Sylvania Platinum has now released their final results for the year ended 2017.

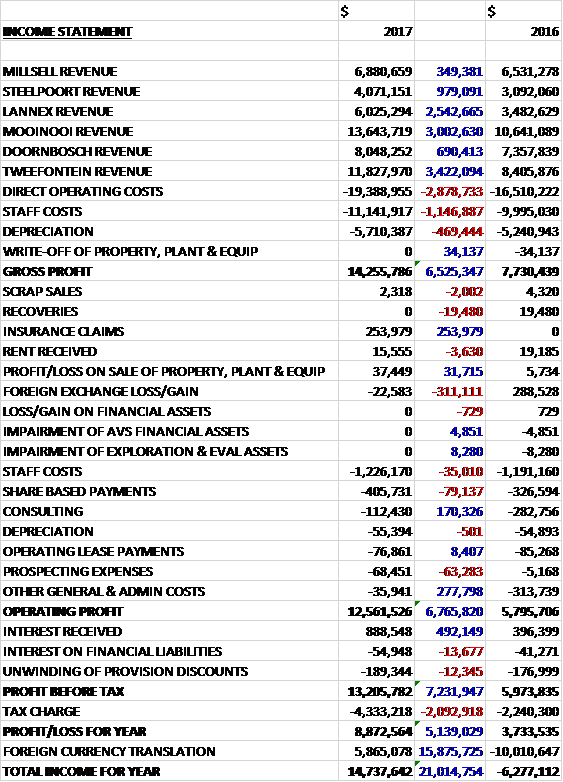

Revenues increased when compared to last year with considerable growth in Lannex, Mooinooi and Tweefontein. Direct operating costs were up $2.9M, staff costs increased by $1.1M and depreciation grew by $469K to give a gross profit $6.5M higher. The group received $254K in insurance claims but saw a $311K negative movement to forex losses. Consulting charges fell by $170K and other general costs reduced by $278K which meant the operating profit increased by $6.8M. The group also received $492K more in interest payments but tax charges grew by $2.1M to give a profit for the year of $8.9M, a growth of $5.1M year on year.

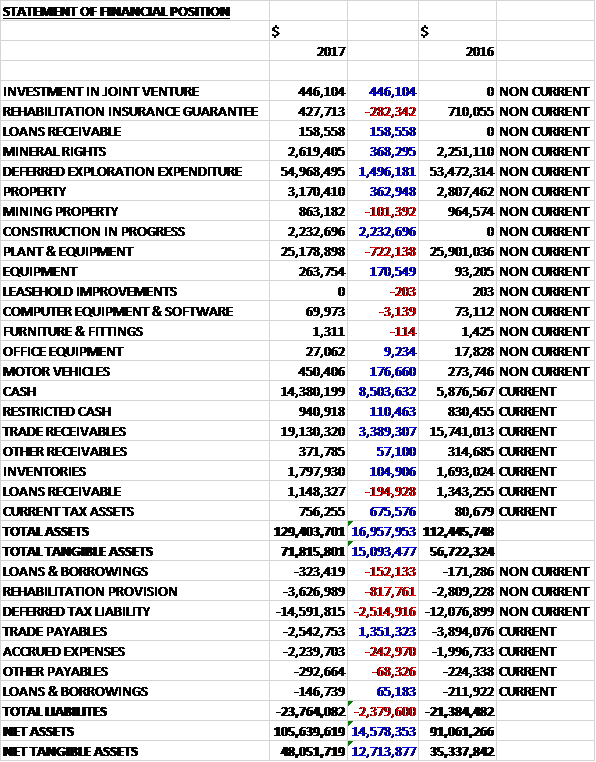

When compared to the end point of last year, total assets increased by $20M driven by an $8.5M growth in cash, a $3.4M increase in trade receivables, a $2.2M increase in construction in progress and a $1.5M growth in deferred exploration expenditure. Total liabilities also increased during the year as a $1.4M decline in trade payables was more than offset by a $2.5M increase in the deferred tax liability. The end result was a net tangible asset level of $48.1M, a growth of $12.7M year on year.

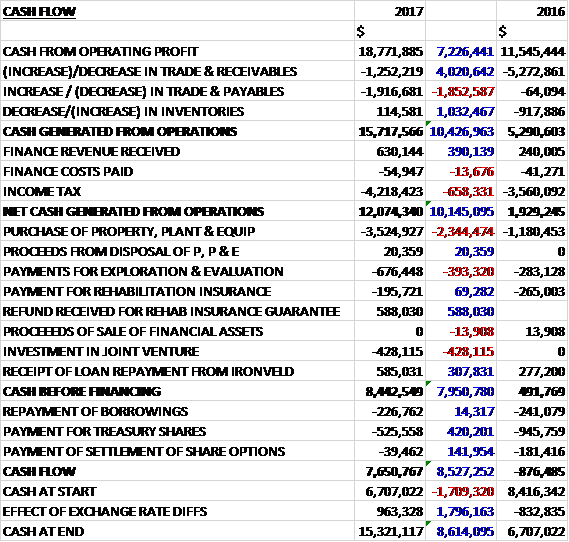

Before movements in working capital, cash profits increased by $7.2M to $18.8M. There was a cash outflow from working capital but this was lower than last time and after tax payments increased by $658K, the net cash from operations was $12.1M, an increase of $10.1M year on year. The group spent $3.5M on property, plant and equipment along with $676K on exploration and there was a free cash flow of $8.4M. Of this, $227K was used to repay loans and $526K to buy their own shares which gave a cash flow of $7.7M and a cash level of $15.3M at the year-end, which is a pretty good performance.

