I feel it is now time to revisit one of my earlier investments that I had sold out of. Swallowfield develops and supplies personal care and beauty products. Nearly half of all sales are Aerosols, with roll-ons coming in second. They have released their final results for the year ending 2014.

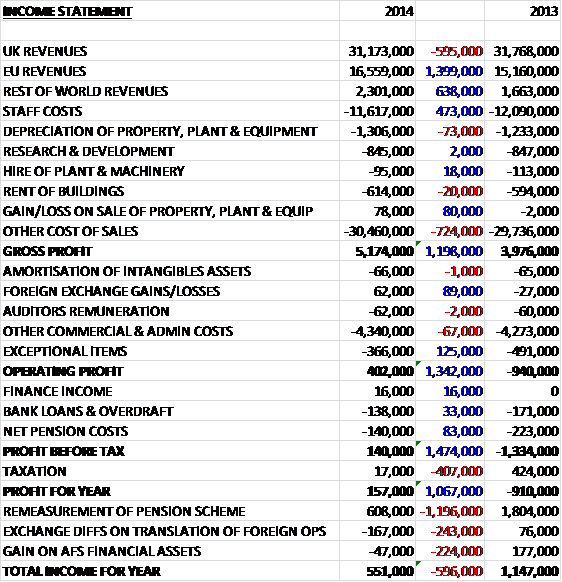

Revenues increased when compared to last year as a £1.4M growth in European sales and a £638K increase in ROW revenues were somewhat offset by a £600K decline in UK revenues. Staff costs fell year on year but other cost of sales increased so that gross profit was £1.2M higher than in 2013. There was a benefit of currency movements and a £125K reduction in “exceptional items” which this year relate to £264K of accelerated depreciation at the Bideford site and a £92K accrual for employee redundancies, somewhat counteracted by a small increase in other admin costs so that operating profit was £1.3M higher. After falling loan and pension costs took their toll and the group received a lower tax rebate (there are still £1M of tax losses that could potentially be utilised), the profit for the year ended up at £157K, a big swing from the £910K loss last year.

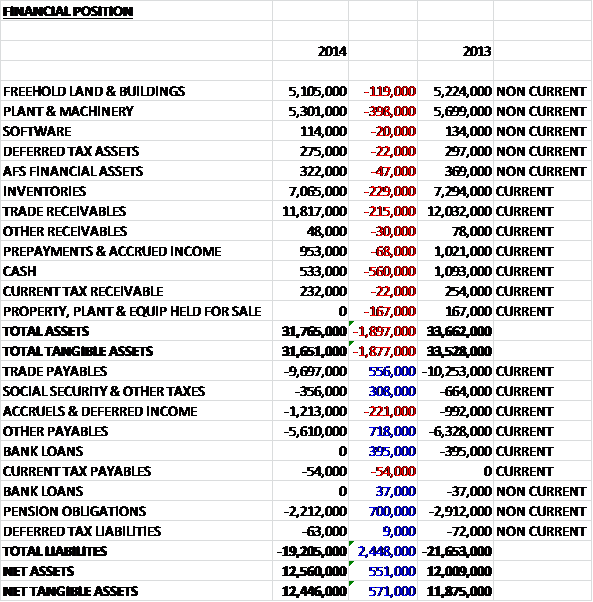

When compared to last year, total assets fell by £1.9M as every asset class declined in value with cash down £560K, plant & machinery falling by £398K and the £167K warehouse the group finally managed to flog. Liabilities also fell as a £718K decline in other payables, a £700K fall in pension obligations and a £556K reduction in trade payables were partially offset by a £221K growth in accruals. Net tangible assets ended the year £571K up at £12.4M but there is also £3.3M worth of operating leases payable off the balance sheet, some £538K less than last year.

