Solid State has now released their final results for the year ended 2019.

Revenues increased when compared to last year as a £1M decline in communications products revenue and an £833K decrease in power products revenue was more than offset by a £10.7M growth in electronic components and modules revenue and a £1.2M increase in computing products revenue. There was a £315K beneficial swing to a forex income but depreciation was up £209K, amortisation increased by £545K and other cost of sales grew by £5.8M to give a gross profit £3.6M higher. Admin expenses also increased ogive an operating profit £406K higher. An increase in interest was offset by a reduction in tax charges so the profit for the year came in at £2.7M, a growth of £415K year on year.

When compared to the end point of last year, total assets increased by £12.3M driven by a £3.1M growth in cash, a £2.8M increase in inventories, a £2.4M growth in trade receivables, a £1.8M growth in goodwill and a £1.1M increase in other intangible assets. Total liabilities also increased during the period due to a £5.7M growth in borrowings, a £1.5M increase in trade payables, a £1.3M increase in accruals and a £1.2M growth in contract liabilities. The end result was a net tangible asset level of £11M, a decline of £842K year on year.

Before movements in working capital, cash profits increased

by £1.1M to £4.6M. There was a cash

inflow from working capital and after interest payments increased by £76K and

tax payments were up £276K there was a net cash from operations of £4.6M, a

growth of £3.2M year on year. The group

spent £600K on property, plant and equipment, £300K on intangible assets and

£3.8M on an acquisition, although they recouped £113K from the sale of assets

to give a cash outflow of £34K before financing. They took out a net £4.2M of new borrowings

and paid out £1M in dividends which gave a cash flow for the year of £3.1M and

a cash level of £3.7M at the year-end.

The pre-tax profit in the Distribution division was £1.7M, a

growth of £382K when compared to last year with an organic sales growth of around

25%, gaining market share, although there was some benefit from Brexit stocking

in Q4 along with a one-off order for around £1M. The addition of the VPT franchise to the

product portfolio in Q1 had a major impact with sales well ahead of budget. This product line represents a continuing

opportunity for the division with the leading edge indicator of design-in

activity showing high levels of activity.

Following the acquisition of Microsemi by Microchip, the

distribution franchise with Microsemi has been extended to include all

Microchip products after the year-end.

This provides significant new product lines and opens up an opportunity

to sell the extended offering to their customers. Additionally the Pacer acquisition adds yet

more expertise and marketing activity increased towards the end of the year to

promote the broader product offering of the enlarged division. The management of the division remain

optimistic about prospects in 2020 and expect it to be another strong

year.

The pre-tax profit in the Manufacturing division was £2.7M,

an increase of £332K year on year despite a marginal fall in revenues

reflecting a favourable change in mix with a greater proportion of high value

added projects. Within the division they

have established three business units – Computing, Power and

Communications.

The Computing business has seen a continued increase in

demand for AI and Internet of Things solutions that are image and video

centric. They have secured an important

order for a new security accredited product for a UK government client that

will deliver revenue in 2020 with additional associated prospects. During the year they introduced a new series

of own brand 19” rack mount servers including entry level and high end chassis

solutions with respective features and pricing competitively matched. In addition they have resolved and delivered some

long standing technically challenging military projects that they were committed

to deliver against the customers’ requirements, maintaining a strong

relationship that will bode well for future co-operation.

In the Power business, they have made some initial sales

into the retail technology and medical sectors where they have not been

traditionally strong, to complement the oil and gas and aerospace sectors. Battery cell manufacturers continue to limit

the supply of product to third part providers and are extending lead times

across the industry in order that they can service the needs of the electric

vehicle market. The focus for future growth remains on harsh environment applications

where they can add value. New

applications in robotics solutions are being targeted in varied market sectors.

In the communications business, the level of business has

fallen over the prior year but they have made significant progress in

developing a portfolio of more standard off the shelf antenna products which

are underpinning more sustainable revenues to augment the bespoke programmes

which the business has traditionally undertaken. This includes provision of antennas for test

and measurement applications within the burgeoning 5G market.

The radio team has established business relationships with

complementary companies providing mission planning computers, digital mapping

solutions and optical sensors, positioning the business as a subsystem provider

of both the data links and situational awareness product. This will allow them to move up the value

chain, generating larger contracts. This

year they have made progress in the early stages of developing the pipeline of international

opportunities for an integrated communications solution.

The group continued to make investments in inventory, in

particular battery cells and processors, to exploit opportunities and mitigate

the risks associated with extended lead times, Brexit and the US/China trade

dispute. The closing stock position also

reflects the Pacer acquisition.

In November he group acquired Pacer Technologies for a cash

consideration of £3.8M. The business was

established in 1989 to specialise in the distribution and custom design of

optoelectonic components, lasers and displays to the OEM market in the medical,

military, commercial, industrial and security sectors. Products include industrial LEDs, lasers,

photon detection and counting equipment.

The business has offices in the UK and the US. During the year Pacer invested in a new value

added facility in Weymouth which includes a clean room.

Going forward, the group’s open order book was up 56% on the

prior year. The acquisition of Pacer has

been a large contributor to this but like for like the order book was still up

20% which gives the board confidence that they remain on track to deliver in

line with expectations. The

macroeconomic environment from the US China trade war to the ongoing Brexit

uncertainty present a level of risk, however.

Current year trading has been ahead of the same period last

year but order intake during Q1 has been softer than expected, likely as a result

of the unwind of Brexit stocking. The open order book remains solid,

however.

At the current share price the shares are trading on a PE

ratio of 15 which falls to 12.6 on next year’s consensus forecast. After a 4% increase in the dividend, the

shares are yielding 2.7% which increases to 2.8% on next year’s forecast. At the year-end the group had a net debt of

£2M compared to a net cash position of £600K at the end of last year.

Overall then this has been a decent year for the group. Profits were up, although net tangible assets declined. The operating cash flow improved but no free cash was generated after the acquisition. The distribution division did well partly due to stock build before Brexit and a large one-off order, although the underlying performance looks good too. The manufacturing division improved due to a focus on higher margin products. Going forward, there are plenty of macroeconomic risks and indeed Q1 orders have been soft, although this is thought to be temporary. The forward PE of 12.6 and yield of 2.8% look about right and I continue to hold.

On the 3rd September the group released a trading

update where they stated that as a result of a strong start to the year the

board is confident that profits for the year will be significantly ahead of

expectations. Revenue is expected to be

in line with forecasts.

Trading in the first four months has been very strong. Generally revenues have been in line with

budget but there has been an acceleration of certain project work into the

first half that had been expected in the second half.

Gross margins are stronger than expected as a result of a favourable sales mix in the manufacturing division and continuing production efficiencies, Pacer continues to perform ahead of expectations and also the group is expecting to benefit from forex movements in the first half.

On the 24th October the group released a trading

update covering the first half of the year.

The record trading performance achieved last year has continued in the

first half of this year and the group is on track to deliver full year earnings

in line with board expectations. Group

sales are expected to show organic growth of 7.5% despite the heightened macroeconomic

uncertainties of recent months.

Gross margins have benefited from £300K of forex tailwinds

with underlying group margins having seen a slight improvement over the prior

period and the pre-tax profit is expected to be around £2.5M. The open order book stood at £36.5M at the

end of the period compared to £36.2M at the same point of last year.

Amino Technologies have now released their interim results for the year ending 2019.

