Avingtrans has now released their final results for the year ended 2019.

Revenues increased when compared to last year due to a £12.7M growth in Energy PSRE revenue, a £12.2M increase in Energy EPM revenue and a £1.7M growth in medical revenue. Depreciation was up £708K, cost of inventories grew by £29M but other cost of sales declined to give a gross profit £8.1M higher. Distribution expenses increased by £672K but acquisition costs fell by £1.5M, amortisation of acquired intangibles decreased by £1.7M and restructuring costs were down £1.3M. Other admin expenses increased by £4.3M to give an operating profit £7.5M improved. There was a decline in finance expenses, mainly due to no losses on derivative contracts but tax increased by £645K to give a profit for the year of £2.5M, an improvement of £9M year on year.

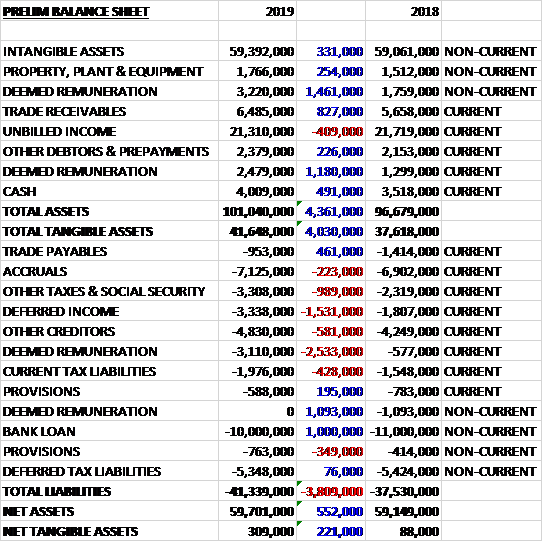

When compared to the end point of last year, total assets increased by just £533K driven by a £4.1M growth in inventories and a £2.3M increase in cash, partially offset by a £2.4M reduction in the amount due under long term contracts, a £1.3M fall in prepayments and accrued income and an £845K decline in customer relationships. Total liabilities also increased during the year as a £2.4M decline in borrowings and an £841K decrease in deferred tax liabilities was more than offset by a £5.6M increase in payments on account. The end result was a net tangible asset level of £31.4M, a growth of £1.4M year on year.

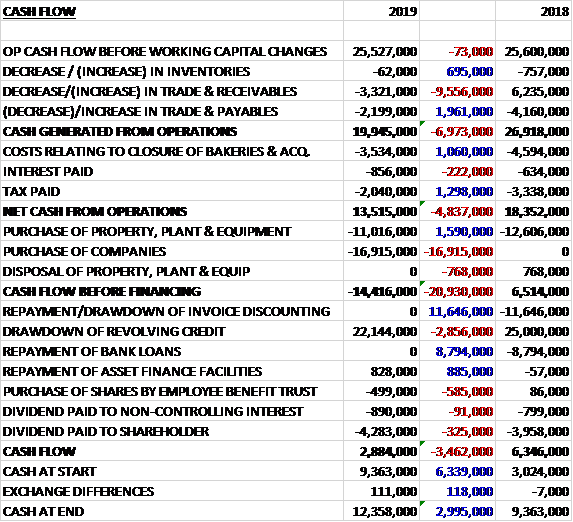

Before movements in working capital, cash profits increased by £5.6M to £7.4M. There was a cash inflow from working capital and despite increases in interest payments and tax the net cash from operations was £9M, an improvement of £15.9M year on year. The group spent £848K on intangible assets and £2.3M on fixed tangible assets to give a free cash flow of £6.1M. Of this, £3.3M was used to repay borrowings, £1.1M paid out in dividends and £1M went on finance lease payments to give a cash flow of £1.3M and a cash level of £8.1M at the year-end.

The operating profit in the Energy EPM division was £2.9M, an improvement of £4.4M year on year. During the year the division secured a number of key contracts, including to provide high temperature molten salt, nuclear life extension equipment and spare parts to nuclear reactors. As part of their global business strategy and to support growth, the group opened up a new factory in Kunshan, China, in January. They also opened a new motor rewind centre in India. The division has won a £10M order with Vattenfall in Sweden and further orders from KHNP in Korea and US nuclear operators.

In the UK and China, EPM signed an authorised channel and service partner agreement with Baker Hughes, a GE company which has a significant installed base in the UK, but no effective local facility to service, overhaul and upgrade their equipment. The business has gained its first order from a Gen IV nuclear developer in the US for molten salt technology and also funding from the US DOE to develop molten salt pump technology for advanced concentrated solar applications. With their new range of pumps for natural gas and a range of renewable technologies, they are slowly reducing their reliance on coal fired power stations.

