Swallowfield has now released its interim results for the year ending 2016.

Revenues increased when compared to the first half of last year as a £1.6M decline in European revenue due to the weakness of the euro was more than offset by a £2.6M growth in UK revenue and a £485K increase in ROW revenue. Cost of sales increased modestly to give a gross profit £1.3M above that of last time. Commercial and admin costs grew by £843K but there was a £554K pension scheme curtailment gain which meant that the operating profit was £1M above that of the first half of 2015. Finance costs crept up and tax was £100K higher as it is anticipated that the UK taxable profits will be above the brought forward tax losses which will mean they will be fully utilised now, to give a profit for the half year period of £960K, an increase of £911K year on year.

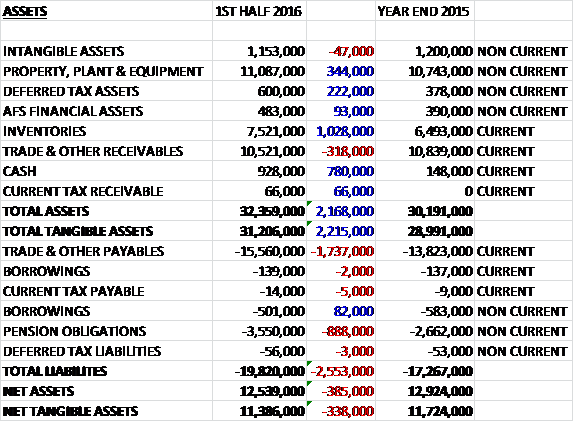

When compared to the end point of last year total assets increased by £2.2M driven by a £1M growth in inventories, a £780K increase in cash, a £344K growth in property, plant and equipment and a £222K increase in deferred tax assets due to the increase in pension obligations, partially offset by a £318K decline in receivables. Total liabilities also increased during the period due to a £1.7M growth in payables and an £888K increase in the pension obligations due to a reduction in bond yields. The end result was a net tangible asset level of £11.4M, a decline of £385K over the past six months.

Before movements in working capital, cash profits increased by £557K to £1.3M. There was a small cash inflow through working capital but this was less than last year so that after a £254K detrimental movement in income tax, the net cash from operations was £1.6M, a decline of £1.1M year on year. This was more than enough to pay for capex, though, and free cash flow was £740K which covered the dividends of £226K but the group still took out more debt of £346K, however, which meant that the cash flow for the period was £780K and the cash level at the period-end was £928K.

Overall the performance was in line with board expectations. The core contract manufacturing business delivered growth in both sales and contribution margin and within the owned brands, the group integrated the Real Shaving brand and executed launches of the Bagsy and MR. brands into Debenhams and Boots respectively.

The group has focused resources on the “drive” and “build” product categories at the expense of the service product categories which they are seeking to exit. The drive categories include personal care aerosols, hot pour products and roll-ons whilst the build categories include cosmetic pencils, fragrance, gifting and premium liquids. During the period the drive and build categories delivered a combined 9% sales growth with a strong margin growth from the drive categories in particular.

The group have introduced a number of new products across a range of key customers and also secured agreements for future supply of several innovative haircare products to major premium brand owners which will positively impact business performance in 2017. They have also seen growth in volumes from their plastic aerosol foaming shower gel which was introduced last year. Furthermore, they delivered their first order under a partnership arrangement entered into with a leading US aerosol manufacturer. This arrangement enables the production of Swallowfield formulation in the US in a cost efficient way to allow European based customers to launch their products into the region which enables the group to receive a commission.

The Real Shaving Company brand has been fully integrated into the business and both sales and margins are contributing positively. A new aerosol product was added to the range and launched in October in the UK and will be introduced in Canada in the spring. A new sampling campaign will be executed in H2 and the group have entered into a sponsorship package with Somerset County Cricket Club.

The premium beauty brand, Bagsy, was rolled out in October to 36 Debenhams stores on full display units. Sales have been building steadily and there are a number of in-store promotions planned through the spring and summer. Further distribution extensions are being worked on, both in the UK and internationally, and the group have entered into an agreement with the fashion designer Savannah Miller which will result in a number of new products to be launched later in the year under the name Savannah Miller for Bagsy.