Revenues declined when compared to the first half of last year as a $557K growth in ROW revenue was more than offset by a $3.1M decline in North American revenue, a $2.2M decrease in European revenue and a $1.8M fall in Latin American revenue. Cost of sales also decreased to give a gross profit $1.4M lower. Operating expenses fell by $3.5M, amortisation was down $730K but there was a $305K escrow release paid to employees and redundancy costs grew by $351K to give an operating profit $2.6M higher. After tax charges were up $433K the profit for the period came in at $2.4M, a growth of $2.2M year on year.

When compared to the end point of last year, total assets decreased by $11.8M, driven by an $8.1M fall in receivables, a $1.8M decline in intangible assets and a $984K decrease in cash. Total liabilities also decreased during the period due to a $9.3M fall in payables. The end result was a net tangible asset level of $18M, a decline of $761K over the past six months.

Before movements in working capital, cash profits increased

by $1.9M to $7.2M. There was a cash outflow from working capital and after a

small increase in tax payments then net cash from operations was $6.2M, a

growth of $1M year on year. The group

spent $1.8M on intangible assets to give a free cash flow of $4.4M which did

not cover the dividends so the cash flow for the half year was an outflow of

$974K and the cash level at the period-end was $19.3M.

The performance in the North American market has been on

target which was a good result given the US tariffs delaying and disrupting

purchase decisions. Contract wins in the

region included Waverly Utilities who selected their Multimedia over Coax capabilities. It delivers IP over existing coaxial cable

deployed to the home. They also saw good

momentum in existing customers migrating to their next generation devices.

Latin America continues to be an important market. They have made good progress with follow on

orders from key customers and also secured a significant new contract with

Entel, the national telecoms operator in Bolivia, supporting a major

country-wide fibre roll out.

In Europe the group has seen significant growth in active

subscribers across its customer base with a 22% increase in the period. They have also rolled out AminoTV across

Delta and Caiway on a multi-tenanted platform and therefore expect this growth

to continue into the second half. The

territory has also been strengthened by the creation of a new distribution

agreement with Scansource to cover all EMEA.

During the period they officially certified the next generation of these

devices with Google on their Operator Tier Android TV platform.

Software and service revenues decreased by 22% in the first

half, primarily as a result of lower AminoTV professional services for their

largest customer as part of the natural cycle to a shift to project maintenance

after implementation. Device revenue

declined as expected as a result of the focus on higher margin accounts.

The group exceeded their $5M annualised cost saving target

through the transformation programme.

They are starting to see pricing and supply constraint pressures on key

components easing, which remain dependent on external market forces.

In May the US added Huawei to the BIS entity list. Subject to the outcome of recent discussions

between the US and China, this may mean that certain US companies are unable to

trade with Huawei. Whilst the outcome of

these talks is not yet clear, there is a risk that this may disrupt discrete

elements of their supply chain for a small number of products. The board do not believe that this will have

a material impact on their performance but they have taken mitigating steps by

dual-sourcing key components.

Going forward, ongoing progress with their transformation

strategy allied to their strong order book, backlog and sales pipeline coverage

underpins the board’s confidence in guidance for the full year despite the

expectation that the challenging market conditions will continue into the second

half.

At the current share price the shares are trading on a PE

ratio of 14.2 which falls to 12.3 on the full year forecast. At the period-end the group had a net cash

position of $19.3M compared to $15M at the same point of last year. After the dividend was kept the same the

shares are yielding 5.8% which is forecast to remain the same for the full year.

On the 15th July the group announced the

acquisition of 24i Media, an online video specialist providing Apps as well as

user experience, solutions and services for a total consideration of €21.4M.

The acquisition will enable the group to deliver full end to

end and on-demand personalised content to its customer base and will build

momentum in their software and services revenues, as well as recurring

revenues. The business has an HQ in

Amsterdam and has a presence in the Czech Rep, Brazil, the US and Spain. It had revenues of €7.1M last year and a

pre-tax loss of €100K. Double digit

revenue growth is expected to continue.

The business has net assets of €3.6M so the acquisition generates

goodwill of €17.8M.

The initial consideration of €19.3M comprised €16M in cash

and €3.3M in Amino shares comprising 3.2M shares to the founders. The deferred consideration of €2.1M comprises

€1.1M in cash payable on the first anniversary of the transaction subject to

the founders remaining managing the group and €1.1M in cash payable on the

second anniversary subject to the founders remaining.

The acquisition is expected to be earnings accretive in the

first full year of ownership.

Overall then this has been a fairly decent period for the group. Profits increased due to lower expenses and the operating cash flow improved. Some free cash was generated but not enough to cover the dividends, however, and net assets did decline. There are a number of issues affecting the market at the moment such as US tariffs and the issues with Huawei but despite these all markets seem to be performing fine. The forward PE of 12.3 and yield of 5.8% doesn’t look too taxing and I am thinking of buying in, although the acquisition does add some risk.

On the 9th December the group released a trading

update for the year. They expect to

report a performance in line with expectations.

They have a net cash position of $1.4M.

The integration of 24i with the group acquired in July is complete and

it continues to make good progress. They

have announced their first joint contract, an agreement with Dutch mobile

virtual network operator Youfone to provide a fully integrated end to end video

solution to refresh and expand its TV and OTT offering. Youfone will deploy a solution that combines

the group’s IPTV and TV Everywhere expertise with 24i’s video experience

design.

Trifast have now released their final results for the year ended 2019.

Revenues increased when compared to last year with growth across all regions. Depreciation was up £316K and other cost of sales increased by £8.6M to give a gross profit £2.4M higher. Distribution expenses were up £200K, operating lease expenses increased by £749K, share based payments were up £260K and other underlying admin expenses grew by £425K, offsetting this was a £512K improvement to a forex gain. We also see a £2.7M increase in Project Atlas costs and the non-repeat of a £556K profit from the sale of fixed assets, all of which meant that the operating profit was £1.9M lower. Interest costs increased by £215K and tax charges grew by £760K due to a prior year tax adjustment relating to EU loss relief claims, to give a profit for the year of £12.2M, a decline of £2.8M year on year.

When compared to the end point of last year, total assets increased by £15.9M, driven by an £8.4M increase in inventories, a £3.2M growth in other intangible assets, a £2.2M increase in goodwill and a £1.2M growth in trade receivables. Total liabilities also increased as a £2.4M decline in other payables and accrued expenses was more than offset by a £5.7M growth in loans and borrowings. The end result was a net tangible asset level of £77.2M, a growth of £5.3M year on year.

Before movements in working capital, cash profits declined

by £278K to £23.2M. There was a cash

outflow from working capital, and interest payments increased by £218K,

although tax payments were down £972K to give a net cash from operations of

£9.1M, a decline of £427K year on year.

The group spent £4.2M on capex and £8.2M on acquisitions which meant

there was a cash outflow of £3.1M before financing. The group took out a net £6.2M to pay £4.6M

dividends and the cash outflow for the year was £1.2M to give a cash level of

£25.2M at the year-end.

The profit in the UK division was £8.6M, a growth of £257K

year on year with revenue growth of 8.4% reflecting the acquisition of PTS in

April 2018. The business has integrated

well, achieving double digit growth.

Organically they have seen a slight reduction in overall trading levels

due to the downturn in UK automotive manufacturing volumes. Gross margins in the organic business reduced

by 150 basis points as a result of deferred purchase price inflationary

pressures coming out of the extended weakness in Sterling.