The operating profit in the Energy PSRE division was £1.9M, a growth of £1.5M when compared to last year. The acquisition of Ormandy has integrated well and has made a satisfactory, albeit modest, profit. The business manufactures off-site plant, heat exchangers and other HVAC products. The fluid handling business in Scotland had an excellent year, as it expanded its capability to support the nuclear decommissioning market in the UK. This has further strengthened the division’s strategic relationship with Sellafield.

The division has a good interest in the UK nuclear submarine fleet and associated facilities as well as developing new nuclear technologies like small nuclear reactors. They have a good installed base on the UK submarine fleet, is the chosen manufacturing partner for the Astute steam turbines and through this experience can support longer tern nuclear technologies. As well as nuclear, divisional brands also have a strong presence in the oil and gas market. This market is now improving with the group securing an order for £10M for steam turbines for a floating production vessel.

The division has seen an increase in end user sales. In particular, PB saw further increases in aftermarket sales and won a new £5M UK government end user contract in June 2018. End-user service arrangements have been signed to gain better access to the reciprocating compressor installed base and an expansion of the channel partners and agents has been concluded. Overall the ration of aftermarket sales for the division has not improved in the year, but this is due to success in growing OE sales in parallel with the aftermarket.

Finally the Crown business remains a small but positive performer in the division, although the year was quieter than expected due to delays in the roll out of smart motorways and 5G networks.

The operating loss in the Medical division was £204K, an increase of £95K when compared to 2018. The division is making gradual progress at Scientific Magnetics and Tecmag as they look to integrate their various sub-systems to produce a prototype MRI demonstrator unit. They have now been able to take first images of inanimate objects with the system. They are now in the next phase of image refinement to bring the system up to the level expected in clinical diagnostic imaging. This next phase will take us a few months to complete and will continue to absorb some cash.

Within NMR, their service offering has been strengthened both in the UK and US so they are optimistic about seeing good progress over the next year. They continue to work with QOne in China and Switzerland on new NMR systems, to challenge the market leader. QOne have been successful in selling initial systems to the market over the last year, albeit that the numbers are still small.

Following its acquisition, Tecmag has been performing relatively well and with support from other group resources managed to achieve a break even result. There is a decent pipeline of legacy business to go for, pending their development of new products. Metalcraft UK’s business with Siemens for MRI components continues to be stable, although progress in China with other vacuum vessel customers remains rather pedestrian. Composite Products had a reasonable year with deliveries to Rapiscan continuing and support from other smaller accounts at this unit.

In October 2018 the group acquired Tecmag Inc for a total consideration of £132K, which generated no goodwill. The acquisition was made to enhance their position in the medical division and it generated profit of £13K. After the year-end the group acquired Booth Industries for a total consideration of £1.8M. In the first seven months of this year the business made a trading loss of £752K. They manufacture high integrity doors used in the nuclear, oil and gas and critical national infrastructure markets. Also after the year-end the group acquired Energy Steel & Supply for $600K which made a loss of $1.6M last year.

Going forward the board remain vigilant over Brexit but their direct EU exposure is somewhat limited and they have and they have taken actions over their supply chains. US and Chinese tariff risks have been largely mitigated by an agile supply chain response but they will continue to monitor that closely.

At the current share price the shares trade on a PE ratio of 32 which falls to 16.3 on next year’s consensus forecast. At the year-end the group had a net debt position of £2M compared to £7.1M at the end of last year. After an increase in the final dividend the shares are yielding 1.5% which increases to 1.6% on next year’s consensus forecast.

On the 30th October the group announced that Booth Industries secured a £7.2M government contract for safety doors. When the group acquired Booth, it did not acquire the existing order book and this new contract brings the total value of contracts won to £12M, spread over the next two years.

Overall then this has been a good year of progress for the group. Profits are up, net assets increased and the operating cash flow improved with plenty of free cash being generated, albeit with help from working capital movements. The energy division seems to be performing well and I would say has hit critical mass but the same can’t really be said of the medical division. It is still loss making and seems to lack the immediate potential to make meaningful profits. I am tempted to buy into the story here, it is still quite expensive with a forward PE of 16.3 and yield of 1.6%, however.

On the 8th November the group announced that director Austen Adams sold 29,008 shares at a value of £72K. He now owns just 5,000 shares.

On the 23rd January the group released a trading update covering the first half of the year. They continued to perform well and are trading in line with market expectations. The order and prospect pipeline remains robust with notable orders secured including a £2M order for HT China for pumps to be installed at a new concentrated solar power plant in Dubai; a record £1M order for Fluid Handling in Scotland from Sellafield for remote maintenance valves to be used on nuclear waste reprocessing equipment; and a £2M order for Peter Brotherhood for additional steam turbines in the defence market as part of a long standing framework agreement.

The recent acquisitions are responding to their recovery programmes well and are integrating as expected with strong order books already secured and healthy prospect pipelines.