Telford Homes have now released their interim results for the year ending 2019.

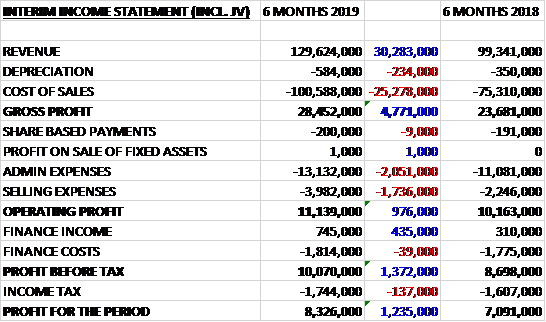

Revenues increased by £30.3M when compared to the first half of last year and after cost of sales also increased the gross profit was £4.8M higher. Admin expenses grew by £2.1M and selling expenses rose £1.7M which meant the operating profit increased by £976K. Finance income grew by £435K but tax charges rose £137K which mean that the profit for the period was £8.3M, a growth of £1.2M year on year.

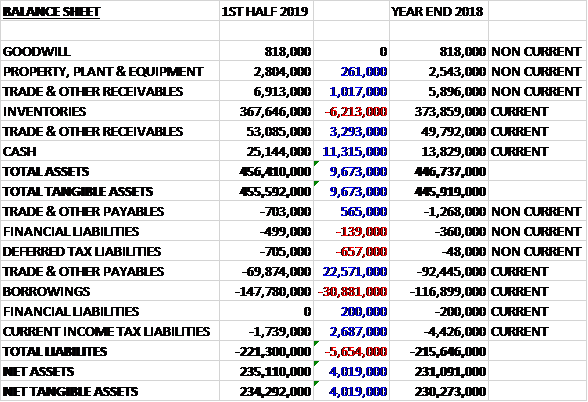

When compared to the end point of last year, total assets increased by £9.7M driven by an £11.3M growth in cash and a £4.3M increase in receivables, partially offset by a £6.2M decline in inventories. Total liabilities also increased during the period as a £23M decline in payables and a £2.7M decrease in current tax liabilities was more than offset by a £30.9M increase in borrowings. The end result was a net tangible asset level of £234.3M, a growth of £4M over the past six months.

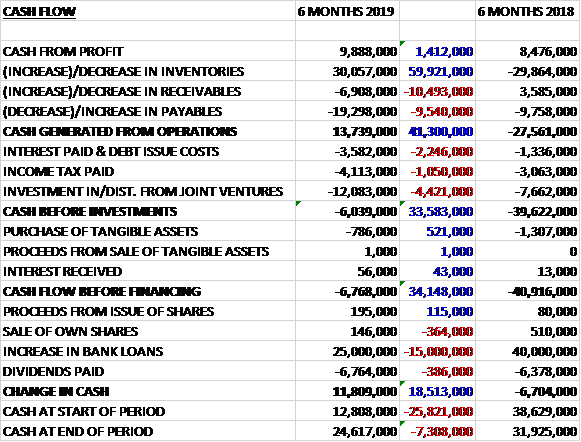

Before movements in working capital, cash profits increased by £1.4M to £9.9M. There was a cash inflow from working capital but interest payments increased by £2.2M, tax payments were up £1.1M and there was a £4.4M increase in the investment into joint ventures which meant that the cash outflow before investments was £6M, an improvement of £33.6M year on year. The spent £786K on intangible assets which meant that before financing there was a cash outflow of £6.8M.

The group are progressing well with their existing build to rent projects and in August they handed over The Pavilions, their first build to rent development which was purchased by L&Q in 2016. They are getting closer to build completion of the two schemes they are working on with M&G in Carmen Street and Redclyffe Road and the same applies to the build to rent block at New Garden Quarter which was sold to Folio. They are now moving towards entering a full build contract with Greystar for 894 build to rent homes at Parkside in Nine Elms and they expect to start on site early in 2019. In addition, they have announced that they started contractual negotiations with a major build to rent investor for the sale of 257 homes in Walthamstow and that process is nearly complete.

In October they announced that they have been chosen to partner a major land owner to obtain planning consent for around 700 homes on a site in East London, with a view to developing a combination of subsidised affordable housing, build to rent homes for the landowner and individual sale homes. This partnership with an established property owner is a key milestone in the build to rent strategy.

Also, with the help of Savills they are making progress towards identifying at least one institutional investor with whom they can forge a long-term partnership for future build to rent activity. The aim is to create a significant long-term build to rent pipeline to the benefit of both parties. They anticipate being in a position to select a partner by the end of 2018 with a view to entering into a contractual arrangement in early 2019.

Despite lower liquidity in the market as a consequence of uncertainty around Brexit the group have continued to secure individual sales, particularly for homes prices below £600K on developments that are complete or close to completion. Homes priced above £600K are currently more difficult to sell, especially if customers already own a home and are delaying a new purchase. This price point represents a relatively small proportion of the overall portfolio, however.