The profit in the European division was £8.4M, a decline of

£652K when compared to last year despite revenues increasing by nearly 5%. A key driver for the revenue growth was the

double digit increases across six of their operations including automotive in

Holland, electronics in Hungary and general industrial in Germany. Reduced domestic appliances volumes as the

result of trading conditions in their Italian operations have offset some of

these increases. Whilst the Spanish

greenfield site continues to grow, securing its first £1M of annual sales in

the year.

The decline in profit is put down to overhead investments to

support growth in Holland, Sweden, Hungary and Spain. In Italy, investments to build their

manufacturing capacity ahead of volume increases have continued to restrict

short term margins there which is expected to reverse over the longer term.

The profit in the US division was £427K, an increase of

£375K when compared to 2018 with revenue growth of 38% following a site move at

the start of the year. This reflects

ongoing gains in both the automotive and electronics sector as their US

business makes good use of the group’s existing customer relationships.

The profit in the Asian division was £9.5M, a growth of £1M

year on year with revenue growth of 3.6%.

There was strong domestic appliance sector increases in Singapore being

offset to some extent by the local factory closure of one of their

multinational OEM customers in China, as well as the knock on effect of

additional US tariffs to a small number of their multinational customers

operating in the region.

The largest source of organic growth (organic revenue growth

was 2.2%) continued to be from the multinational tier 1’s in the automotive

sector, with strong global automotive sales of 6.4%. Excluding the impact of the reductions of

volumes in the struggling UK automotive market this growth would have been 8.7%

as they continue to win market share via new platform builds despite the

reduction in global manufacturing volumes.

There was a £2.5M increase in inventories as a result of

Brexit planning. Outside of Brexit,

additional stock investments of £1.9M have been made at their US operations to

support their strong ongoing growth and to ensure buffer stocks are held as new

platform wins go into production. Going

forward, they expect the negative impact of this to settle.

On the manufacturing side the capex plans will continue,

albeit at a reduced level to increase capacity, most noticeably at the Taiwan

site. This will reduce the per part

production costs by bringing more manufacturing in house. On the distribution side they will be

extending their warehouse facilities in Lancaster in 2020, supporting the

double digit growth they have seen there over the last three years. Looking longer term, the board has approved a

more substantial site move in Hungary for the summer of 2020. This relocation to a purpose built warehouse

will more than double capacity to future proof the business for further

growth. In Europe they will continue to

invest in their expanding distribution site in Spain.

In April the group acquired PTS for an initial consideration

of £8.5M and contingent consideration of up to £2.5M in cash. Based in the UK, the business is a

distributor of stainless steel industrial fastenings and precision turned

parts, primarily to the electronics, medical instruments, petrochemical,

defence and robotics sectors. Over the

last year the business contributed £1.2M to group pre-tax profit.

There were a number of one-off items during the year. Net acquisition costs of £100K were incurred

in relation to the acquisition of PTS but this was offset by a £100K fall in

the contingent consideration. As a

consequence of the work undertaken on Project Atlas, the group have incurred

direct costs of £3.1M largely relating to project team and consultancy costs. A factory, previously rented to an automotive

OEM was sold in the prior year for £1.7M which generated a one-off profit of

£600K.

Despite the global reduction in vehicle volume production

through the latter part of 2018 and start of 2019, the group has made

significant market share gains so that so far they have not been too badly

affected despite earning around a third of their revenues from Tier 1 and 2

automotive suppliers with a 6% organic revenue growth.

Going forward there can be no doubt that the macroeconomic

environment has become more challenging over recent years. With the uncertainty of Brexit weighing on

the UK economy, the continuing trade tensions between the US and China and the

heightened risk of a Eurozone recession.

Despite this the group have entered the year well positioned with a

solid pipeline in place and their expectations for the year ahead remain

unchanged.

After a 10% increase in the dividends, the shares are

yielding 1.9% which increases to 2% on next year’s forecast. At the current share price the shares are

trading on a PE ratio of 22.7 which falls to 14.7 on next year’s forecast. At the year-end the group had a net debt

position of £14.2M compared to £7.4M at the end of last year.

Overall then this was a fairly decent update in a difficult market. Profits declined due to the costs associated with Project Atlas, net assets grew but the operating cash flow declined somewhat with no free cash being generated after the acquisition. Most regions saw profit growth, although in the case of the UK it was due to the acquisition. Profits declined in Europe due to an increased investment in overheads. Going forward, there are growing macroeconomic risks including Brexit, increased barriers to trade and a faltering automotive market in some areas. The shares are not exactly cheap either with a forward yield of 2% and PE of 14.7. This remains a quality company though so I am minded to hold on for the moment.

On the 24th July the group released a trading update. The macroeconomic environment has become more volatile over the last twelve months and the uncertainty has manifested in lead times on production schedules moving out on a number of new business wins. This has impacted the start of 2020, also marked by some instances of subdued demand in certain geographies as well as the ongoing automotive slowdown. The pipeline remains solid, however, and activity levels around the group continue to be encouraging. At this early stage, however, the board’s expectations for the year remain unchanged.

On the 21st October the group released a trading

update for the first half of the year. The

challenging market environment has continued into Q2 with end markets across a

number of sectors remaining weak, particularly in automotive. This has led to some reduced volumes to

existing builds across the UK, Europe and Asia.

As well as lead times on production schedules moving out on a number of

new business wins.

The impact of this has reduced revenue levels with a

corresponding reduction in gross and operating margins against a semi-fixed cost

base. As a result, following a review of

their year to date results and an update in forecasts for board have concluded

that in the absence of further market deterioration, their underlying pre-tax

profit in 2020 is expected to be around £22M.

The pipeline of new wins remains solid and activity levels

around the group continue to be encouraging across all sectors. Both their US region and the latest UK

acquisition, PTS, have continued to perform well, delivering double digit

revenue growth.

Somero have now released their final results for the year ended 2018.

Revenues increased when compared to last year as a $2.4M reduction in Canadian revenue was more than offset by a $9.2M growth in US revenue and a $1.6M increase in ROW revenue. Depreciation was down $925K but other cost of sales increased by $4.4M to give a gross profit $4.9M higher. Selling expenses were up $633K, engineering expenses increased by $135K and admin expenses grew by $354K which meant the operating profit was $3.7M higher. There was a $519K detrimental swing to a forex loss but other expenses reduced by $163K before a $209K increase in tax charges meant that the profit for the year came in at $21.5M, a growth of $3.1M year on year.

When compared to the end point of last year, total assets increased by $8.7M, driven by a $9.2M growth in cash and a $2.1M increase in inventories partially offset by a $1M decrease in prepaid expenses and other assets, a $795K fall in accounts receivable and a $746K decline in deferred tax assets. Total liabilities also increased as a $1M fall in accounts payable was more than offset by a $1.3M increase in income tax payable. The end result was a net tangible asset level of $52.2M, a growth of $8.2M year on year.

Before movements in working capital, cash profits increased

by $2.5M to $25.3M. There was a cash

outflow from working capital but this was less than last year and after the tax

income increased by $705K the cash from operations came in at $23.8M, a growth

of $3.8M year on year. The group spent a

net $756K on capex to give a free cash flow of $23.1M. Of this, $12.3M was paid out in dividends and

the cash flow from the year came in at $10.1M to give a level of $28.2M at the

end of the year.

Sales in North America grew 12%. That was driven by strong H2 trading in which

sales grew 16%. The high level of

non-residential construction activity alongside a shortage of skilled labour

increased the demand for the group’s products.