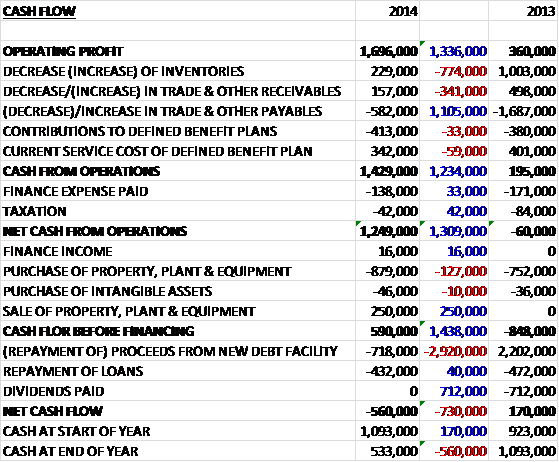

Before movements in working capital, cash profits increased by £1.3M to £1.7M. Working capital changes broadly cancelled each other so that cash from operations was £1.2M higher at £1.4M. After lower finance expenses and tax, the net cash from operations was £1.2M, an improvement on the £60K cash outflow last year. The bulk of this cash was spent on property, plant and equipment but £250K was received from the sale of tangible assets and free cash flow was £590K, a £1.4M swing compared to 2013. The group spent all of this cash, and then some, was spent on paying back debt to leave a net cash outflow of £560K for the year to leave the group with £533K cash at the end.

Over the year the retail markets in the UK and Europe remained challenging which impacted the toiletries and cosmetics sector, resulting in lower levels of consumer demand which led to a strong and prolonged period of promotional activity from the group’s competitors. Despite this, the decent momentum that occurred towards the end of last year continued into 2014, driving underlying net growth with new customer wins and product launches. Direct exports increased year on year with the growth coming from the US, South Africa, China and Europe.

The group are looking to drive specific categories where they see most growth, these include personal care aerosols, lip balms, deodorant sticks and roll-ons. New products are being developed that will be marketed under Swallowfield’s own brand and will be positioned to avoid any direct conflict with the existing customer base. Mysteriously they are also developing a new high growth, high margin product category that can become additional drive category by 2016. The other side of the strategy is to concentrate on costs and the group has consolidated their Bideford site into two buildings from three and relocated some lines to the Czech Republic which is expected to save £230K per annum.

Although progress has been made in this regard, the group still has two customers who account for more than 10% of total revenues, with one accounting for 15% and the other 11%. To put this into context, though, in 2012 the group had three customers that accounted for more than half of all business. The group is also somewhat susceptible to exchange rate changes as a 5% strengthening of Sterling would result in a £182K reduction in profits. The group already has £650K contracted for but not provided which seems like a fairly substantial investment for a company of this size. Other potential risks include the susceptibility to general economic conditions and any movements in input prices, although it should be pointed out that these are probably in the group’s favour at the moment.

During the year Edward Beale joined the board as a non-executive director. He is a chartered accountant and the CEO of City Group. Going forward the board expect the challenging retail market conditions in Europe and the UK to continue in the short and medium term. They are confident, however, that the new strategy along with new product developments and further efficiencies will gain momentum and improve profitability.

There was no dividend recommended this year but it is expected that next year’s dividend will yield 2.1% at the current share price. The board have indicated that at this time the dividend payment will be reinstated to align with the underlying earnings and cash flow of the business. The P/E ratio is 24.9, which is certainly not cheap but it seems growth is being priced in as the 2015 ratio is expected to be 10.8 which conversely seems good value. At the end of the year net debt stood at £5.1M, a £600K reduction on last year.

Overall then, this was a year of improvement for Swallowfield. Progress is being made, but the group is not there yet. Profits improved, as did the fairly decent balance sheet. Probably most importantly, a tight control on working capital kept the cash generation at a pretty decent level and the group did the sensible thing and used it to pay off debt, although more cash is really needed to make a decent dent and allow them to return to dividend payments. The focus on certain products seems fairly sensible and I do believe that Swallowfield has turned a corner. The fall in the oil price is helpful as this should help costs but the declining Euro is probably going to be a bit of a drag on some of those growing exports. Overall, one to watch but I would want to see a bit more evidence of further progress before jumping in.

On the 13th November the group released an AGM statement. Trading in the first four months of the year was broadly in line with expectations with momentum continuing with new customer wins and new product launches but this was been partially offset by the euro weakness and customer mix. The board expect there to be a significant weighting to the second half of the year, caused by phasing of new contract wins and natural seasonality and that full year profitability will be in line with current expectations.

For a company as small as Swallowfield, the share price tends to jump around a bit but the chart looks interesting in recent weeks as a short bullish run has crossed over both the 50 and 200 day moving averages. I am still not convinced the group will present a great set of results at the half year point but I am considering taking a small position for the long term.

On the 9th February it was announced that the largest shareholder, Peter Gyllenhammer purchased 22,500 shares at a cost of about £23K. He now owns over 26% of the company. This is clearly a modest buy from someone with Gyllenhammer’s means but it strikes me as a good vote of confidence in the company so I have taken this as a trigger to take up the small position I spoke of above.