The new male haircare brand, MR, was launched into 350 Boots stores in October and sales have also been building steadily. Again, a range of in-store promotions and digital advertising through the spring and summer are expected to build further consumer awareness and sales. The value brand Tru continues to generate sales in existing outlets and the group are looking to further extend its retail distribution.

The board have identified a project to implement an upgrade of the group’s energy and waste infrastructure at the main Wellington site which aims to generate savings of about £150K per annum. This work is now underway with the installation of a new compressor and boiler complete and waste treatment trial in progress. This is expected to be completed during the current year.

During the period the group had one customer representing over 23% of total revenues. This represents a clear risk but apparently it reflects the timing of new launches and strong re-orders falling in the first half of the year which is expected to normalise over the full year – does this mean revenues are likely to be lower?

During the period the group recognised a credit of £770K relating to a curtailment gain which represents a reduction in liabilities on close of the defined benefit pension scheme to future accrual. One-off costs of £220K were incurred during this closure process which gives a net gain of £550K. The last scheme funding valuation which took place in April 2014 revealed a funding deficit of £1.3M which meant the company agreed to pay £108K per annum over ten years to eliminate the deficit which the valuation due to take place in 2017. The pension scheme is actually quite large given the size of the company with the total value of obligations standing at £23M.

Despite challenging retail conditions and the increasing macro-economic uncertainty, the board expect to see continued growth in both sales and profitability for the full year.

Net debt at the period-end stood at £4.9M compared to £5.4M at the end of last year. At the current share price the shares are trading on a hefty PE ratio of 27.1 which reduces to 14.7 on the full year forecast. After the reinstatement of the interim dividend, the shares are yielding 1.6% which increases to 1.7% on the full year forecast.

Overall then, this was a period of good progress for the group. Profits were up but net assets fell due to an increase in pension obligations. The operating cash flow also declined but this was due to a less favourable movement in working capital and cash profits increased with a decent amount of free cash being generated. The core contract manufacturing business seems to have performed well but there are no details about the contribution from the own brands, but I suppose it is early days. There is still a decent amount of debt here and the pension scheme is an omnipresent issue which means the forward PE of 14.7 and dividend yield of 1.7% doesn’t appear that cheap. Despite this, I feel there is enough momentum and quality here to justify this price so I am continuing to hold.

On the 6th June the group announced the acquisition of Brand Architekts and a placing in order to raise £8.6M which was significantly oversubscribed.

Brand Architekts owns and manages a portfolio of mid-premium beauty and personal care products that are sold in major UK high street retailers as well as through export. The business generated pre-tax profits of £2M last year and will be a transformational acquisition, being immediately earnings enhancing.

The majority of its sales are through major UK high street retailers, many of which are already existing customers of Swallowfield but further sales are made through export, notably to North America, Australia, Scandinavia and Turkey. Their key brands include Dirty Works, Kind Natured, Argan, Happy Naturals, DrSalts, Superfacialist and Senspa and they currently outsource production to suppliers in China. The two current owners will be entering into consultancy agreements for two years following the completion of the acquisition.

The total consideration for the acquisition is £11M, including contingent consideration of £1.85M and will come from the proceeds of the placing along with a modest extension of the current banking facilities.

The placing is to raise £8.6M at a price of 155p per share, a small premium to the share price the day before the announcement. The placing shares will represent about 33% of the total share capital following admission which means that the total voting rights will be 16,865,267.

The group’s current trading is in line with expectations, continuing the strong momentum in the first half of the year. The group’s owned brands continue to make good progress with further retail and online stockists added and the development of new marketing collaborations such as Bagsy with the fashion designer Savannah Miller and the Real Shaving Company with Somerset Cricket T20 Blast.

On the 11th July the group released a trading update covering the year ended 2016. They anticipate full year profitability will be towards the upper end of expectations. Overall revenues are expected to show growth of 10% having been bolstered by the strong performance of innovative new products introduced during the last year and the developing owned brands portfolio. This has also driven strong year on year growth in margin. There was a net debt position of £4.3M at the year-end compared to £5.4M at the end of the prior year.

The acquisition of Brand Architekts was completed after the year-end so had no impact on these figures. Initial feedback from customers regarding the new products has apparently been positive. Whilst the board are mindful of the broader economic and political environment as a result of the EU referendum, they are confident they can navigate any potential macro-economic uncertainty that may lie ahead.