The profit at Millsell was $2.5M, a decrease of $317K year on year; the profit at Steelpoort was $78K, an improvement of $901K, the profit at Lannex was $667K, an improvement of $2.3M; the profit at Mooinooi was $3M, an increase of $4.3M; the profit at Doornbosch was $2.8M, broadly flat; and the profit at Tweefontein was $5.2M, a growth of $2M.

The basket price rose 10% year on year to $935 per ounce and production increased 17% to 70,869 ounces. Cash costs per feed tonne increased by 13% to $26 per tonne, impacted by a stronger ZAR/USD exchange rate but the higher ounce production resulted in a decrease in SDO cash costs by 3% to $426 per ounce.

PGM feed grades and tonnes both increased modestly during the year but the biggest contributor towards the record annual production was the 7% increase in PGM recovery efficiency from 43.2% to 46.4%. This was due to improved flotation technology, improved flotation stability and higher flotation mass pull strategy during the year enabled the improvement in the recovery efficiency.

Project Echo started during the year and by the year-end, $2.2M had been spent on the Millsell and Doornbosch MF2 modules. This is within the budget for this phase and it is expected that these expansion sections will be commissioned during the next six months. This will assist in filling the ounce gap from the scheduled closure of the Steelpoort operation that reached its end of life in June. The MF2 roll-out will lead to improved PGM recovery efficiencies, lower PGM production unit costs, increased cash generation and enable the SDO to extend its operating life and to sustain its production profile of around 70,000 ounces going forward.

In November the group entered into an agreement to establish the Tizer Sylvania Consortium which operates a pilot pelletiser plant in South Africa. They have a 50% interest for an initial consideration of $459K. The joint venture has not year earned any income or incurred any expenses.

At Harriet’s Wish, the intention to proceed with a water use license application has been delayed as transfer of the title deeds from the deceased original landowners to lawful occupants and descendants will need to occur in order to get the necessary permissions from landowners, as is a requirement for such an application.

At Nonnenworth, during Q3 the group reported that the rights to mine copper, gold, nickel and PGMs, as well as heavy minerals, iron and vanadium had been granted. The rights were subsequently executed and registered with the MTO. The process to transfer the right to mine heavy minerals, iron and vanadium to Ironveld is underway.

At Volspruit, during Q4 the group was granted the mining right to mine PGMs, gold, copper, nickel and chrome. The process is underway to execute the rights and have them registered with the MTO but mining can’t start without the Environmental Authorisation The group has pursued an appeal against the decision not to grant an EA for the project. To date no decision has been forthcoming. The group intends to proceed with a WULA but this will require preliminary detailed civil designs of all dam facilities which will incur additional costs. It has therefore been postponed pending the decision on the EA.

At Grasvally, an amendment to the existing prospecting right to include processing of the old waste rock dumps was granted in Q1 but the MR lodged in 2016 is still awaited. Currently the WULA for the project has not yet been granted. The group was issued notification in Q2 that the EA for the project had been granted but this was appealed. In Q4 they were informed that the appeal was set aside so the EA for processing the waste rock dumps stands.

They began extraction of a Chrome bulk sample during Q3. The plan is to extract 15,000 tonnes of ROM and at the year-end, a total of five bulk sample open pits had been blasted with total excavated ROM stockpiles measuring 6,167 tonnes. The remainder is to be extracted once the beneficiation testing of the initial stockpiles is finalised. The initial results were positive, but a decision has been taken to move beneficiation to a more suitable plant in Steelpoort to better liberate the chrome from the ore.

After the year-end, in July, the group announced that it reached a conditional agreement with Pan African Resources to acquire Phoenix Platinum for $6.6M.

Going forward, based on current resources, plant infrastructure and operational performance, there should be similar production performance in 2018 and with the roll out of project Echo the group should be able to maintain production levels of around 70,000 ounces for many years going forward.

At the current share price the shares are trading on a PE ratio of 4.4 which increases to 8.4 on next year’s consensus forecast, although I have no idea how old that forecast is. At the year-end the group had $6.3M cash on hand, $8.1M in short term deposits and a further $2.2M available as undrawn borrowing facilities.

Overall then this has been a very strong year. The profit increased, the net asset base grew and the operating cash flow improved with plenty of free cash being generated. The group has benefited from both the increased basket price and production levels and with the latter due to improved flotation technology, this should be sustainable depending on how project Echo goes. The project seems to have got off to a good start but with anything of this size, there is inherent risk. There is not much happening with exploration but I would prefer the focus is on Project Echo and if this year is anything to go by, it seems plausible that they will complete it without having to raise any more equity. I am tempted to buy in here.