They see continued strength in the underlying non-residential

construction industry in the US and an extended pipeline of projects that

remain in front of their US-based customer base. Going into next year, market drivers in North

America continue to demand for replacement equipment, technology upgrades,

fleet additions and new products.

In Europe, 2018 sales grew by $300K driven by a solid

performance throughout the year. The

most significant markets were the UK, Germany, France, Spain and Portugal. European market conditions and activity

levels remain positive with well-balanced demand.

In China sales declined by $200K. The board believe they are taking the

appropriate steps to position themselves for future growth in the region. This includes a narrowed product line focus

supported by marketing and demand generation initiatives, combined with the

expected increasing benefit from the in-country sales leadership. They will continue to pursue market

development efforts to drive he acceptance and demand for quality concrete

floors by building owners and end users.

Sales in the Middle East increased by $300K. Activity levels were solid throughout the

year with meaningful contributions from Turkey, UAE and Egypt. In Latin America sales were down $600K as

project activity remained solid but did not translate into equipment sales as

expected due in part to the impact of election cycles in the region. During the year, the most significant

contributors came from Mexico and Chile.

They remain encouraged by the activity seen throughout the year,

particularly in Mexico and see improvement in 2019.

In the ROW region sales were strong, up $1.7M. The most significant contributors to growth

were Australia and India. They are

particularly encouraged by early signs of increasing demand for concrete floors

in India and the investments they have made with in-country leadership and

resources are helping to drive these results.

During the year the group completed the design and

development of the SkyScreed 25, the world’s first Laser Screed machine for use

in structural high rise applications.

This opens up a new market segment.

The board are pleased with early interest in the product but also

understand this only represents the first step in a long journey of product

development. They have therefore made

the decision to moderately increase investment to enable them to accelerate

product development initiatives in this market.

They are confident in their ability to deliver on these initiatives

alongside continuing to deliver profitable growth for shareholders.

The group is also moving forward with plans for a $3.5M

expansion of their Michigan facility.

This will add 35,000 square feet to the facility, providing their

assembly operations with needed space to accommodate their broadening product

line. In addition the expansion will add

needed office space and engineering testing areas. They will not, however, be proceeding with

the planned $1.3M expansion of the Florida facility in light of this. They now will review options to modestly

expand training and office space in Florida at a significantly lower cost.

After the year-end, in January, the group purchased the

business assets of Line Dragon, a US-based provider of concrete placing and

hose dragging equipment to the concrete industry. The acquisition was for $2M in cash with

ongoing performance payments.

Going forward, the board believes the group has numerous

meaningful growth opportunities next year that is supported by positive

non-residential construction market conditions and reinforced by customers reporting

project backlogs that extend beyond 2019.

Based on this, they are confident that they will deliver another year of

profitable growth.

At the current share price the shares are trading on a PE

ratio of 9.8 which increases to 10.9 on next year’s forecast. After a 23% increase in the dividends, and

including a supplemental dividend, the shares are yielding 6.8% but this falls

to 5.2% on next year’s forecast. At the

year-end the group had a net cash position of $28.2M compared to $19M at the

end of the prior year.

On the 7th June the group released a trading

update covering the first five months of the year. Trading in the period has fallen below

management expectations, primarily due to adverse weather conditions in the US

where broad sections experienced the highest levels of rainfall on record. This has delayed project starts which has

slowed the pace of equipment purchases, the impact of which was seen in March

and April. Whilst there was an

improvement in trading towards the end of May and they expect trading in the US

will improve through the rest of the year, they now do not expect to fully

recapture the shortfall in the current year.

As such they now expect to deliver revenues of $87M, EBITDA

of around $28M and expect to have year-end net cash of $18M. The positive US market conditions have not

changed and whilst they expect it will take some time for momentum to rebuild,

the level of work in front of their customers remains significant.

In the group’s other main markets, Europe and China, as well

as in the ROW territories, trading has been comparable to 2018 and they

continue to see opportunities for growth in the second half. Growth in India

has been steady. The Middle East and

Latin America are trading below 2018 levels, but they expect to see

improvements in the second half notwithstanding the political uncertainty and

economic challenges in these regions.

Overall then 2018 has been a good year for the group. Profits were up, net assets increased and the operating cash flow improved with plenty of free cash generated. Unfortunately this performance has not transferred into 2019. The main problem is being blamed on the weather in the US, by far the most important market. Elsewhere Europe, China and ROW seem solid if not great but the Middle East and Latin America is not doing well. With an improvement in the weather in the US, sales have improved but not enough to offset the shortfall. It does appear that global markets in general are more subdued but as long as the US market remains robust, this should be temporary. With a forward PE of 10.9 and yield of 5.2% this still seems decent value.

Avon Rubber have now released their interim results for the year ending 2019.

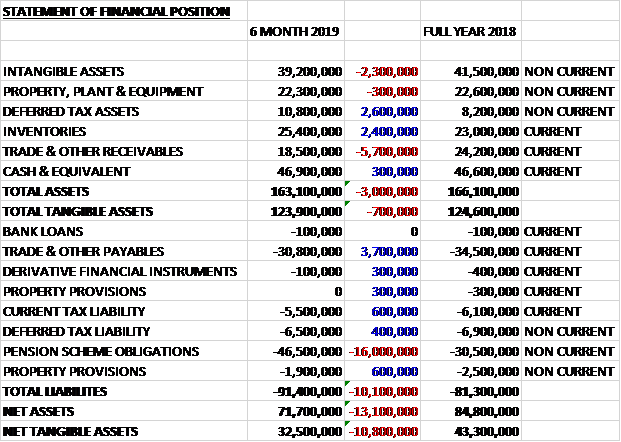

Revenues declined when compared to the first half of last year due to a £3.8M fall in protection and defence revenue and a £300K decrease in dairy revenue. Cost of sales also fell to give a gross profit £2M lower. Depreciation was down £400K but other selling and distribution costs were up £900K. Amortisation increased by £900K and there was a £2.9M charge relating to the GMP equalisation. This meant that the operating profit declined by £6.1M. Finance costs were slightly lower and tax charges fell by £300K to give a profit for the period of £2.8M, a decline of £5.7M year on year.

When compared to the end point of last year, total assets declined by £3M, driven by a £5.7M fall in receivables and a £2.3M decline in intangible assets partially offset by a £2.6M growth in deferred tax assets and a £2.4M increase in inventories. Total liabilities increased during the period as a £3.7M decrease in payables was more than offset by a £16M increase in pension obligations. The end result was a net tangible asset level of £32.5M, a decline of £10.8M over the past six months.

Before movements in working capital, cash profits declined

by £3.4M to £12.7M there was a cash outflow from working capital which was

higher than last time but both tax and interest charges reduced slightly to

give a net cash from operations of £8.9M, a decline of £7.3M year on year. The group spent £2.3M on fixed assets and

£1.8M on purchased software so the free cash flow came to £4.8M. Of this, £3.3M was spent on dividends and

£1.3M on their own shares to give a cash flow of £200K and a cash level of

£46.9M at the period-end.

The operating profit in the Avon Protection division was

£6.1M, a decline of £2.6M year on year.

Military revenues rose but both law enforcement and fire revenues

declined. The group were awarded two

significant long term contracts with the US DOD. The M53A1 framework contract, which also

covers additional products has a maximum value of $246M and a minimum five year

duration. This framework is accessible

to a number of different customers within the DOD including all four military

service branches. The first order under

the contract worth $20.2M was received in March with deliveries starting in the

second half of the year.