The group held their second off-plan sale at New Garden Quarter. The combined UK and overseas launch of Gallions Point resulted in 15 sales with performance supressed by Brexit worries and the potential risk of increased stamp duty for overseas investors. The majority of these homes are priced under £600K with completions due in 2020 so the board are confident they will be attractive to owner-occupiers at the appropriate time. Sales to individual investors, whether in the UK or overseas, no longer represent a significant part of the future pipeline with build to rent transactions and individual owner-occupier sales now drawing focus.

The open market sale remains an important part of the business model with the recent purchase from Greystar of part of their site in Greenford. The group will deliver 194 homes for individual open market sale at an average selling price of £500K, and 84 affordable homes for shared ownership. They intend to begin work on site in mid-2019 with completion expected in 2022. The group are engaged in discussions on two land acquisition sites. The current development pipeline stands at just over 5,000, including Parkside in Nine Elms, and has a gross development value of £1.65BN.

The group expect a much greater number of open market completions in H2 together with a number of new construction contracts and therefore the results for the year will be weighted towards the second half. There have been a few isolated cases of modest build cost pressures in later trades as projects complete but general construction activity in London, particularly residential development, does appear to have reduced a little in recent months which tends to take some of the pressure off trades that are otherwise in high demand.

Going forward the group still have work to do in order to achieve their original target of exceeding £50M of total profit before tax for 2019 and Brexit brings a certain amount of unpredictability.

At the current share price the shares are trading on a PE ratio of 6.9 which is forecast to remain the same for the full year forecast. After a 6.3% increase in the interim dividend the shares are yielding 5.1% which increases to 5.2% on the full year forecast. At the period-end the group had a net debt position of £122.6M compared to £103.1M at the year-end.

Overall then the performance during the first half has been an improvement on last year. Profits are up, net assets improved and although the group wasn’t cash generative at the operating level, the cash flow did improve. The build to rent focus should cushion the group somewhat but there is no doubt that conditions in the housing market are being affected by a number of issues, not least Brexit. The forward PE of 6.9 and yield of 5.2% suggest the shares are good value but I feel there is a real possibility that the group might not make its target sales if conditions continue to deteriorate.

On the 11th February the group announced that it had exchange contracts for the purchase of a site in Stratford for a total cash consideration of £20M. The land has been acquired from the Department for Transport. The 1.14 acre site is expected to deliver 380 homes with subsidised affordable housing expected to make up 50% of the development. The gross development value is expected to be at least £160M.

On the 19th February the group announced that it had exchanged contracts for the sale of its Equipment Works build to rent development site in Walthamstow to a joint venture between Henderson Park and Greystar. The transaction comprises the sale of the freehold interest in the land and the construction of 257 build to rent homes for a net consideration of £105.5M. The sale will consist of an initial land payment followed by regular payments throughout the construction period and a final profit payment.

The 3.16 acre site was purchased in December 2017 and has full planning consent for 337 new homes including 80 affordable homes and 18,830 square feet of flexible commercial space. The development is under construction and is expected to be completed in late 2021.

On the 5th March the group announced that it has chosen Invesco and M&G as their long term strategic partners for future build to rent transactions. M&G will be their priority partner for schemes including up to 200 build to rent homes and Invesco will have priority for the larger schemes.

On the 28th February the group released a trading update. Despite the positive outlook on build to rent the London sales market remains subdued. Whilst sales are still being secured they are being achieved at a slower rate than under normal market conditions and customer expectations of increased incentives and discounts are putting some pressure on sale margins.

In addition, two build contracts that were expected to exchange in 2019 are now likely to happen in Q1 2020, due primarily to planning issues, and this moves around £5M of profit between the two years. New individual sales secured since November effectively offset these contracts such that they still expect pre-tax profit for 2019 will be around £40M.

At this time they do not expect a significant improvement in the individual sale market in the short term and as a result expect a continued impact on sales rates and margins in 2020. They have also experienced some frustrating challenges in achieving planning consents on some developments including most notably the LEB Building in Bethnal Green. Planning delays can increase costs, push back the timing of profit recognition and impact on their ability to invest in new opportunities.

Finally they have experienced a disappointing delay to the construction programme in Finsbury Park of around six months due to matters dealing with transport bodies and the need to coincide with works undertaken by third parties. Given that completions were largely due in the second half of 2020 this will have a significant impact in terms of moving profit of around £15M into 2021.

These factors, combined with the impact of lower margin build to rent transactions, are changing their profit expectations for the next few years and they now expect pre-tax profit in 2020 to be significantly lower than 2019. After 2020 profits in each year will grow again, albeit at lower margins due to the increased focus on build to rent.