On the 30th October the group released an update covering Q1. Overall 16,589 ounces were produced, which is an 8% decrease on Q4 due in part to the scheduled closure of the Steelpoort plant. Annual production is still forecasted to be 80,000 ounces. Revenue increased by 7% to $14.1M, primarily as a result of a 7% increase in the basket price to $1,028, which has continued to improve since the period-end, and group EBITDA improved 9% to $5.5M. Cash balances grew by $2.1M to $17.14M.

As outlined in a prior announcement, the group agreed to axquire Phoenix for a purchase price of $6.6M and due to the close proximity of the business to the group’s existing operation, certain synergies are expected to be achieved. The acquisition together with the commissioning of the Millsell and Doornbosch secondary milling and flotation modules as part of Project Echo in 2018 are expected to increase ounce production in H2.

The cash costs increased by 18% to $496 per ounce, primarily due to the lower production but are expected to return to previous levels as Project Echo is rolled out.

As the first two MF2 modules of Project Echo, which are currently under construction at Millsell and Doornbosch, are commissioned towards the end of the next quarter, PGM ounces are expected to increase again and contribute towards the planned production of 70,000 ounces for the year.

Although PGM recovery efficiencies increased by 11% due to a combination of improved flotation efficiency at current operations and the absence of lower recovery efficient ounces from Steelpoort in the previous quarter, the PGM feed tonnes and feed grades were 10% and 9% lower respectively and impacted negatively on PGM production. The feed tonnes will remain lower in future due to Steelpoort’s closure but recovery efficiencies are planned to improve significantly as the project Echo MF2 flotation modules are commissioned towards the end of the next quarter.

On the 30th January the group released a Q2 update. During the period, Phoenix was integrated into the group and renamed Sylvania Lesedi. The SDO produced 17,302 ounces, a 4% increase over Q1, largely due to the integration of the Lesedi operation, with the business contributing 1,458 ounces, the highest production the plant had seen in two years, meaning the production from the remaining dump operations was around 4% lower. Revenue was stable in dollar terms due to monthly price adjustments on ounces delivered and group EBITDA decreased 11% to $4.9M quarter on quarter.

The cash costs in dollar terms increased by 2% to $507 per ounce but increased 6% in Rand terms, mainly due to the higher cash operating costs contribution from Lesedi of $651 per ounce.

The group cash balance at the period-end was $12.6M, a $4.8M decrease. Cash generated from operations before working capital was $4.8M with a cash outflow of $2.1M from working capital. $1.4M was spent on Project Echo, $1.2M on other capex and $6.3M on the Phoenix acquisition.

Plant feed tonnes increased 9% primarily due to the additional feed volumes from Lesedi, while Millsell and Mooinooi feed tonnes were lower than the previous quarter due to operational challenges. Mooinooi operations reduced feed tonnages were associated with lower than planned current arisings from the host mine in December as well as operational downtime associated with the delayed commissioning of a new tailings facility as a result of environmental authorisations that were received later than anticipated.

Excluding Lesedi, PGM feed grades were constant at 3.69g/t but overall the feed grade was 2% lower due to the reduced grades at Lesedi of 2.8g/t. PGM recovery efficiency was 11% lower due to a combination of lower recovery efficiency at Lesedi and recovery challenges at Millsell, Lannex and Mooinooi associated with plant and flotation feed stability which has since been addressed.

Project Echo continues to progress well with both the Millsell and Doornbosch MF2 modules being commissioned during December and the Mooinooi and Tweefontein modules in the design phase to be executed during 2018. Millsell MF2 commissioning, which included a complete new flotation section, was delayed by around a month due to construction and power constraints but Doornbosch MF2, where the old Steelpoort PGM flotation plant was relocated, was commissioned a month early with both sections expected to contribute significantly during the next quarter.

The group took full ownership of Phoenix Platinum in November and renamed the operation Sylvania Lesedi. During the past quarter the primary focus was on increasing plant production volumes, improving plant feed stability, feed grade and recovery efficiency and also to implement action plans to reduce overall production costs.

Current initiatives included the applied Sylvania operating model in terms of production and procurement, and the operation is already benefiting from involvement of SDO’s share production and technical management teams; mass pull optimisation strategy has been developed and implemented since late November in order to improve recovery efficiencies in the flotation circuit; plant feed tonnes and grades have increased since December through plant de-bottlenecking and resource scheduling; and the outsourced plant operations and maintenance contract was terminated in December, which should result in significant savings over the coming quarters.

The mining right for the Volspruit project has been appealed. All necessary documentation has been filed and the group is awaiting an outcome on a decision. The Grasvally Chrome project has been issued an Integrated Waste and Water use licence for bulk sampling operations which will allow the processing of the bulk sample on site.

With the Millsell and Doornbosch MF2 modules now in the process of being optimised, the board are expecting a significant improvement in production over the second half and remain confident, with the inclusion of Lesedi, that they will achieve the targeted 75,000 ounces for the year with 78,000 targeted for 2019.

Overall then, things seem to be progressing quite well here and I am tempted to buy back in.