The M69 sole source contract to supply the DOD with the M69

Joint Service Aircrew Mask for Strategic Aircraft, related accessories and

engineering support extends their portfolio reach into the aviation sector for

the first time and has a maximum value of $93M and a minimum five year

duration. The first orders, worth

$17.8M, were received in February with deliveries also starting in the second

half.

These contract awards support their portfolio as it

transitions from being historically focused on the M50 mask system to becoming

a multi-product portfolio. Having grown

orders ahead of revenue, these contracts together with a broadening ROW

military and law enforcement customer base provide the group with greater flexibility

to manage order fulfilment scheduling.

The extended US government partial shutdown has impacted

profit in the period from their ROW military and law enforcement

customers. The admin backlog created

continues to reduce and with a strong opening order book, the recently

announced mask system contract and a pipeline of other opportunities they have

good visibility for the second half of the year.

The military order book of £44.2M has grown significantly in

the period driven by the first orders for the M69 aircrew mask and the M53A1

mask and powered air system contracts.

Military revenues of £30.9M were 7.2% higher. DOD revenues of £22.9M were lower than last

year with lower shipments of M50 mask systems and a different phasing of

filters, spares and accessories. This

was offset by a £6M increase in revenue from ROW customers reflecting

completion of the Norwegian military MCM100 underwater rebreather order.

Law enforcement revenue reduced by 38%. This was significantly impacted by the

extended US government partial shutdown.

Delays in the timing and shipment of orders resulted in a carryover of

revenue into the second half with an opening order book of £8.3M compared to

£3.6M at the end of last year. They

expect a much stronger second half for law enforcement as a result, the impact

of delays in H1 mean that they do not expect to show year on year growth for

the business, however.

Fire orders received reduced by 2.3% to £8M. The timing of shipments resulted in revenue

decreasing by 11.4% which is offset by the growth in the order book of £1.3M,

supporting expectations of a return to growth in the second half. Delays in the NFPA approval process mean they

are now expecting to be able to launch their upgraded Magnum SCBA in Q4.

The operating profit in the Dairy division was £1.9M, a

decrease of £700K when compared to the first half of last year. After a weaker environment through Q1 in the

key North American and European markets impacted all business lines, Q2 has

seen a rebound in dairy market conditions, with improving milk prices reflected

in increased farmer confidence which has resulted in improved order intake and

a strong opening order book for the second half.

Revenue decreased by 2.6% which was more than offset by a

£1.2M growth in the order book to carry into the second half. Interface revenues increased by £200K and

were impacted by weaker market conditions in Q1 although order intake increased

by 2.7% due to improved market conditions in Q2. Precision, control and intelligence revenue

fell by 9.5% reflecting the caution of dairy farmers to commit to capital

investment over the period. Strong order

intake over Q2 resulted in 11% growth in order intake over the period. There remains a growing pipeline of other

opportunities in this market as the improving trading conditions support

farmers looking to invest and deliver improved farm efficiency.

Farm Services revenue remained broadly flat. They are more resilient to the dairy market

cycle but during the period they have seen a greater level of farm

consolidations and closures. They have

continued to convert farms to Farm Services but this has been offset by wider

market dynamics. They anticipate a

return to growth in the second half.

During the period they have taken the opportunity to

consolidate all EU commercial operations into the existing Italian

facility. This provides a single

customer service point for all three lines of the business and at the same time

they have also transferred the European liner production in house to support

their operational efficiency.

The main on-recurring item relates to the £2.9M increase in

pension liabilities following the GMP equalisation ruling.

As a result of the strong momentum in Avon Protection and

despite the performance in the first half being adversely affected by the US

government partial shutdown and challenging dairy market conditions, the board

remains confident in delivering full year expectations. The opening order book for the second half of

£59.1M represents a 38% increase compared to the same point of last year. The opening order book and mask system

contract provide strong visibility into the second half of the year and the

board remain confident in delivering full year expectations. Avon Protection revenues are expected to

grow mid-single digit basis and with rebounding milk prices a stronger second

half for the dairy division should result in flat revenues for the year.

At the current share price the shares are trading on a PE

ratio of 21.8 which falls to 18.5 on the full year consensus forecast. At the period-end the group had a net cash

position of £46.8M compared to £46.5M at the end of the year. After a 30% increase in the interim dividend

the shares are now yielding 1.2% which increases to 1.5% on the full year forecast.

On the 2nd May the group announced that

non-executive director Petrus Vervaat purchased 2,500 shares at a value of

£36K.

Overall then this has been a difficult period for the group. Profits declined, net assets reduced and the operating cash flow fell, although there remained a decent amount of free cash generated. There were problems across both divisions. Protection was affected by the US government partial shutdown and the dairy division by a poor milk market and prices. For the second half, these issues seem to have mostly been resolved and there is a good opening order book. A forward PE of 18.5 and yield of 1.5% is not cheap but this is a quality company and I am minded to hold on.

On the 7th August the group announced that it had

signed an agreement to acquire 3M’s ballistic protection business and the

rights to the Ceradyne brand for an initial cash consideration of £75M and a

further contingent cash consideration of up to £21M.

The business is a leader in critical personal protective

equipment with established positions with the US DOD and has existing contracts

for next generation ballistic helmets and body armour. It operates from three sites in the US and

last year made an EBITDA of $10.8M.

Recurring annual cost synergies of around £4M are expected to be

delivered in the first full year of ownership from integrating IT systems and

back office functions. The one-off costs

to implement this are expected to be around £8M.

The acquisition is expected to close in the first half of

2020.

On the 16th September the group released a

trading update covering the year where they noted that trading in the second

half continued in line with expectations.

Revenues are expected to grow by 4% on a constant currency basis with

the EBITDA margin modestly ahead of last year.

The protection division had a strong year, underpinned by the

performance of the military business.

They have completed the planned initial deliveries of the M69 aircrew

mask and the M53A1 mask and powered air system to the US DOD. They have also completed the $16.6M ROW mask

system contract announced in April.

Law Enforcement performance has been stronger in the second

half but the impact of delays resulting from the extended US government partial

shutdown in the first half will result in a year on year revenue decline. Fire performance in the second half has been

further impacted by delays in the NFPA approval process for the new safety

standard, which has prevented the launch of their upgraded Magnum SCBA. They now expect to launch it in the first

half of 2020.

The improved global dairy market conditions experienced in

Q2 have continued into the second half, resulting in improved trading

conditions. This has resulted in the business

returning to revenue growth across all lines.

The US DOD contract awards totalling $340M for the M53A1 and

M69 mask systems along with the acquisition of 3M’s ballistic protection business

has strengthened the medium-term outlook which leaves the group well positioned

to deliver further growth.

Photo-Me has now released their interim results for the year ending 2019.

Revenues decreased when compared to the first half of last year as a £4.3M growth in European revenue was more than offset by a £6M decline in UK and Irish revenue and a £745K fall in Asian revenue. Depreciation and amortisation grew but other cost of sales declined to give a gross profit £2.7M lower. The group did not make the £2.2M sale of land that occurred last time, there was a £1.2M detrimental swing to forex movements and other admin expenses grew by more than £1M which meant that the operating profit was £7.2M lower. The group did gain £3.2M on the disposal of Stilla Tech but suffered a £2.7M mark to market loss on the Max Sight valuation. Other finance costs also increased but tax charges were down £2.8M to give a profit of £20.1M, a decline of £4.1M year on year.

