the group increased revenue by £200K and management service fees grew by £200K. They had net cash of £4M at the year-end.

As expected the tenant fee ban tempered lettings revenues in the second half but the group made good progress with a mitigation plan and is now confident that the objective of the full mitigation will be achieved by June 2020, six months ahead of the original plan. Early indications of improving market conditions underpin the board expectations that the volume of house sales should increase in 2020. The lettings market is also expected to remain healthy with rising rents and increased confidence leading to more opportunities for the franchisees to acquire competitors’ books than this year.

It is worth noting that the CEO is leaving having been with the group since IPO in 2013.