When compared to the end point of last year, total assets increased by £20.1M, driven by a £29.9M increase in cash, a £4.5M growth in goodwill, a £1.6M increase in financial instruments and a £1.3M growth in property, plant and equipment, partially offset by a £4.5M decline in current tax assets, a £6M fall in financial assets, a £3.8M decline in receivables and a £2.5M fall in inventories. Total liabilities also increased during the period due to an £23.5M growth in borrowings and a £10.5M increase in payables. The end result was a net tangible asset level of £103.1M, a decline of £14.3M over the past six months.

Before movements in working capital, cash profits declined

by £992K to £39.2M. There was a cash

outflow from working capital so the net cash from operations came in at £31.1M,

a decline of £3.7M year on year. The

group spent £4M on acquisitions but received £4.4M from the disposal of an

associate and £1.6M from the repayments of loans advanced to the

associate. They spent £1.3M on

intangible assets and £12.8M on property, plant and equipment to give a free

cash flow of £19.5M. Of this, £14M was

paid out in dividend and again the group took out a large chunk of new

borrowings (£26.7M) to give a cash flow of £29.4M and a cash level of

£88.6M. It is quite hard to understand

the reason for the new borrowings in my view.

The operating underlying profit in Asia was £2.7M, a growth

of £348K year on year, although Japanese restructuring costs were £1.2M which

meant the actual profit was £1.5M, a fall of £859K. Revenue reduced by 3% which was a decent

performance given the challenges in the Japanese market. Admin functions were streamlined, low revenue

machines were relocated and unprofitable units removed. The business recovered faster than expected

and is now performing well. Trading in

the other countries in Asia remains strong.

In the second half the group will see the full benefit from

the restructuring programme. Whilst the

market in Japan remains highly competitive, the board continue to believe there

are growth opportunities and they intend to start the deployment of their new

units which have a significantly lower production cost than the units deployed

previously and will offer a 35% faster return on investment.

The operating profit in Europe was £20.7M, a decline of £1.8M

when compared to last year which is being put down to last year’s French litigation

outcome. The group remains in

discussions with the French government regarding the extension of its secure

photo ID transfer technology to include photo ID for new passports and ID

cards. Advanced discussions continued

with the Dutch government regarding deployment of their technology for use in

driving licences in the Netherlands. The

laundry business continued to perform well, including a first time contribution

from La Wash.

The operating profit in the UK and Ireland was £4.5M, a

decrease of £2.8M year on year. This was

due to large order lags in B2B and third party sales activities which should be

recovered in the second half. The

restructuring of Photo-Me retail had a negative impact on revenue and there was

some impact on revenue from the removal of unprofitable children’s rides The group diversified its photobooth services

with the roll out of secure digital upload technology for Irish Online passport

renewal and British passport renewals.

In total, 2,950 photobooths are now enabled for UK passport renewals

with a target of 4,000 by the end of December.

The acquired business made a pre-tax profit of £315K during

the period.

ID revenue increased 1% with a 1% growth in the number of

units in operation. The group now has

more than 10,000 photobooths connected to government organisations for the

secure upload of photo ID and it is expected that this number will continue to

grow as discussions with Governments progress.

New services have been introduced to a small number of booths in the UK,

Ireland and France, enabling customers to scan and copy documents. They are monitoring customer response.

Total revenue from laundry increased by 26%. The rollout of Revolution machines continues

with the estate increased by 30%. The

UK, Ireland, Portugal, France and Spain remain key geographies for growth and the

group is looking to extend operations into Germany and Austria. They are still on track to deploy 6,000 units

by the end of 2020.

The number of kiosks in operation have reduced by 7% and

revenue from kiosks was down 27%. This

was primarily due to the restructuring of Photo-Me Retail, which resulted in

the removal of machines located in shops which were closed. These units were transferred to Photomaton in

France and have been refurbished prior to being deployed to replace previous

generation machines in the country.

While the machines have improved revenue following relocation to France,

there was a period of time when the machines were not operational.

The board foresees that in the short term the negative

impact of the uncertainty surrounding Brexit and the UK economy could also

spill over into their UK operations. In

the long term, potential re-nationalisation of UK ID documents as well as

strengthened immigration regulations could lead to increased requests for the

group’s secure ID products.

After the period-end, the first banking booth which provides

retail banking services to customers was launched in partnership with

Anytime. The first ten booths were

opened in Paris, allowing customers to open a bank account and scan in

supporting documents. It then takes two

days for a new account to be opened once compliance checks have been

completed.

In May the group acquired La Wash group, for a consideration

of €5M. It is a Spanish business to

business laundry service company based in Barcelona. The acquisition generated

goodwill of £4.4M. A further £219K of

consideration is payable to the vendor of the acquired business.

During the period the group made net gains of £560K which

included the gain of £3.2M on the disposal of Stilla Technologies, an

associate, and the market to market loss of £2.7M arising on the fair valuation

of Max Sight Holdings.

During the period the group has been impacted by reduced B2B

revenue and machine sales activity, especially in the UK, where they have

suffered from large order lags. They

expect this to recover in the second half of the year. The strong performance in Japan and the

continued positive momentum of their high margin laundry business gives the

board continued confidence in their pre-tax guidance of £44M for the year. Their ability to meet guidance will be

reliant on normalised trading conditions in their key markets.

At the current share price the shares are trading on a PE

ratio of 10.5 which falls to 10.4 on the full year consensus forecast. After the interim dividend was kept the same,

the shares are yielding 8.9% which is forecast to remain the same for the full

year. At the period-end the group had a

net cash position of £32.4M compared to £26.7M at the year-end.

On the 3rd April the group released a trading update

covering the year. Their operations in Europe and Asia are continuing to grow

in line with expectations. The strong

performance in Japan has continued into the second half of the year, following

the reorganisation.

Overall trading in the UK has become more challenging than

expected reflecting the slowdown in consumer activity as a result of continued

uncertainty around the Brexit negotiations.

This has meant that the expected recovery in B2B machines revenue is not

now expected to materialise this year.

As a result, the board believes that pre-tax profit will be slightly below

previous guidance of £44M and will instead be just above £42M.

On the 25th April the group announced that it had

acquired a 96% share in Sempa, a French company that specialises in commercialised

self-service fresh fruit juice equipment.

The gross consideration payable for the acquisition is €20.6M, funded by

a new debt facility of €20M (why isn’t

the group using its existing cash resources?).

The business is the leader in France for the

commercialisation of self-service fresh fruit juice equipment. They operate via a lease model whereby they

sell equipment to customers via lease finance agreements. They receive full payment on sale of the equipment

and the lease finance contracts are then subject to renewal every year.

Sempa’s pre-tax profit last year was €3.7M and it had gross

assets of €9M. The acquisition is

expected to be earnings enhancing in 2020 and is expected to contribute around

€3.7M in pre-tax profit.

Overall then this has been a bit of a tricky period for the

group. Profits were down, net assets

decreased and the operating cash flow declined.

The group apparently made a decent amount of free cash but the cash position

here continues to confuse me. Why take

out more loans when there appears to be a huge amount of cash on the balance

sheet. I don’t understand. The underlying business in Europe seems to

be performing decently, and the performance in Japan seems to be recovering

more quickly than expected.

Brexit-related uncertainty is putting a drag on UK results,

however. The Sempa acquisition seems

good, but again why take out more loans when the group could easily afford it

out of their cash reserves? The shares

look good value, with a forward PE of 10.4 and yield of 8.5% but I just feel a

little uneasy.

James Halstead has now released its interim results for the year ending 2019.

Revenues declined by £238K but costs of sales were down £852K to give a gross profit £614K higher. Finance costs declined by £177K by tax charges were up £182K which meant that the profit for the period was £19M, a growth of £609K year on year.

When compared to the end point of last year, total assets increased by £343K, driven by a £12.1M growth in cash partially offset by a £7.4M decline in inventories and a £5.1M decrease in receivables. Total liabilities increased during the year, mainly due to a £3.6M increase in the pension obligations and an £855K growth in current tax liabilities. The end result was a net tangible asset level of £121M, a decline of £4.6M over the past six months.

After movements in working capital the operating cash flow

increased by £18.2M. After an increase

in tax payments the net cash from operations was £34M, a growth of £18.1M year

on year. The group spent £2M on capex to

give a free cash flow of £32M. Of this,

£20.1M was spent on dividends to give a cash flow of £12M and a cash level of

£62.8M at the period-end.

In terms of sales, every month showed an increase on the

comparative except December when larger customers were exercising stock

control. Despite this, sales overall

were 3.9% ahead. Export markets were

mostly strong but with Central Europe showing a decline of 1.7% but the start

of the second half has shown a return of solid growth.

Gross margin improved as a result of a better product mix

and favourable plant performance, although it was impeded to some extend by raw

material price increases. Raw material

inflation was only around 3%, whereas last year it was 18%. The group made a significant investment in

new sheet vinyl ranges and in Germany they are taking market share with 15%

growth in homogenous sheet vinyl.

Palletone, launched in May 2018, continues to gain traction. Investment continues with new showroom

facilities having been opened in Cologne to provide greater market support to

customers.

Going forward, obviously Brexit hangs over everything and

there are many complications beyond the practicalities of port entry

delay. Management has spent extensive

time considering the possible implications and they have made appropriate stock

adjustments as a contingency. The start

of the second half has seen a good increase in sales and their newer ranges

continue to increase their market penetration.

In January they introduced further ranges to the market which have been

well received. The board have confidence

in their continued progress through the year.

At the current share price the shares are trading on a PE

ratio of 29.6 which falls to 27.8 on the full year consensus forecast. After a 3.9% increase in the interim dividend

the shares are yielding 2.6% which increases to 2.9% on the full year forecast. At the period-end the group had a net cash

position of £62.8M.

Overall then this has been a bit of a subdued but steady period. Profits were up due to good controls on costs, and the operating cash flow improved with a good amount of free cash being generated. Net assets saw a decline, however. Raw material cost inflation has become much more manageable and most markets seem stable despite Brexit looming. All this stability comes at a price, however, and the forward PE of 27.8 and 2.9% yield is certainly not cheap. Would definitely be worth an investment if the price is right.

On the 10th May the group announced that non-executive director Michael Halstead sold 100,000 shares at a value of £510K. On the 15th May it was announced that non-executive director Michael Halstead sold 120,000 shares at a value of £610K.

On the 30th July the group released a trading

update covering the year as a whole.

Sales were ahead of last year despite difficult trading conditions. Flooring installations throughout the year were

wide ranging such as Harrow School, Euro Disney’s Hotel and Chanel concessions

across the globe. The healthcare

business continues to make good progress and projects completed included Poissy

Hospital in France and the Quillota Hospital in Chile. UK turnover was 7% up in a market that seems

to be quite robust despite the high street retail issues.

In Europe competition is ever increasing with new entrants

selling an increasing array of flooring.

In the German market the group have retained market share but turnover

was at a lower level. There are markets

with double digit growth, however, and France, South America and the

Netherlands are examples.

Raw material prices are stable and the availability problems

of last year have ameliorated and working capital remains robustly managed with

their cash generation secure.

AG Barr have now released their final results for the year ended 2019.

Revenues increased when compared to last time as a £5.7M decrease in still drinks revenue was more than offset by a £7.2M growth in carbonates revenue. Cost of inventories grew by £10M to give a gross profit £8.2M lower. Depreciation was up £700K but other operating expenses fell by £10.2M. There was no gain on the sale of a distribution site, which netted £2.5M last time and there was a £700K GBP pension equalisation charge. Offsetting this was £900K fall in the sugar reduction programme costs and £300K less reorganisation costs which meant the operating profit was £800K lower. Finance costs reduced by £400K but the tax charge was up £1M to give a profit for the year of £35.8M, a decline of £1.4M year on year.

When compared to the end point of last year, total assets increased by £10.3M driven by a £6.8M growth in cash, a £5.9M increase in plant, equipment and vehicles, a £2.4M growth in inventories and a £1.2M increase in trade receivables, partially offset by a £4.6M decline in assets under construction and a £1.2M decrease in software assets. Total liabilities also increased during the year as a £1.7M decline in pension obligations was more than offset by a £2.4M increase in trade payables. The end result was a net tangible asset level of £163.5M, a growth of £10.1M year on year.

Before movements in working capital, cash profits increased

by £2.5M to £55.1M. There was a cash

outflow from working capital but this was less than last time so after tax

payments increased by £1.6M, the net cash from operations was £44.4M, a growth

of £2.3M year on year. The group spent

£8.9M on capex to give a free cash flow of £35.5M. Of this, £10.3M was used to buy their own

shares and £17.9M went on dividends to give a cash flow for the year of £6.8M

and a cash level of £21.8M at the year-end.

The gross profit in the carbonates division was £100.1M, a

growth of £6M year on year, driven by Irn-Bru, Barr Flavours and Rubicon Spring. The Barr flavours range has made excellent

progress and the board expect to deliver further progress in 2019 due to

increased levels of distribution gained in the second half of 2018

The gross profit in the still drinks and water division was

£14.7M, a decline of £1.4M when compared to last year. While the performance of Rubicon still juice

drinks has been impacted by the overall decline in the fruit drinks category,

the brand as a whole has grown by nearly 8% in volume terms reflecting the

significant growth of Rubicon Spring. Strathmore

gained less benefit from the significant weather related demand across the hot

summer months and was impacted by competitive pricing.

The gross profit in the other division was £7.7M, an

increase of £300K when compared to 2018.

The Funkin business continued its strong growth trajectory with revenue

growth of 9%. They made significant

progress across core business development in the on-trade along with the

exciting launch of draught cocktails, initially focused on outdoor events and

now expending into higher volume on-trade pubs, bars and restaurants. Following their initial entry into the home

cocktails market with the growing Shaker Pack product, the next step will be

the launch of nitro cocktails in can format which will be launched into the

market in the first half of 2019, further supporting their strategy of building

the brand from its existing strong base in the on-trade into the wider consumer

market.

This was a tricky year for the market. Carbon dioxide shortages during a period of

hot weather, snow disruption and a number of customer business failures

together with the implementation of the soft drinks levy led to significant

changes in pricing, promotional and demand factors in the wider market.

The implementation of the levy has led to distortions in

both value and volume performance in the market. Unit pricing changes and

shifts in promotional dynamics have been evident across the full year. The total UK soft drinks market saw value up

8.1% and volume up 3%. This was

particularly evident in the carbonates category where value grew 11.6% and

volume increased by 2.7%. In regular

colas, value grew 1.9% while volume declined by 22%. The only sector in decline was juice drinks

which continues this long term trajectory as consumers choose water, flavoured

water or traditional carbonates. Overall

Barr soft drinks volume share grew by 11%.

Last year saw the reformulation of the group’s biggest

brands and the implementation of the soft drinks levy. The group placed an intentional short term

trading focus on volume across the core carbonates business as they established

where market pricing and promotions would sit after the levy came in. This has given some short term boosts to their

volume growth.

The group expect to see the overall soft drinks market

performance stabilise in 2019 as the comparisons start to include the

levy. They expect to revert back to

their long-term strategy of value over volume as they do so.

They have seen a significant amount of change in their

partnership brands across the period.

They launched new partnerships with Bundaberg and San Benedetto in early

2018 which have got off to a strong start with the brands making good progress. The Snapple brand has not made as much

progress as they would have liked but the change in ownership of the parent

company has led to a positive change which they hope will lead to a more

autonomous position for the group allowing them to focus on growth over the

long term.

Rockstar progress has slowed in the period, down 3.1% in

volume terms in a challenging marketplace where significant competitive

investment and activity have dented the strong prior year performance. The group expect to launch a number of new

Rockstar products in order to regain sales momentum. They have regained momentum in their

international sales performance with revenue growth of 8.6% as their business

development plans delivered strongly in Ireland, Sweden and Germany.

The board forecasted that operating margin would see a

moderate reduction as they continued to support brand development, innovation,

customer service and flexibility. They

were also impacted by unplanned CO2 shortages, unprecedented seasonal demand

which led to suboptimal operating conditions and additional operating costs

during the summer months. Going forward

they expect moderate cost inflation in the coming year which they expect to

offset through “management actions” (whatever that is) which should see margins

stabilise.

Given the largely UK-based sales profile, the current

assessment is that the specific issue of the Brexit will not have a significant

impact on the business other than through its effects on forex and the

procurement of raw materials

During the year there was a charge of £700K for the past

service cost in respect of the equalisation of GBP benefits following a high

court judgement.

As far as capex is concerned, the major project this year

has been the replacement and upgrade of the liquid to line processes in the

Cumbernauld factory. Cash spend on this

£13M investment was lower than originally planned due to rephrasing of both

operational activity and supplier payments, however the project remains on

schedule with commissioning planned for 2020.

As a consequence, capex in 2020 is expected to be higher than previously

guided.

For Brexit, a steering group has considered the implications

both for transition disruption in the 3-4 months after an exit and for the

longer term strategy. Action has been

taken to mitigate short term transitory issues by increasing forex coverage and

inventory levels of strategic raw materials.

Given the UK focus of the commercial activities and the largely UK

sourced supply base, the current assessment is that an exit from the EU will

not have a significant strategic impact on their business and is not a

principal risk.

Going forward, the political and economic climate in the UK

indicates that 2019 will be another uncertain year for UK-based

businesses. For soft drinks this is

likely to be made all the more challenging by further regulation and ever

changing consumer dynamics. Despite

this, the board have confidence in their growth strategy.

At the current share price the shares are trading on a PE

ratio of 26.3 which reduces to 25.2 on next year’s consensus forecast. After a 7% increase in the dividend the

shares are yielding 2% which is forecasted to remain the same next year. At the year-end the group had a net cash

position of £21.8M compared to £15M at the end of last year, which was higher

due to the change in timing of the capex investments and share buy-backs.

Overall then this seems to have been a decent year in a fairly tricky market. Profit was down but this was due to last year’s distribution site sale, otherwise it would have increased. Net assets grew and the operating cash flow improved with good free cash generation (although capex will rise next year). The carbonates and other business is doing well but the stills sector is struggling somewhat due to a general fall in the juice market. The group seems to have successfully overcome Co2 shortages and the soft drinks levy but this performance comes at a price and the shares look pricey with a forward PE of 25.2 and yield of 2%. This should be a great investment at the right price.

In May it was announced that commercial director Jonathan

Kemp sold 4,000 shares at a value of £33K.

On the 7th June the group announced a minority interest investment in new business start-up Elegantly Spirits, owner of the Stryyk brand which has a portfolio of zero proof spirits. As part of the investment, Funkin has entered into a long term agreement on normal market terms to act as a distributor for all Elegantly Spirit products and the group are investing £1M for a 20% stake. The business was recently formed by the original founders of Funkin….

On the 16th July the group released a trading

update covering the first half of the year.

Trading so far has been below management expectations. This has been exacerbated by some specific brand

challenges, particularly in Rockstar energy and Rubicon juice drinks, as well

as some disappointing spring and summer weather.

They have taken action to address the specific brand issues,

including the planned launch of three new Rockstar products at the end of the

summer, and recipe improvement activity for Rubicon but the benefit of these

actions will not be felt until later in H2.

In a transitional pricing year for their core carbonates

portfolio, they are seeing positive indications of acceptance of the new price

positioning. Funkin continues to perform

strongly and the recent launch of nitro-infused premium cocktails in cans is already

exceeding expectations.

Revenue is expected to be 10% down on last year. Despite the strong second half plan, it is

not expected that they will fully recover from the volume impact in the first

five months of the year and the current trading they are experiencing. As a result the board expect profit to be 20%

lower in the full year. It is also expected

that there will be some exceptional costs incurred in the current year as they

take action to regain momentum.

Spectris have now released their final results for the year ended 2018.

Revenues increased when compared to last year as a £34.2M decline in industrial controls revenue was more than offset by a £76.2M growth in materials analysis revenue, a £35.3M increase in test and measurement revenue and a £1.3M growth in in-line instrumentation revenue. Depreciation was up £4.7M and other cost of sales grew by £34M to give a gross profit £39.9M higher. Indirect production and engineering expenses declined by £10M but sales and market expenses were up £15.7M, acquisition related costs increased by £11.8M and other admin costs also grew which meant that the operating profit was £6M lower. There was a £44.2M reduction in the profit on business disposals and an £8.5M increased loss on retranslation of intercompany loans arising from Sterling’s strengthening against the dollar, along with a £2.4M increase in interest payable on loans. Tax charges were down £10.8M, however, to give a profit for the year of £185.2M, a decline of £49.6M year on year.

When compared to the end point of last year, total assets increased by £294.3M driven by a £138.8M growth in goodwill, a £40.4M increase in inventories, a £38.9M receivable from a joint venture, a £42.6M growth in trade receivables, a £35.1M increase in the value of trade names, a £30.9M increase in freehold properties and a £23.8M growth in plant and equipment, partially offset by a £64.8M decline in cash and a £28.6M decrease in assets held for sale. Total liabilities also increased during the year due to a £177.2M growth in bank loans and a £36.7M increase in contract liabilities. The end result was a net asset level (excluding goodwill) of £277.5M, a decline of £155.9M year on year.

Before movements in working capital, cash profits increased

by £12.2M to £267.2M. There was a cash

outflow from working capital and after interest payments increased by £4.7M but

tax payments reduced by £9.3M the net cash from operations declined by £17.2M

to £168.7M. The group spent £97M on

fixed assets and spent a net £152.6M on acquisitions to give a cash outflow of

£72.7M before financing. The group also

paid out £68.2M in dividends and £100.5M on share buy-backs and to finance this

they took out new loans of £175.5M. The

end result was a cash outflow of £65.2M and a cash level of £67.3M at the end

of the year.

The operating profit in the Materials Analysis division was

£72.1M, a growth of £3.5M year on year on sales that increased by 16%

reflecting an 8% increase in like for like sales, a 10% contribution from

acquisitions and a 2% negative impact from forex movements. Sales growth was driven by strong demand in

Asia, particularly in China, South Korea and India with a notably stronger

performance in the second half. In North